Today, let’s talk about everyone’s favourite topic: house prices.

House prices are sometimes pointed to as a reason why Financial Independence in Australia is excruciatingly hard, if not impossible to achieve.

But I have great news: This is false! And in this article, I’ll explain why.

So far, we’ve slayed the mythical dragons of the spiralling cost of living and how hard it is to earn a good income. Aside from kids, the other major hurdle is property prices.

In fact, I’ve written about housing multiple times on this blog. See the following articles:

Yet the same story persists: “I want to own a house, but house prices are so expensive. Therefore, financial independence isn’t going to happen for me.”

Do you have to choose between the security of home ownership and the freedom of financial independence? Fortunately, the answer is no.

We also have plenty of new readers around here lately, so this article gives us a chance to indoctrinate them with our well-meaning and empowering philosophy: “our level of freedom is the result of the decisions we make.”

That, and our intolerance for complaining 😉 Alight, let’s get started!

Let’s be honest. When we’re talking about high house prices, we’re only talking about two cities: Sydney and Melbourne.

You can hardly argue the other Aussie cities are expensive. While Sydney and Melbourne have seen strong growth in the recent decade, other cities like Brisbane, Adelaide and Perth haven’t had much growth at all. In fact, Perth has gone backwards!

Some people take advantage of this by moving interstate for a similar lifestyle at lower cost. But that’s not for everyone. This idea is usually met with comments around losing income or moving away from friends and family.

We’ll talk more about moving and trade-offs later. But the income part is interesting. We want the high incomes that big cities offer, yet we somehow expect the cheap housing of a smaller city. Wishful thinking?

We know the first factor in how much people can spend on housing is our income. And incomes have risen steadily over the last few decades, which is great.

But you’ve probably also heard that house prices have grown faster than household income over the last couple of decades. This is no doubt true in many places.

Which leads people to believe things have gotten out of hand and are therefore unsustainable. But is that true? How do prices rise faster than incomes?

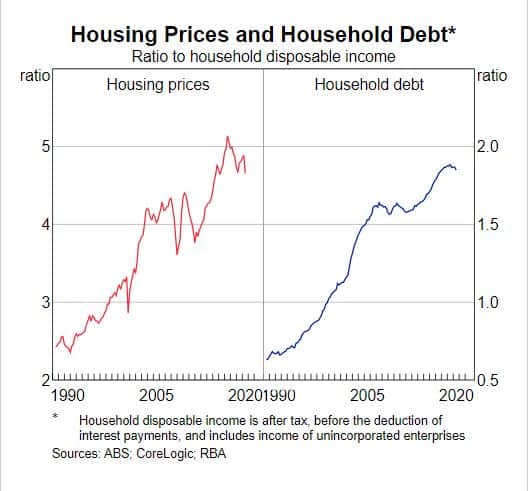

Nope, it’s not magic. Nope, not a government conspiracy either. Could it have something to do with the following chart?

Ahh yes, debt. The sweet nectar that economies thrive on. As we can see, households decided to borrow a shitload more money over the last 30 years.

Now, sceptics might suggest they were forced to borrow more because of rising house prices. Uh-oh… I hear something. It’s my bullshit detector going off. Everybody who participated in the housing market during the last couple decades was well aware of what they were doing.

We aren’t forced to do anything. Everything is a choice. We borrowed more because we wanted to. Either to get the house we wanted, to avoid missing out on house price gains, to avoid renting, or to invest in other property.

Having said that, this chart does look a little worrying, doesn’t it?

If debt has increased so much, how on earth can people afford this debt? That’s an easy one, which can be answered with another chart…

This shows the RBA Cash Rate, which is the main driver of mortgage interest rates in Australia.

Clearly, interest rates have been on a steady march downward for the last 30 years. There are multiple reasons for this which are outside the scope of today’s post!

So as mortgage rates came down, people decided to borrow more. Suddenly, they could afford a better, bigger, more badass house in a nicer location for the same weekly repayments.

See? There’s no conspiracy. Every subsequent property buyer (myself included) has participated in this by paying higher prices and/or taking on more debt.

And this might surprise you, but the amount of interest we’re paying is actually much lower now than it has been in recent times. That’s despite households having much higher debt.

Consider this: Interest rates were an eye-watering 18% about thirty years ago. Just last week I noticed one lender offering mortgages at 1.8%… a whopping 90% lower than what you could get in 1990.

Even just a few years ago, mortgage rates were around 5%. Now you can get a home loan for around 2% at the time of writing. While these are small percentages, the difference in monthly repayments is huge!

This rarely gets mentioned by the gloomy media. But right now mortgage repayments are way more affordable than they have been in a very long time! Using Moneysmart’s mortgage calculator, here’s an example:

Scenario A: 30 Year Mortgage. $500,000. Interest rate: 5%.

Monthly repayments: $2,684. Yearly repayments: $32,526.

Scenario B: 30 Year Mortgage. $500,000. Interest rate: 2%.

Monthly repayments: $1,848. Yearly repayments: $22,325.

Wow, the difference in mortgage repayments is $10,000 per year! And this ‘affordability benefit’ has occurred in just the last few years. This person now has an extra ten grand to save, spend or invest. Of course, being an Aussie, they might opt for the following:

Scenario C. 30 Year Mortgage. $700,000. Interest rate: 2%.

Monthly repayments: $2,587. Yearly repayments: $31,255.

As you can see in Scenario C, with lower rates we can borrow $200,000 more and the repayments are actually lower than Scenario A when rates were higher!

When interest rates fall, we have a clear choice to make. We can pocket the savings from lower repayments. Or we can increase our borrowing. Clearly, we know which option many Aussie households chose!

This is exactly what has happened on a grand scale in the last few decades. Rates have fallen dramatically, while our incomes have risen. More women are also working now, pushing household income even higher. So our ability to service debt has gone way, way up.

What’s the take home message here?

Because we aren’t paying cash, the affordability of our mortgage repayments is far more important than the overall level of house prices.

Okay, so maybe our debt level is manageable now, but it won’t remain that way forever, right? What about when rates go up significantly?

You should definitely allow for that in your planning. But in all likelihood, this is unlikely to occur anytime soon (2022 comment: that didn’t age well, haha)

Interest rates will only go up meaningfully when the economy is humming along, and the RBA wants things to slow down a bit (of course, they use fancier words than that!).

Increasing interest rates usually mean things are going well. It means wages are rising, and the economy is strong. In other words, when we are in a position to tolerate higher rates. If rates are increased too much, mortgages become less affordable, and people have less money to spend elsewhere.

This causes the economy to slow down, leading to the RBA eventually reducing interest rates once again. Alongside that, property prices tend to fall due to weaker buying power from the possible homebuyers.

It’s all a very fine balancing act. There’s nothing for us to do except be aware of its existence and make sensible decisions with our personal finances. If we do that, there’s no reason to worry and we’ll comfortably coast through just about any situation.

Even though it sounds like I’m saying there’s almost no impact on your house-buying ability, that’s not true. Because before we can get a mortgage, we need to save a deposit.

And yes, higher house prices mean a bigger deposit. So that particular hurdle is now higher. But remember, for those pursuing financial independence, saving is our specialty! Therefore, getting that deposit should be a piece of cake.

Compare that to other people who are too busy trying to Afterpay a pair of socks because they’ve already spent next week’s pay on a new phone and $35 lunches, wiping their sloppy face with an overdue power bill like it’s a damn napkin.

Hell, even a 10% deposit on a million-dollar property should only take a few years to come up with for dedicated savers. Of course, when you buy a house there’s also stamp duty and other things, but most states have great discounts and incentives in place to help with this, depending on the property price.

Honestly, I think much of the house-price frustration comes from looking at past prices and wishing we could pay those instead of today’s price. I get that. Who wouldn’t love to travel back in time and scoop up some prime real estate which now looks like a bargain?

I’m not even that fond of property investing these days, but I’d still give a kidney to go back and buy up a bunch of waterfront property!

Jokes aside, this feeling like we’ve missed out is dangerous. Because we start thinking life is unfair and everybody else had it easier. And that’s a dangerous downward spiral.

Sure, some people probably have had it easy. But an equal number worked their arses off to build the wealth they have today. Ultimately, we can’t go back in time. Playing a victim will get us nowhere.

All we have is the choices we can make today, and the future.

And today, we have the lowest mortgage rates in history. So, we can either bitch and moan, or we can look around and see that maybe, just maybe, there are more opportunities than obstacles.

Lastly, we’re easily biased and intimidated by big numbers. But – and I’ll say this for almost nothing else in life – focus on the repayments, not the sticker price. Go and do the numbers yourself with a simple mortgage calculator. You might be surprised at how affordable home ownership is in the current environment.

Buying a home and Financial Independence may seem like an either/or choice at first. But there are many things we can to do make home ownership and FIRE highly compatible.

Buy with a smaller deposit. Now, I know this is the opposite to what most people say (including the Barefoot Investor). But hear me out. The main idea behind saving a 20% deposit is to build a strong savings habit and become goal-oriented. If you’re pursuing Financial Independence, you already tick that box!

Next, the aim is to avoid paying Lenders Mortgage Insurance (LMI). This is usually payable when you have a deposit of less than 15-20%. This protects the bank from loss if you default on your mortgage and they need to sell your property.

But these days, we have the First Home Loan Deposit Scheme from the federal government. This removes LMI for the homebuyer and protects the bank from losses. From all reports, this has been incredibly popular so the government will likely keep supporting it.

I think it’s perfectly fine (maybe better) to buy your home with a small deposit. BUT, only if you already have a solid savings habit and you can pay very little or no LMI.

Now, you could argue this doesn’t help you avoid high house prices. True. But this does help you lock in your home price sooner and put more cash towards investing, which is what really creates wealth and makes early retirement dreams come true.

The easiest way to meet both your home ownership and FIRE goals is to simply buy a less expensive place. Genius, I know. But seriously, it’s better to check our ego at the door on this one.

Be prepared to buy a smaller place than your friends if home ownership and financial independence is important to you.

Trust me, you won’t give a shit what they think in 10 years time, when you’ve got increasing amounts of freedom while they’re still chained to their jobs.

That’s what my friend did 10 years ago, and today he has more flexibility and less stress than his other friends.

Around 2009, my friend bought a modest apartment in a location he liked. His friends thought he was crazy and encouraged him to go bigger.

But he refused, thinking it made more sense not to overstretch, especially since the apartment was perfect for his needs.

Influenced by the prosperity of the mining boom, his friends proceeded to buy large houses, with more bedrooms than they needed and decked them out with beautiful new furniture (using additional debt like personal loans and store credit).

They’d invite each other over, partly to show off, and mentally compare what each one had recently bought. You know what happens next. The mining boom faded and Perth’s economy turned down.

Many of these people were saddled with large debts, and falling income. Some have been forced to sell up. And many ended up with ruined relationships due to financial stress.

As for my friend, he continued to quietly and effortlessly pay off his apartment (which is about half paid-off now). He still lives there contentedly and enjoys his life with very little stress, now only needing to work part-time. All because he decided to think for himself.

More recently, he told me these friends now see the wisdom and maturity behind what he had done from the start.

Even more than house prices, I see a bigger hurdle standing in the way of most people’s financial success. Themselves.

Being adamant that home ownership is non-negotiable part of a good life. Being reluctant to compromise on the size or style of a property. Insisting on living in a certain area of an expensive capital city.

Which is all perfectly fine, but may not fit with the goal of being financially independent in your 30s… on a low income… with kids… and overseas travel… with new vehicles… and a restaurant habit… and… you see where I’m going?

Some people are willing to give up one thing to get another. People move to Australia, say goodbye to their families in the hopes of building a better life here. That’s true of most of our families – almost everyone who is reading this – at some point in the past.

The truth is, we can’t have it all. We need to choose. We need to prioritise. That’s what life is about. If you want X, maybe you can’t have Y. Or maybe it’ll just be damn hard, so don’t expect it to be easy.

There are two things that annoy me more than anything. 1. Unreasonable expectations. 2. Complaining.

This article will upset some people. If I expected otherwise, that would be unreasonable. Therefore, I do expect at least a handful of people to have an instinctive reaction of “this article is complete bullshit” and “try living in the real world.”

That’s okay. This blog doesn’t exist to please everyone. It’s a platform to share my thoughts, experiences, and hopefully, help others create more freedom in their own lives, because I know how sweet it is.

And to achieve that, I write what I feel are important lessons, not what sounds good. Sometimes things are uncomfortable to hear, because we tell ourselves certain stories about the way the world is, and what is and isn’t possible for us.

Here’s the wrap: Do high house prices prevent Financial Independence? No, of course not!

Are they a hurdle? Perhaps. But not hugely so. And certainly not for motivated savers like the FIRE crowd with the lowest mortgage rates in history!

But if you’re not sold, that’s fine too. Because the great thing is, you don’t need to own a house to retire early. And if you do own a place, you don’t even need to pay it off before you can become financially independent!

So what do you think? Has David finally slayed the Goliath of Australian housing?

I look forward to hearing about your own conquest! See you on the other side!

…By the way, if your fellow Aussies are still using ‘house prices’ as the ultimate excuse for why FIRE is not possible, send them to this article and we’ll straighten them out together 😉

What are your thoughts on this topic? Let me know in the comments below!

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Interesting perspective on affordability. Question I’ve been asking myself in this low interest rate environment- would you use this time to pay off your mortgage debt or invest in more assets? Right now the properties I hold are 50% LVR. I’ve just been focusing on paying them down worried about rising interest rates- even if it is many years down the track.

I guess it depends. If you could be in financial trouble if rates went up, then paying down debt makes sense. If not, then I would definitely lean towards investing. With a mortgage rate of 2% or so, long term returns from investing will be far superior to that. But depends what you’re comfortable with.

Dave, when you say “high house prices”, how to best quantify it? I mean what do you consider expensive house price relative to income? Is it 7x gross income, 5x gross income?

I guess in many FIRE circle, many long to be financially independent well before the preservation age e.g. in 30s or 40s and buying expensive house would prevent them to be financially independent early.

I hope for you to produce another article with quantifiable examples sometime in the future (this is constructive criticism, for I love your blog so much I read every article). But I disagree with your conclusion saying “…high house prices prevent Financial Independence? No, of course not!”, at least coming from me who wants to be financially independent earlier instead of in my 60s or 70s.

Another question, how do you quantify someone as “house poor” ?

I don’t have a special metric that I consider ‘high’ or low. I’m just going by the commonly accepted statements that Australia has high house prices compared to the rest of the world (usually looking at house prices to personal incomes). So I actually don’t care how others are measuring it.

There is no need to slap a multiple on it like 7x income or whatever – that’s the whole point actually – in my examples I’m using prices/interest rates/repayments to bring it down to what tangible effect it has on cashflow. The lazy metrics like 7x income etc. are not useful as it doesn’t account for things like interest rates, which have an enormous influence on the affordability of mortgages.

I don’t know what you mean by ‘house poor’?

So what your saying, it doesnt matter how big your mortgage is as long as your repayment today (due to low interest rate) is small enough that it wont impact your cash flow. I get it. Thanks for sharing your thoughts on this, it makes me really think about forgoing the option of buying a house altogether

Basically yes, I’m saying the level of mortgage repayments matter more than house prices. People get all upset about house prices because of the big numbers involved, when in fact mortgages are relatively affordable. Of course, one still has to be able to deal with higher rates at some point in the future, but by then your income should’ve gone up. Certainly nothing wrong with renting if you prefer, owning a house is not mandatory for FI. Hope that helps 🙂

‘wiping their sloppy face with an overdue power bill like it’s a damn napkin’

This has got to be nominated for quote of the year!

I’m all serious though another great article! Cheers SMA

Haha thanks mate!

Agree! Great writing.

Yep laughed, read a few times, shared it and was about to quote it here. Will just add my plus one here instead (+1). Gold mate, gold.

Wow thanks, much appreciated! You guys are awesome 🙂

It’s almost laughable how simple it is! You might be able to afford the debt, but the mortgagee PDS doesn’t come with the list of things you have to give up to pay that debt back

Great article Dave. It’s amazing what you can achieve when you have a goal in mind.

You talk about houses prices being a lot lower years ago but wages were also low. Our first home was $55,000 I was earning $197 a week. The house I am in now was $360,000 purchased 4 years ago and I now earn $700 per week.

There are many ways to achieve FIRE but it takes time and patience.

You have to work out what is really important in life.

360k? Good deal! May I know where is this and how many bedroom is it?

Tassie 2 minutes to the beach 4 bedrooms 2.5 acres worth $560,000 now.

Wow that’s a lot of land. Must be beautiful there?! 🙂

Yes best place to live and retire!

Well said Bianca, it all comes back to priorities at the end of the day.

Thanks Dave, I have a close friend who scoffed & put their nose up at us for living in a 20km radius to Brisbane City rather than a 10km one like they are. Meanwhile we paid off our mortgage in 7 years & they are still renting saving for a 20% deposit to buy within their ideal area. The benefits of exploring all the possibilities and tradeoffs means we have gained so much more than if we were also so inflexible.

That’s a fantastic example Emma, thanks for sharing! Absolutely – having a mind that’s open to multiple ways of doing things is an asset that pays big dividends.

Top notch analysis, thanks for another great article

Cheers Adam, thanks for reading.

Love it Dave. Another quality article. I say to my kids “you can do anything, but you can’t do everything”. I agree it comes down to one’s priorities in life. For the shares vs property nerds out there, check out this fascinating video from Ben Felix, a Canadian blogger. I enjoyed his thoughts on the unrecoverable costs of home ownership. Yes, I know it probably makes more sense to include this video in a different article of Dave’s, but if I don’t share it here, I will forget about it…

https://youtu.be/Uwl3-jBNEd4

Thanks mate! Good saying too – hopefully your kids are soaking in the lessons I’m sure you’re passing onto them.

As a fellow Canadian, I will vouch that Ben Felix is great. He also has a fantastic (yet quite monotonous) podcast called Rational Reminder if you’re interested. Really get interviews on there.

+1 for the quote (I was also reminded of that while reading) and +1 for Ben Felix / Rational Reminder podcast.

It’s this huge battle between “The Australian Dream” and this idealistic pursuit of what ‘FIRE’ is, even though it’s completely subjective to everyone’s goals. Which is why you probably couldn’t ever slay this dragon, although you definitely injured the thing. Thanks for the great read mate.

Hi Dave, great article, specially around keeping the deposit low to allow extra saving and investing.

One thing I missed is the consideration around the area where to leave is around schools and family support, for example it might be cheaper to move further away to buy a cheaper property but maybe you would spend more to pay for a private school for your kids or being away from your family they can’t help taking care of the kids hence you need to spend more with day care, what is your view on that?

Cheers Lucas. Well that’s the tradeoff isn’t it? Very specific to the family situation and perhaps the area you live in, so there’s no blanket answer for that. Everyone has to weigh it up for themselves.

G’day Dave ,

Great read as always ???????? Thankyou .

On a different topic , I just read Jessica Irvine (economics writer for SMH) recent article titled;‘‘Do you have enough Super ? The answer might surprise you . ‘’…..it’s a great read .

Take care . ????

Thanks very much Jimmy!

Another great article Dave. Have to love the media’s throw away lines like ‘Australia has the most expensive housing prices in the world’. Where if the truth was told, Nearly half of Australia has the most expensive housing prices in the world. So you are on the ball again it’s a Sydney and Melbourne issue really as you say.

So still plenty of bargains out there depending on what floats your boat.

Australia’s debt issue well the media is definately underating that one.

Any wonder Afterpay and it’s Cohorts are thriving atm due to the herd not having any funds left on payday.

Cheers Dwayne. They’re called ‘throw away lines’ for a reason… that’s all we should do with them 😉

Great article Dave. I find it so odd that when interest rates fall and mortgage affordability rises, people will often choose to take on more debt as opposed to accelerating their journey towards financial independence. This article is a good reminder that we have more control over our financial lives than we often think.

Hey thanks, glad you liked it!