There are many people in Australia today with plenty of equity, yet very little freedom. They are the definition of equity rich, cashflow poor. Maybe you’re one of them. I was.

And that’s usually because of our love of property. While it’s been a fine vehicle for building wealth, it’s a very hard asset to retire on.

Net rental yields are low. Ownership costs are very high. And the lending environment has changed.

So to actually escape the hamster wheel and create the freedom we’re really after, we need to be open to new ideas. That’s what this post is all about!

I learned this first-hand on my journey to Financial Independence. As I grew my property portfolio, the lending environment was changing dramatically – effectively squashing the plan of refinancing our portfolio to live off the steadily growing equity in perpetuity.

In this ‘live off equity’ strategy, you need to prove serviceability to the banks, which is much harder than it was years ago. Your cashflow needs to be high, or your loans (LVR) need to be very low.

The first criteria is extremely hard to meet, after costs, with property in most parts of Australia. And the second one means you’ll need a huge amount of equity (many millions) to make it work. Neither of which are likely to be an effective or efficient option for the majority of investors.

Living off rents is often more viable, but also not a very efficient strategy for generating income from your wealth. We’ll go into that later. But after considering all the options, I decided to look at what other assets can be used to create a good income stream to live on.

And it turns out, there was one asset class right under my nose the whole time. I’d just chosen to ignore, because I was afraid of it.

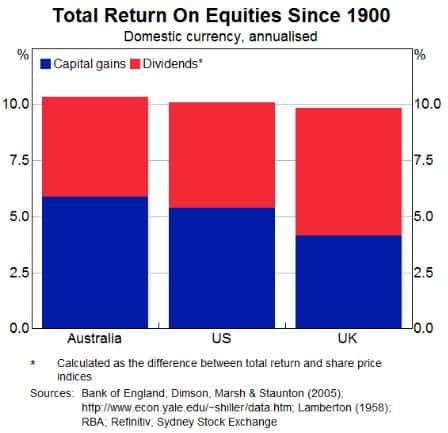

That asset class is Aussie shares. The reason I didn’t feel comfortable investing in shares (and many people don’t) was because, honestly, I didn’t understand it.

And that creates fear of the unknown. But after opening my mind and doing lots of reading, a light bulb went off in my head…

We needed much less equity to retire on, if those savings were just parked in the right place. Australian shares pay attractive dividends, and come with generous tax credits attached, which juice the income even further.

Which is why we’re free from mandatory work today, and have a growing portfolio of income-producing shares, rather than stuck at work for another 10 years, stubbornly trying to create the same freedom with property.

But I know, shares are scary, risky etc. I totally get it. I’ve been there. That’s why, today, we’ll cover all the most common worries about the sharemarket, from property investors and newbies alike!

And hopefully, by the end you’ll see shares in another light, and realise the massive opportunity available for those with property equity who want to be free sooner rather than later.

Well, where does this ‘casino’ label come from? Probably a few things. We see on the news each day, the market either went up or down, and we have no idea why.

We also see plenty of panicked headlines about ‘impending crash’, or ‘market sell-off’, or ‘billions wiped out’. Often times, that’s accompanied by frantic Wall Street traders yelling at each other and pulling their hair out!

No wonder we think it’s a casino! But let’s sit back and think about it for a minute. What exactly is the sharemarket?

It’s a market, where we can buy and sell shares. Thanks Captain Obvious. Shares of what? Of all the different listed businesses in Australia. Hmm, okay. So think of it as a big supermarket, for people wanting to buy and sell companies.

In fact, in the olden days, people used to actually exchange papers of ownership at coffee houses, in a dignified and business-like transaction.

Because they were, as we are today on a much larger scale, simply buying and selling businesses.

Obviously, nowadays it’s an online marketplace, which is more effortless. And we can also do it at near-zero cost. This, unfortunately, makes people more likely to trade more often.

The fact that we’re able to buy and sell at any time of the day, at any price we want, depending on how we feel, is what causes shares to fluctuate in price.

It certainly appears that way. But consider this.

If property was transacted the same way shares are, you’d likely see much more volatility than you do now. Imagine trying to sell your house every weekend. The turnout, mood, and offers will likely vary quite a bit. Some weeks people will fight over it. Other weeks, there’ll be little interest, or low-ball offers only.

One little fact that is often overlooked about property price indices, is that this price includes all renovations, extensions and improvements.

We know people tend to spend considerable amounts on their homes. Re-doing kitchens and bathrooms, putting in nice gardens, new floors etc.

So a $500k house, which 2 years later sells for $550k, could have had $50k of renovations done. No capital growth. But the 10% growth in sales price is what gets recorded. So there is a misleading upward bias to the data.

Because most approach property with a long term view, nobody worries about short term price drops. If someone comes and offers you 10% less for your house than you paid for it a few months ago, you have two options.

You can freak out about it, thinking you’ve lost money, or simply say “no thanks – I’m in it for the long term.”

The same common-sense thinking should be taken to the sharemarket. Just because you see the price, doesn’t mean you need to care about it. It can be tough at first, accepting the price movements of shares.

But all that price tells you, is what buyers and sellers were transacting for on that day. Most of the time, absolutely nothing has changed with those businesses.

The sharemarket has delivered very attractive returns for a long time. But to earn these returns, you need to be able to stomach a steep fall from time to time.

It’s a rare event, and nobody knows when it’ll be. Maybe once every couple of decades.

Just think about the long term trend of markets, and realise the world will keep turning, people will keep innovating, and the market, on average, will keep rising over time.

The other side of this coin is opportunity. When shares fall heavily, you have the very handy option to buy more shares at lower prices, and higher dividend yields.

If you’re building a portfolio, that’s exactly what you want! And if you’re living off the income from your portfolio, you can basically ignore it.

And isn’t it funny how the media loves to report the end of the world and markets falling, yet they pretty much never mention the steady yet enormous march upwards over the decades?

Often this is an emotional factor. If you buy shares in a company or index fund, you don’t control the actions of any of the people running it, or the results of the business.

But having direct control doesn’t mean you’ll get a better outcome.

I’m in 100% control of my Perth properties. I can do whatever I like with them. That hasn’t been the slightest bit helpful over the last 5 years.

On the flipside, I’m 100% responsible for them. Meaning, the burden of cost, issues and administration comes back to me.

Some point out the aspect of being able to renovate a property to add value. That’s definitely possible. And if you do the work yourself, it can work out quite well indeed.

But you can only do this once, and there’s risk involved. If the market falls slightly while you’re doing a renovation, you’ll be lucky to recoup your costs.

The other side of this is that renovations aren’t even optional. As property owners, we’re forced to repair, maintain and even upgrade the property over time, just to maintain market rents, otherwise nobody will want to live there!

Sure, you don’t control your shares. But that’s part of the benefit. There’s no responsibility on you and nothing to worry about. You also have more control over getting your cash when you need it.

You can sell off a chunk of shares and have $50k in your account in a day or two. Bit hard to do that with property!

This one is just flat out loopy. If you live in the big cities of Australia, look at the CBD. See the names on those skyscrapers. All very real businesses, wouldn’t you say?

Think of your local Woolies or Coles supermarket. Been to Sydney Airport lately? Driven on a toll-road? Visited a Westfield shopping centre? And most of us have loans with a major bank. They all seem pretty real to me.

There’d be hundreds of businesses or buildings you would use or walk past all the time. And without realising, many of those will be owned by a company listed on the ASX.

So by investing in an Australian index fund for example, while you might only own a tiny part of each business, you’re an owner nonetheless!

Try walking up and caressing the exterior of your investment property. Your tenants will likely call the police! Do it at Woolies, and people just think you’re a weirdo (I’ve only done it once – shut up!).

You know the term I hate the most? Dabbling. When you hear of someone ‘dabbling’ in shares, you can almost guarantee they have no idea what they’re doing. And that it’s going to end badly.

Many people who get into shares, for some reason, forget all common sense. It turns from investing into gambling.

Looking for the next big winner. Taking a hot tip from someone at the pub. Does anyone really believe that’s a realistic way to grow wealthy?

We love a punt in Australia. So unfortunately, the way many newbies approach the sharemarket is more like buying lottery tickets. Buy a bit of this and a bit of that and hope one of them goes to the moon. That’s not investing.

So I’m not surprised your mate/relative/work colleague lost money in the sharemarket! The market is very good at separating people who don’t know what they’re doing from their money. But that’s really down to an individual’s behaviour, not the market itself.

After all, go back to the long term performance of the sharemarket.

The only way you’re losing money is if you’re gambling, rather than investing. Or your time-frame is measured in months, rather than decades.

So approach the sharemarket in a healthy manner. Think very long term. Invest regularly. Diversify. Keep costs low. Buy and hold. Don’t trade. Reinvest your dividends.

And importantly, ignore the media! Do this, and you qualify for those healthy long term returns.

Ahh, this is a very good point! Shares are quite risky, individually. Companies can and do go broke and fall out of existence.

That’s not really going to happen with an individual property in a half-decent location.

So how do we fix this problem? Diversification. The more companies you own, the less reliant you are on any one company remaining prosperous. So if you own lots, like 50 or more, if one or two go broke, it won’t even matter.

By spreading your money across a diversified portfolio, you will have exposure to a range of industries too. Healthcare. Real estate. Financials. Mining. Utilities. Industrials. And so on.

Luckily you can do this at very low cost, by purchasing shares in listed investment companies (LICs), which may hold shares in 100 different companies, or a broad index fund, which will hold the largest 200-300 Aussie companies.

Okay, I think we’ve covered most of the main worries about investing in the sharemarket. Now let’s look at some other reasons why you should consider using shares to create an income stream.

If you’ve bought and sold property, you know there are substantial sums to pay. On the way in and out!

Stamp duty by itself is horrendous. Then we’ve got selling (and maybe buyers) agent fees, solicitor costs, bank fees etc. But let’s forget that and focus on what affects our cashflow.

Recently, I ran through our property costs since we’ve been doing our tax. And it’s actually a bit worse than I thought.

On multiple properties, various costs chewed up around half of the rental income. And that’s without anything major going wrong.

Just things like painting, carpets, special levies and a longer than expected vacancy. For most people, I think the ongoing costs are greatly underappreciated.

Each property will need you to tip in cash regularly for repairs and maintenance.

In fact, as I was writing this, my property manager informed me one of our tenants is saying they have no hot water!

Anyway, when measured over 10 years and then spread out annually, these costs alone puts a decent dent in your expected cashflow.

Then of course we’ve got the yearly costs, in addition to the lumpy ones above. Council rates. Water rates. Insurances. Strata fees. Management fees. Land tax. Which leads to my next point.

Shares on the other hand, require absolutely no extra cash from you to keep producing income.

The cash you receive is yours to keep. Rents and dividends are not equal. Not even close. Here’s why…

Take a 4% rental yield. After all the costs listed above, it’s going to erode at least a third of the rent. Usually closer to 40% or more. So you’re left with a net yield of around 2.5%.

Take a 4% dividend yield. This comes with no costs attached. And in fact, it comes with franking credits (a credit for the tax the company has already paid on this money before paying you a dividend).

A fully franked dividend means a 4% yield becomes 5.7% with franking. These credits either cover any tax owing on your dividend income, or if you’re in a low tax environment, will be refunded to you at tax time.

On the face of it the yields look the same. But in reality, the rent ends up being less than half. To get 5.7% rental income, after costs and before tax, you’d need a yield of 9-10%.

Can you get that? Maybe. But it’d have to be an extremely cheap (higher risk) location, likely with terrible growth prospects and perhaps questionable tenants. So you’d be sacrificing growing income for an ultra high yield today.

Ignore franking refunds for a minute. You’d likely need a rental yield of around 7% to match the 4% cash dividend yield. And that dividend yield will come with 30% tax paid, whereas the rent will be fully taxable.

What about commercial property? These deliver higher yields. But then your wealth is concentrated in one or two assets, with higher tenant/vacancy risk. Not ideal.

In short, Aussie shares generally provide a much higher cashflow, once all costs are taken into account. You could argue that rents may be more stable than dividends.

But rents can and do fall too. Coming from Perth, I’m speaking from painful experience. Even our well-located Brisbane property has had a double-digit decline in rent.

It’s often pointed out that while Aussie shares have franking credits, property has depreciation benefits. So they both have unique tax benefits. But these aren’t equal either.

You’re allowed to deduct your property depreciating over time, because its condition is literally declining with every year that passes. So while it makes for a nice tax deduction, it also means – yep you guessed it… future expenses!

The other thing is, depreciation is a tax deduction. Franking credits are a tax credit. That’s very different.

One is a real (future) cost you can use to reduce your tax. The other is real cash with your name on it, sitting with the tax office.

In addition, the value of franking credits are enormous. As mentioned above, it literally adds 1.5% or more to your yearly cashflow yield, if you’re in a very low tax situation, like early retirement for example. Or franking will cover a large portion of tax payable, if you’re on a high personal tax rate.

Even if we assume depreciation is a free kick, it may shield around a 25-30% of your rental income from tax in many cases. But then regular tax is payable on the rest of your rent. So depreciation is a real cost, and in any event, the tax saved is small in comparison to franking credits.

Even considering the yield differences, are rents and dividends likely to have the same growth?

Personally, I don’t think so. Some time ago I looked at this, measuring rental growth versus dividend growth, from two old fashioned widely diversified LICs Argo and AFIC (which are a decent proxy for the Aussie sharemarket as a whole).

While I’m sure the numbers aren’t perfect, in my view, a low cost diversified LIC or index fund is likely to provide similar or better growth in income over time, given the spread of quality businesses.

Why do I say this? Well for one, companies reinvest some of their earnings to help grow future profits and dividends.

Rents and property prices can’t grow faster than wages forever. Or people won’t be able to afford accommodation. And wages can’t grow faster than company profits forever. Or companies would go out of business.

So, in a grossly oversimplified way, company profits (whether listed or private) tend to sit at the top of the chain.

This is where value is created, through efficiency and innovation, which enables companies to afford higher wages, leading to higher rents for property over time.

While both rents and dividends are likely to outpace inflation over time, I think dividends may grow a little quicker.

This point is obvious, but worth mentioning. Having the investment income you’re living off, coming from only a handful of properties is pretty risky business.

You can diversify between locations, that’s fair. But you still have considerable amounts of money invested in a highly concentrated way.

When you compare that to owning say, 100-300 businesses from all over the country, which dominate here and also earn significant revenue from overseas, the difference is stark!

You’re then exposed to different companies, industries and economies. Even if the properties are in nice locations, the diversification is almost non-existent.

With your diversified shares, if a company or two goes out of business, you won’t even notice!

This can offer a bit of extra peace of mind, knowing your money is spread around, rather than concentrated in a few assets.

After having experience with both asset classes, the admin side of things is also different.

While we have property managers taking care of things, there are still semi-regular emails to attend to. Something needs fixed. Someone is moving out. You get the idea by now.

On the buying and selling side, there’s also no need to deal with banks, brokers, agents or solicitors.

Costs are insanely cheap ($9.50 flat fee to buy or sell $5k or $500k of shares with the click of a few buttons with a low cost broker, versus tens of thousands of dollars and a mountain of paperwork with property).

With shares, I’ve noticed there is basically no emails or maintenance. Rental statements come with bills and a list of costs attached. Dividend statements come with no bills, and instead, come with franking credits attached!

Given the simplicity of this, it’s also easier for record keeping and tax returns. Very much hassle-free.

We’re outsourcing both the management of our properties, and the management of our shares. And the costs here also differ.

Property managers tend to charge around 6-9% of the rental income as a management fee, in most cases.

But when all fees are included (inspection fees, property condition reports, admin fees, GST, letting/leasing fees, advertising), the real cost comes out at around 10-15% or more. I was also surprised to figure this out recently, having never really run the numbers.

Letting fees are usually a big one (often 2-4 weeks rent), and it usually occurs every couple of years as tenants move. Do the numbers for yourself, if you think I’m making this up!

So let’s say we’ve got $1 million invested in an Aussie index fund (the ASX 300), managed by Vanguard. Vanguard charges 0.10% per annum of the asset value to manage the fund. The fees taken out will amount to $1,000 per year. There are even cheaper funds than this, by the way!

Let’s say we’ve got $1m savings in a couple of paid off properties. If we assume a rental yield of 4%, the rent before costs will be $40,000. The total management fees, being 10-15% of the rent, will be around $4,000 to $6,000 per annum, on average. This is a decent difference in itself. Possibly $5,000 per year in cashflow.

What’s more, for the higher costs paid, you’re still on the hook for all decisions that need to be made. But at least you’ve got that much loved aspect of control! Looks like a high price to pay. On the other hand, your index fund will ask nothing of you, ever.

Instead, those 300 companies you own are being run by people trying to increase profits year after year, while you kick back with your feet up and watch those dividends hit the bank account!

While the income will flow in each year for both, with shares there are no vacancies to worry about.

Under this example, if one of your two properties is vacant, you might be missing half your income while you find new tenants. A little stressful, to say the least.

This post is not anti-property. We still own a handful of properties, which we’re slowly selling down over time.

And I’m not saying everyone should be fully invested in shares. But I am saying, if you have a decent amount of equity and it’s providing you little to no freedom, there are other options!

This is about overcoming the hurdles and worries to share investing. You don’t have to stay stuck being asset rich, cashflow poor. There is another way. Hopefully I’ve helped you see that today.

If you’re currently a property investor or newbie to shares, please think long and hard about the points raised here. Consider how you’re actually going to escape the daily grind.

Maybe, like me, you’ll decide that your capital is better off being invested in a low cost and low fuss diversified share portfolio, generating a strong and tax-effective income stream to live on.

That way, you can move forward with the next chapter of your life, from the happy position of Financial Independence.

In a future post, we’ll look at how you might go about transitioning from property to shares and live off your accumulated assets. Stay tuned! Update: here’s that post…

Turning Equity into Income: The Property to Shares Transition Strategy.

If you know someone who might benefit from this post, please share it with them. And thanks for reading!

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Great article dave!

For you to make money in properties, it will need to go up by 10% to compensate for all the transaction costs, so when you purchase a property, you are down 10% straight away. Most people choose to ignore this tho…..

Another problem with property is everyone wants to grab some $$ off you.

1) Councils will increase the rate regardless of the market condition or your rental income

2) Tradies still charge you the same and rip you off whenever they can

3) State revenue changes its rules to grab more land tax off you when they run out of money, doesn’t matter if your property has gone down in value

4) Accountants charges higher for preparing tax returns for properties than shares, because there is just more work involved with properties

5) Property managers don’t really care about your property as they dont have the owner mindset, they just want hassle free money flowing in.

If I’m making 500K a year and pays 49% tax and want to work til 65, then a high-quality property with potential for capital growth might work……… otherwise, I dont see the benefit….

You might argue you can leverage cheap with property and gain large profit, however, leverage is double-edged sword and can work both ways, you have to have the ability to pick the right property at the right stage of the cycle and able to hold on for this to work….

Thanks Jack!

Fair points you make. The leverage aspect is the saving grace and can work very well, but it’s not a slam dunk in many cases. Will go into that in the future.

Another thing I don’t like about property is the uncertainty with future income.

If I have 1 Million invested in shares, I can expect an income of $40,000 fully franked or around $57,000 Gross income P.A.

However, if that 1 Million is to be invested in 2 properties, the income will be around 25- 30K a year.

If a recession hit, and dividend drops 30%, I can still live on $30,000 a year. However, if the rent drops, together with prolong period of vacancy and increase in expenses such as insurance, repairs, rates… I have no idea what my income will be. This is the uncertainty that I cannot live with.

If you think this scenario is unlikely, just ask any perth property investor and they will tell you a different story.

Property investment is dependent on the state economy and Perth has an economy based on resourses which are now on the up. It has been a contrarian investment and is likely to outperform over the next few years as employment increases. You specific examples to justify a ramp of general statements is folly

1) All mining companies are making record profits but a lot of them are in production stage and moving towards automation which requires fewer people. meaning fewer workers needed in WA.

2) previous mining boom was due to a large number of construction projects on, requiring workers and jobs are plenty in WA at that time. This is not the case now, most mines are in production.

3) a lot of FIFO workers don’t actually live in Perth or WA, flying from melbourne or Brisbane doesn’t cost that much more than flying from Perth…

4) A lot of people got burnt in the last housing boom are in negative equity, as soon as housing picks up, they will be putting their house on the market, hence increasing supply and push down the price.

5) Business confidence is still very low in WA and I don’t see that recovering, you can read graphs and predict cycles and do whatever you want but all you need to do is drive around the surburbs and see how many vacant shops are there. Had a friend who appplied for a part time reception job and there were more than 200 applicants applying for this job.

So yes, Perth is most likely at the bottom, but I dont see house booming again anytime soon….. better returns elsewhere……

Hi Jack

Would love to know how I can earn $40k off a $1m portfolio!?

Can’t speak for Jack, but earning $40k income from $1m is actually very simple. The index fund I quoted in the article (VAS) has a dividend yield of 4% currently, which means it will pay $40k of dividends on a $1m portfolio. Plus those dividends are about 80% franked, which will give franking credits of around $14k. And the old LICs discussed on this blog regularly typically have a yield around 4% too, plus franking credits. Hope that’s useful Angie.

Hi Dave

yes that is very helpful. I am thinking of selling my property and investing in index funds and LIC shares instead!

Thanks!

Traditional Lics such as Milton currently trades at around 4.1% Fully franked or 5.8% Gross, this yield is similar to others such as WHF. Both pay a relatively stable dividend.

Otherwise index funds such as VAS pays roughly the same yield, which means 1million portfolio will deliver 58K Gross income.

You can also look at good quality REITs with long leases and low gearing, most pay above 6% yield.

Another great article Dave. I have a number of Investment properties and am seriously thinking of selling one and putting proceeds into more shares. On the property I have in mind I would likely have a small loss, but when you factor in all the additional holding costs and land tax it would be near enough to break even.

I recently put a PERTH property on the market and will take a capital loss.

Made the decision not because I think there is further to fall in Perth, in fact, I think we are at the bottom…. the problem is how long will we remain at this bottom and when will

It pick up ? I don’t see the market turning any time soon because I know so many people holding on for the market to turn and as soon as price picks up they will put their house on the market……

Thanks Jason. Even if the numbers weren’t as they are, I think it can still make sense from a simplicity and diversification standpoint. More hassle free and truly passive income.

Great article and 100% correct. I am also saying that investing in property in Australia has been ridiculous since 2003 (unless you like to speculate which is by definition not investing). Not at those costs and returns plus it is a huge bubble and it is deflating, and will continue to do so, simply because it is unaffordable to so many. Of course there is a bunch of other reasons which I won’t go into here now.

To maximise returns I moved countries and traveled the world, looking for opportunities.

Around 2012 I left Australia, being fed up with politics and bad legislation there, and to increase my net income and savings by 400% before looking for an opportunity to invest overseas in property.

I am in full control, know exactly what to expect cash flow wise (incl. repairs, taxes, management, and maintenance). I am running at +6% after tax which would be an equivalent to about 9.5% in Australia, if I had stayed and invested there).

If I was bound to exclusively living in Australia, for some reason, I would follow your advise and focus on Aussie shares. It is a good investment for now, but I would be careful on the timing closer to retirement age given we are in the 11th year of unprecedented growth and untested Modern Monetary Theory, which I believe is a hoax. Debt is at record high, people feel the crunch, especially in Australia, and if history is any indicator of the future, we are in for some interesting times.

Cheers FG. I’m not in the bubble camp personally, and I don’t believe we’re in for a long decline either. But I do think there are too many folks hanging onto their properties out of loyalty (the never sell attitude) and unnecessary fear of the sharemarket, and it’s blocking them from creating meaningful freedom in their lives – which is likely why they invested in the first place!

Hopefully this stuff is a little more convincing coming from someone who has been the leveraged property route and still has money in both asset classes, rather than articles written by hardcore share investors or fund managers.

I’ll throw another tangent into the mix

Imagine you separate or divorce at the worst possible time in either markets (property or shares), which will be easier to offload and divide equitably and amicably

Imagine trying to sell properties at the bottom of the market because you have too and worrying about tenants, mortgage payments etc..shares just seem a lot cleaner

With any investments, if you’ve made a mistake then you can always take your loss and move on. Worst case is 100% capital lose.

If you’ve made a mistake with shares, sell at a lose and get your money in 3 days.

With property, I know some properties in my neighbourhood that’s been on the market for 3 years and no sell. So whilst the property is on the market, you still need to pay all the rates and maintenance etc

And If you own one of these apartments in opal tower or mascot building in Sydney then you are exposed to >>100% capital lose, it can be an infinite liability. You are stuck with a house you cannot live in, cannot demolish and need to pay for endless rates/taxes/strata levy/mortgage and astronomical repair bills.

Who says property is safe and shares are risky again ?

Hmm that’s a good point Baz – it’s likely some properties are sold off at lower prices as people just want to get out and move on with their lives.

Another point with property is government interference to look after the tenants, fair enough i say but at the landlords costs..

Deadbolts and Security Screens, Security locks on windows, shatterproof glass on showers, hardwired smoke detectors and alarms, annual compliance checks (by electricians as PM’s aren’t willing to do) whilst there can be massive gains by leverage in a bull market compliance and governments can make things harder (introducing the NRAS, APRA, not removing stamp duty or sate taxes etc etc)

Then look at IKEA, BHP, RIO etc or even Google and concessions made to big business

Exactly, you can never predict future cash flow as there will be more and more compliances to follow and more rates and taxes.

When you buy something not for the cash flow and fundamentals but for it to appreciate in price, I call that speculation.

Investing in properties is a game of speculation.

Absolutely – don’t think anyone could argue the leverage can make a huge difference. Those gains are diluted by purchase costs, holding costs and later selling costs and even CGT. The security/safety stuff is completely fair for tenants, but as you say, those little things can add up too for the landlord.

As always, BEAUTIFUL post! This post is one of the gems you can find on the internet. People mostly only look on the surface, even looks (biologically speaking ie dating etc. And I admit I can’t help it :P). But when you think logically, there is almost NO chance of one finding a gold nugget lying on the surface of the ground ready for one to pick up. One has to dig deep. One needs to take the time and effort to read (reading widely is one solution to the situation of ‘You don’t know what you don’t know’), think/analyse and act. The good stuff are always covered under layers upon layers of things. And when you find a website like this, hold on to it. (Same for stocks.) The fact that many people like to leave everything to their accountants also makes it harder for people to even notice, let alone realise, the actual costs of owning investment properties. I’d say try to do away with the accountants and do it youself. Thank you, Dave. I love you to the bottom of my heart (not romantically :D) for doing a lot of the hard work (digging).

Thanks very much Michael, really appreciate it!

You make good points – we shouldn’t take things at face value and should instead poke a little deeper. We should really know how the numbers work ourselves, rather than relying on an accountant or other expert to do it for us. A good example is people comparing what a property was bought and sold for and thinking that figure is the gain, forgetting to adjust for all the costs to buy sell and hold along the way.

Thanks again for the kind words 🙂

Another great article Dave, really enjoy your straightforward thoughts. We probably have 5 years left of full time work after which we would transition to part time. We also own a few properties in regional NSW as well as Sydney. The issue will become which ones to sell and which ones to keep. There will also be the cost of capital gains when we do sell. I know it’s not a simple topic but would love to hear your thoughts around that.

Thanks Fastjewel. Very nice to hear you’ll be semi-retired in only a few years time – great work! It can get a little tricky trying to figure it out and while there are far too many variables in people’s situations for me to cover, I aim to give some examples and thoughts around selling down and transitioning to shares, which are hopefully helpful!

Hi Dave,

First time making a comment… Got to say one of our favourite articles you’ve done to date (couldn’t go past not mentioning) Nailed each point and make it really simple! We’ll be bookmarking this article and sharing it.

Keep up the great content!

faymeandmiguel

Thanks for reading and for the comment – much appreciated!

Very comprehensive post. Best post on the site.

Don’t forget about special dividends from AFIC, ARG, MLT and BLK from time to time. I’m yet to see a tenant come up to me and say, “Hey! Thanks for this property and letting me rent it. Here is an extra payment on top of my rent for being such a good property owner. Oh and I am also very sorry about the scuffed floors, backyard that looks like a scene from Jumanji, and broken plaster all over the house.”

LOL good point! Was laughing about this with a mate recently! Our tenants never say “you know we had a good year financially, here is some extra cash” 😉

Great article.

For many years, I was heavily invested in Melbourne residential property and it took me a long time to realise my mistake. From a financial point of view I was ultimately successful, but I never had peace of mind. I always dreaded checking my email in case there was a message from my property manager regarding repairs. It was always something … leaky roof, hot water heater died, electrical faults, plumbing issues. I gradually sold my properties and bought shares. I held onto one last house mainly because of sentimental reasons. But the final straw came when I was on holiday in New Zealand and I received a call from the property manager saying that there was a burst water pipe that extensive caused damage to the kitchen. After that was eventually sorted with the insurance company, I decided to sell in late 2017.

These days I am invested mainly in Australian shares, and I feel much more relaxed and happy. If I had my time again, I would never touch investment property. The fact that stamp duty is almost 6% of the purchase price means that the property investment is starting at a significant loss, not to mention all the ongoing costs of ownership that you listed.

With shares (LICs in particular) I have a steady and reliable income with the possibility of surprise special dividends, and no hassles with tenants and incompetent property managers. Also, let’s not forget the LIC gain tax deductions.

Occasionally I get tempted to buy a little investment unit, but I said to my wife that she has permission to slap me if ever I start talking about buying property.

Keep up the good work Dave.

Thanks Robert!

Glad you’re happy with your portfolio – the reliability of dividends (mainly LICs) and hassle-free ownership is really enjoyable.

The repairs/maintenance stuff is easy to shrug off at first, but it does always seem to be something. And then you start thinking you’re overplaying it in your head. But when you check the yearly rental statement – nope, you haven’t overplayed it, there was heaps of bills!

You’re right mate, stamp duty has become unreasonably high. There’s a great article about this which escapes me now – it’s risen as a proportion of property value for the last couple of decades as it hasn’t been adjusted (stamp duty bracket creep).

Haha at least you have a good backstop (your wife) if you ever get distracted 🙂

Dave they dont make a cape big enough for a superhero like yourself

great points all round

i am a 6 million net worth and still working in something that i really hate and about a 60/40 split shares to property have been so blessed with post GFC gains in shares but i guess personally its the departure from career and identity as a gen X still in the old mould work till you drop even though in todays environment i dont have to anymore the fight and the punch is still in the old dog

the question i have for you is what would you do ?

Haha thanks Josh!

Man, incredible job getting to the position you’re in – well done! There is no way I’d keep working a job I hated with a net worth that large.

Totally understand the identity thing – it’s very common. But you’ll form a new identity out of your current work – through how you spend your time (hobbies, family/friends, new work, investing) – it will take time but it will happen, and you’ll end up more fulfilled than before. If you can’t mentally make the break, then at least slowly wind down by dropping one or two days a week, see how it feels, then drop another day, and so on. Or even switch careers entirely if you still want to work full time, and transition to something that’s more enjoyable/meaningful for you, regardless of what it pays. Unless you spend half a mill per year or something crazy, you can afford to make these choices, for your happiness and sanity.

People would give up so much to be in the position you’re in, so make the most of it I reckon 🙂

And don’t forget the one thing that money will never buy you or Warren Buffet – time, and to a certain extent, happiness. The idea is to make enough money or more to ultimately enjoy life.

Can I ask why you’re still holding onto you IPs? Are you not worried about the opportunity costs by holding onto them? Apologies if you’ve addressed this in an earlier post/article.

Good question Aleks. Combination of things which I mention in my portfolio updates here and here. Also a secondary answer is (after all selling costs) some properties wouldn’t have much equity in them, so I’m effectively banking on them doing better over the next 5 years than they have over the last 5 years, so the opportunity cost is small in those cases.

Ripper article David.

One more point to add about shares and that is their divisibility. You can’t sell half a house!

One negative point about shares is leverage though. It is very easy and safer to leverage with property but lot harder/riskier with shares.

Cheers Paul!

I did mention the point on selling portions of shares vs property. The leverage point is fair, there is a clear difference between the two. On the other hand, property needs leverage for the return to be acceptable going forward, is my view. This post was really focused on retiring on these assets – we’ll go into the leverage aspect in another post.

But I won’t turn it into a property vs shares debate as that’s all rather meaningless and an unwinnable argument with too many variables. But just trying to balance the scales a bit and hopefully get a few pro-property people to see things in another light – it might even help them declare FI sooner 🙂

Apologies for missing out on the selling portions bit Dave, was a long read and must have got too occupied with the other great points in the post.

I am one of those pro-property people that are now seeing things in another light and all thanks to your great efforts so thanks for that 🙂 And definitely agreed, property vs shares is a futile debate, both have their advantages/disadvantages.

Shh, stop telling everyone how great shares are 😉

Hahaha kidding! I think articles like this are great to show the other side of the coin for those who have only ever heard the traditional Aussie property spruik.

Thanks Miss B lol. I don’t expect it’ll change many people’s views, but might help a few who are more open-minded and ready to see, which is good enough!

Great to point out the ‘hidden cost’ of improvements/ renovations on property market prices. I so often see people talking about seeing huge price rises in certain areas, or friends that have sold and made a tone.

Never hear people talking about the hundreds of thousands of dollars people spend on renovations, no to mention holding costs of a mortgage and possible renting at the same time when renovating.

Well put Trent – the only two numbers most focus on are purchase price and sold price and nothing else. The figures are often a little disturbing (from experience) when all costs are accounted for, so it definitely feels better to brush them off lol.

Another great read Dave! I think I saw you mentioned you will do an article about shares with leverage (I assume leveraging with house equity?) in the comment section? if so, I am very looking forward to it. Because I am planning to redirect my fund from my property redevelopment project to share. But I am more inclined to do a pay-down/redraw approach as opposed to a drip-feeding cash in the share market.

Once again, thanks for another great article. Reading your site has become my part of my routines now.

Cheers

Gordon

Glad you enjoyed it Gordon! Nah I’ll be doing an article on using leveraged property starting from scratch and comparing that to a typical share investor using cash only over a 10-15 year FI timeframe. But unlike most comparisons, I’ll include all costs involved and use realistic assumptions (even though they’ll be made up as I don’t know the future!). I’m doing this because I’ve been asked many times if it’s better to use property first for growth and then switching to shares for income later.

I’ve written about using debt with shares previously here, which includes estimates of returns you might make. Sorry if that’s not what you’re after, there’s simply too many possible scenarios to discuss! But that article I linked is all about paying down the mortgage and redrawing it (debt recycling). Hope that helps. And thanks so much for being a regular reader 🙂

Hi Dave,

Another great post. I’m glad I found your blog as it helps me to keep on track for my own early retirement journey. Very rare to find someone who writes as detailed as you do with such relatability for the Australian market. Many thanks!

I do have a question about MER, management expense ratio. You’re previous post where you review LIC’s, how exactly do we pay for those expenses such as 0.14% per annum. Is that deducted from our total capital based on the number of shares we own of the company each year or do we lose a share each year to pay for that management fee? I’ve always been confused as to how we pay for it.

Best wishes, Dan

Thanks for the comment Dan, very pleased you’re enjoying the blog!

The MER for an index fund is deducted from the value of the shares automatically (not sure how often), and given how small it is, it’s unnoticeable. And for LICs, the costs are typically the expenses for running the company for a given year, which comes from the LIC’s earnings before paying you a dividend. Doesn’t matter how many shares you own, the percentage fee is the same, so more invested means more dollars paid in fees, but the same % MER. Hope that makes sense 🙂

Hi Dave,

Tangentially related to this post, I’m curious on your thoughts on the old rent vs buy PPOR question. In this country, people have a view that if you don’t own a house, you’ve got nothing. Property ownership is basically a religion. I’m not a believer (especially when rental yields in my town of Sydney are at something like 2%) but I’m curious on your views. Apologies if you’ve already written about this elsewhere.

Cheers.

Hi Yaz, I wrote about rent vs buy a while back here.

I don’t think it’s necessary at all to own a house. Lots of pros and cons to each choice. I also wrote another post on housing that gets to the heart of the issue here (Is your dream house costing you your freedom?)

A bit late to the party here. I think you’ve made a lot of good points… however it comes across a little biased towards those who seek zero involvement in their investments. That’s not necessarily a bad thing, but look at the alternative view. Property can have a place in some investors portfolios.

For example, one could improve the property for additional capital gain.

One could build a granny flat or convert the property into separate dwellings to achieve dual cashflow.

Or rent out by the room or do short term rentals for extra cash – of course, assuming the property is suitable.

One could redevelop the property and build townhouses, if they were so inclined. Sell them all, keep them all – whatever floats their boat.

You can’t improve shares – it is what it is.

Of course this means one has to actively manage their property portfolio, and there are additional costs involved – but maybe some people actually like doing that.

I’m not saying that property is better than shares. We all know they’re different fundamentally, but for the right person, property could be a good option, just like how shares are a great option for others.

Thanks for the comment Ms FM. I guess it is biased to passive investors. This post was aiming at why property investors who’ve already built equity should consider shares to create an income stream to retire on. There are numerous ways to make money in property as you’ve suggested, this post isn’t arguing against that.

I just know there’s a lot of investors out there with plenty of equity yet little freedom, because they’re wedded to property and fearful of the sharemarket. And the same concerns are also had by newbie investors – so the aim was to provide an alternate (and hopefully helpful) viewpoint for those people, from someone who has experience with both asset classes and has learned a few things about retiring early.

This article is a nice short version of Peter Thornhill’s book. I completely agree with all the points laid out. The only problem to your article is that property has the advantage of being illiquid and hence serves well as a buy and hold asset – something the average mums and dads are good at. This asset class has done them well.

With shares though, how many of these average mums/dads can keep their emotions under control? Will they be able to deal with a 20% correction? What is going to stop them from drifting away from LIC/ETFs to being smart stock pickers. How many will sell off their portfolio during a correction rather than buying the dip? The market is a beast that welcomes the emotionally weak with both hands to rid them of their money.

No doubt, the smart and emotionally balanced folks should have stocks as their primary asset and property as secondary. However, the average person will eventually do well with property. It may not be the best retirement egg, but still better than having no egg (a possibility with stocks).

PS: I trade stocks for a living.

Very good points. The behavioural issue is a big one, and something I try to get across in many posts. But this wasn’t a property vs shares post for building wealth. As I said above to Ms Fire Mum, this was a message for property investors to open their eyes a bit and see the sharemarket in a different way, allowing them to possibly retire a lot earlier (the whole premise of this blog), by using shares to create income.

Back to the first line of the post – There are many people in Australia today with plenty of equity, yet very little freedom. That’s the ‘problem’ I’m trying to help with here, by providing answers to common worries etc.

If people still want to stick with property that’s totally okay, but it’s better they do it knowing there is an alternative and that they are possibly giving up many years of freedom, from their reluctance to cash out and invest that equity into shares. Hope that makes sense.

Hi Dave

I just had a question about rising stock prices and dividend yield.

With the current ultra low interest rate environment in Australia, this is sending more people into equities in search of yield and as a result is driving up stock prices as well as the P/E ratio. Would this mean that dividend yield would reduce in equal measure?

And if so, would this impact the old LIC’s dividend yield? Or due to the company’s profit and franking reserves they would be able to maintain their average 4% dividend?

Sorry if I’ve got this wrong, still learning how this all works!

Thanks.

Hey Scott. Yes dividend yields reduce when prices rise (if the dividend doesn’t rise too). Yes this impacts LICs, and investments of all types. They can only increase dividends if company earnings and dividends increase. But if prices are increasing, and earnings/dividends are flat, then the yield will be lower.

For example, Company A pays a $4 per-share dividend and its shares trade for $100 each – a yield of 4%. Prices go up 10%, and its shares now trade at $110. If the dividend is still $4 per-share, the yield is now 3.6%. Goes the other way too. If prices are flat and dividends increase, then the yield is higher.

You cant improve shares?

oh yes you can, business expand, business find new market, profit can be 2 times, 10 times, 20 times higher than it is today in the business journey, dividend and capital gain will comes with it.

Majority of Australian richest people run business that they found and float on the ASX, so these guys has improve their business and made a bucket load over time and shareholder enjoyed the same benefit.

I am at the receiving end of this I made no less than 7 figures just buy shares in business these family found and ride with them for decades, the Wilson family with Reece Plumbing, The Turner family with Fight Centre, The Lowy Family with Westfield and many more, life is magic with these guys.

each one of them delivered 30-40+ times return on invested capital and I lost count of dividend payment

over the years

Commbank was a small banks when it float by the government for under $10 bucks it is $80 today

and the dividend it paid each yeas is more than 60% the whole capital you paid for the shares every single year, you would got all your capital back in dividend and then more more more and that just on dividend

capital gain is the other extra ordinary returns.

Really great examples Charlie! Thanks for the comment!

I think Ms FireMum was referring to the direct control over property and how it can be renovated etc. Businesses obviously have drastically more levers to pull so they can grow, but I accept people can make money from property development. For some reason people go nuts over this control aspect of property, though I’m not as convinced.

Hi Dave,

Great article and very comprehensive.

We have gone through the transition from our one investment property to shares with satisfying results. What forced us to consider this change was that our property went up in value forcing our part pension significantly lower as we were being assessed under the assets test.

As mentioned in some of the comments, you can’t sell part of your property, and the rent was not increasing sufficiently to compensate (we had long term tenants as well). We ended up selling the property and after analysing the sort of factors you mentioned, including overcoming our fear of the stockmarket due to lack of knowledge, decided to invest there.

The results and the simplicity of management have impressed us.

Now, with shares, if the values goes up, and our pension is reduced, we have the option of selling some of those shares to compensate for the reduced income, if necessary.

Thanks for sharing your situation Den. Great to hear it’s worked out well for you. An awesome example of overcoming your fears of the sharemarket and ending up with a positive outcome!

Ah yes, the simplicity of shares is very enjoyable, and the income (with no bills) is heavenly 🙂