When people are looking for income, they are naturally drawn towards high yield invesments.

After all, if you want income, then a high yield is better, right?

Well, no not necessarily. There’s lots more to it than that, which we’ll cover in this post.

High yield funds, stock picking, yield vs growth, and individual goals – we’re doing a round-the-world trip! Then we’ll put it into the context of Financial Independence and finish with some simple take-home principles and a core message. Let’s go!

Before we begin, I dived into this topic before and set the record straight on dividend-focused investing in a post titled “Should You Invest for Income or Growth?” It goes hand in hand with today’s article, so definitely check that out.

It should be obvious there are two dimensions to most investments. Yield, being current income. And growth, being the level at which that income (or the investment’s value) increases over time.

Keeping it simple, investments with a high yield, tend to have low expected growth. And investments with a low yield, tend to have higher expected growth.

Wait a minute, why ‘expected’ growth? Well, because nothing is certain. Current yield or income is a bit more certain because it’s based on current profits. But it’s important to note, this is also subject to change!

Let’s take the example of a 7% annual return. Imagine a sliding scale of investment options, each offering different levels of yield and growth. For example…

A: Yield of 7% and 0% growth.

B: Yield of 5% and 2% growth.

C: Yield of 3% and 4% growth.

D: Yield of 0% and 7% growth.

Oversimplifying, as investors we get to choose which option we prefer. That could be based on our desire for income, our tax rate, and our views on each investment, among other things.

Some investors think, “Sweet, I’ll just go for all the highest yield stuff and build my passive income faster!” “Why should I bother with any of the lower yielding options!?”

Firstly, some companies trade at a high yield because their share prices have been hammered. Not because of a general market panic, but because the business or its industry faces genuine problems.

That being said, local investors like the tax-effective nature of Aussie dividends, so some tend to fill their portfolio with high yielders. And in Australia, this typically means buying lots of bank shares! But this isn’t a great idea for a few reasons.

Our sharemarket is already relatively top heavy. So even owning an index fund or diversified LIC means holding a decent amount in banks – around 20% or so.

Loading up a portfolio with banks means being very reliant on one industry for dividend income. Yes, they’ve done well historically, but they’re now facing some challenges (more on this later). The point is, by doing this we’re taking extra risk. So that high income comes at a cost.

A portfolio of only high yield stocks might have poor growth over time. This means dividends may struggle to increase, which is far from ideal. Dividends may even fall in the short term, if the high yield proves unsustainable.

Maybe a short term hit to your dividends doesn’t sound so bad, as long as the long term works out okay?

People are often attracted to high yielding stocks for the certainty of having a higher income today. I totally get it. But the irony is, a highly concentrated approach of holding a handful of high yield stocks means reaching your goal is actually less certain, compared to a diversified portfolio.

Some may argue my approach of investing mostly in Australia is kinda the same thing, versus having a global portfolio. I guess the key difference is, I’m not relying on a few companies in one industry for our income.

I’m backing an entire country and economy, with hundreds of companies in various sectors, with many doing business all around the world. So when certain companies or sectors are struggling, plenty of others are doing fine. Besides that, I’m comfortable with this risk and have found a level of diversification that feels right for our situation.

Back to the point. There is more risk and uncertainty picking high yielding stocks to achieve your income goal. And over time you might be missing out on the holy grail of investing – an effortlessly growing income stream which needs zero management from the investor.

Why? Because that’s much more achievable (and likely) with a diversified set-and-forget portfolio, than with a handful of individual companies.

Given the risk of uncertainty of picking a few high yield stocks, some investors then seek out high yield funds instead. On the surface, this makes total sense. It takes away the risk of picking your own stocks, outsources the effort and offers some diversification.

There are simply too many funds to cover. But let’s look at a few I’ve come across that are targeting the ‘high yield’ focused investor.

(The following is simply my personal thoughts on certain funds/products, not a view on the companies or fund providers themselves.)

This is a highly active fund which buys and sells stocks around their dividend dates to collect the highest possible dividends and franking credits throughout the year. This is known as ‘dividend stripping’.

How does the following sound as an income stream?

Holy cow, where do I sign up? This is income investing on steroids, right?

WRONG! While Betashares has some perfectly fine funds, including low cost index options, this is not one of them. In my opinion, this fund is an absolute piece of garbage. I’d almost call it predatory. A while back, I wrote an article about HVST for The Motley Fool, which you can find here.

Safe to say, I’m not a fan!

Total returns have been less than 1% per annum since October 2014. Or almost 4% per annum including franking. That compares to the market’s return of 9.7% per annum, before franking, according to this interactive Vanguard return chart.

Shares (units) listed at around $25 each. Today they’re trading at around $15. A 40% loss of value.

How about the income stream? Well, the first few monthly distributions were around 22-23 cents each. The last two payments were around 10 cents each. That’s a decline in income of over 50%. The exact opposite of what we want! Great income, huh?

Why does this happen? Because the 10-15% yearly income stream is simply not possible, since that is larger than what long term total returns would be.

The solution? You’re supposed to reinvest the income and franking, then somehow create your own income stream. With total returns of 0-4% per year, good luck with that! Oh, and the fee for this marvellous service is almost 1% per annum. PASS!

I can imagine many income-hungry retirees being lured into funds with the appearance of an ultra-high yield. Only to later learn (the hard way) that it’s too good to be true and see both their income and capital decline. And frankly, that gives me the shits.

By the way, I’m not picking on Betashares – again, they have some good funds too! I’m just running through some high yield funds which have been pointed out to me.

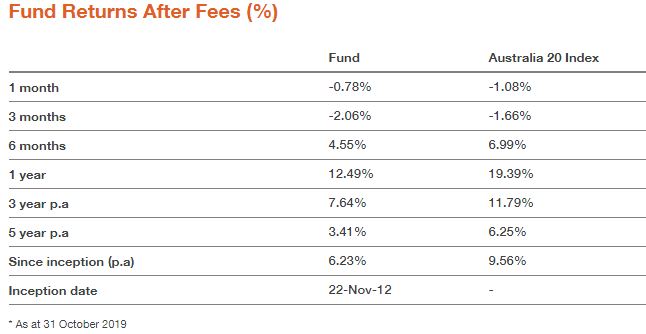

OK. YMAX holds the biggest 20 names in the ASX. Banks, miners, etc. And it boosts the fund’s yield by selling options against these holdings. This effectively trades capital growth for extra income.

In my view, this is a bit more harmless than the ‘dividend stripping’ strategy. But this portfolio is still very concentrated, with only 20 companies held overall. YMAX has about 50% exposure to financials, compared to 30% for the ASX300.

YMAX currently offers a yield of 9.5%, or 12% including franking. Does that sound realistic to you?

Anyway, the fund listed in November 2012. Here’s the performance since then…

The fund has underperformed the top 20 index (the exact same holdings) by 3.3% per annum. So the options trading has been a huge drag on returns. Fees charged are currently 0.76% p.a.

In the last 5 years, shares have gone from $11, down to around $8.50. A drop in value of more than 20%. Well, how about the income?

Total distributions paid in 2014 was 99 cents per unit. In 2019, total distributions paid was 76 cents per unit. A decline in income of more than 20%. Is that a coincidence? No.

Again, the yield looks great on paper. But in real life, it’s probably not the outcome investors are hoping for. The lesson is, you cannot expect an ongoing yield higher than a realistic annual return! If long term total returns are 8% per annum, then expecting a 9% cash yield is, well, wishful thinking.

Sorry, but the tooth-fairy isn’t going to fund those dividend payments.

There are also a large number of listed investment companies with high yields. But this high yield doesn’t come from the dividends paid by the underlying portfolio. Instead, the high yield is generated by trading.

Typically, these funds do lots of buying and selling, and hold stocks for a relatively short time. Capital gains are harvested by taking profits on their winners and distributing money to shareholders as fully franked dividends.

This doesn’t sound like a big deal, and in isolation, it isn’t. But when a fund is paying out very large dividends sourced from capital gains, there is a real risk the LIC runs out of profits to pay out. A bad run in the markets, or with their strategy, will see the dividend become unsustainable and eventually cut – perhaps drastically.

The company structure helps these LICs smooth out dividend payments over time. But it’s not magic. A strategy reliant on harvesting capital gains to pay large dividends is far riskier than one based on simply collecting the natural dividends from the underlying companies.

Therefore, as individuals, our investment income is on far less stable footing with these funds than more passive options.

This fund is closer to the buy-and-hold investing that we preach around here. And it was actually the first share I ever invested in.

VHY aims to provide ‘low-cost exposure to companies listed on the Australian Securities Exchange (ASX) that have higher forecast dividends relative to other ASX-listed companies’.

At the time of writing, the yield on this fund is a more realistic 5.3%, or 7.3% including franking. As far as high yield funds go, this is a decent option. Low cost (0.25%), not promising the world, and no fancy trading of options. It also holds 60 stocks right now, which is much more than when I held it (about 40) and is better than the other options in this space.

The issues for me are, it still has over 40% in financials. It holds stocks based on ‘forecast dividends’, meaning the portfolio is changed around a fair bit (turnover is regularly between 20% and 40%). This causes the fund to be less tax-efficient (more selling) and the income to be less reliable (capital gains paid out) than a buy-hold portfolio.

These aren’t big issues. But personally, I decided to move towards other income-focused funds like the old LICs, where the focus is long term ownership of companies, more diversification and steadily growing income.

This fund simply aims to hold and replicate the returns from the top 20 companies on the ASX. Nothing else. Like the YMAX fund, without the options trading. Fees are currently 0.24% p.a.

ILC is a concentrated portfolio of large caps. It’s good in the sense that it’s easy to understand and you know what you’re getting.

The current yield is 5.4%, before franking. Performance has been in line with the top 20 index, as you’d expect. My only concern here is the concentration. Financials currently represent almost 47% of the fund.

I mean, sure, you’re getting a higher yield than a standard Aussie index fund or LIC, which typically yields around 4%, plus franking. But it’s not much more. Is it really worth it?

It should be obvious by now that there is a clear trade-off going on. To achieve a higher yield, all else being equal, requires taking on some extra risk.

The above funds are very heavy in financial stocks. If bank dividends drop, a crunch in income is inescapable. Interestingly, 3 out of the 4 big banks have now cut their dividends in the last couple of years.

Of course, there are other sectors like mining. But mining profits are notoriously volatile, and just a few short years ago, BHP cut its dividend by 75%! So that’s hardly a safe haven either.

So far we’ve covered why direct high yield stocks like banks don’t seem to be a great idea. A top 20 fund would be a small improvement. And a high yield fund like VHY is better again.

The next step up is widely diversified low cost LICs and finally, broad market index funds. These two are clearly the most desirable choice in my eyes.

See a pattern here? Each step brings a slightly lower yield, but much improved diversification and a more reliable outcome. This means a higher likelihood of delivering a sustainable, and growing income over time to meet an investor’s cashflow needs.

This way, the performance of the underlying companies averages out. So even though some won’t do well, others will, and this is what drives income growth over time.

Widely diversified funds like low cost LICs, and to a greater extent index funds, hold a large basket of companies (100 to 300). Each company inside has earnings which are growing (or declining) at a different pace.

So within reason, it doesn’t matter what’s happening to the banks, or to the mining giants, or any company in particular. Yes, those companies matter because they’re large, but the results of the whole basket is more important.

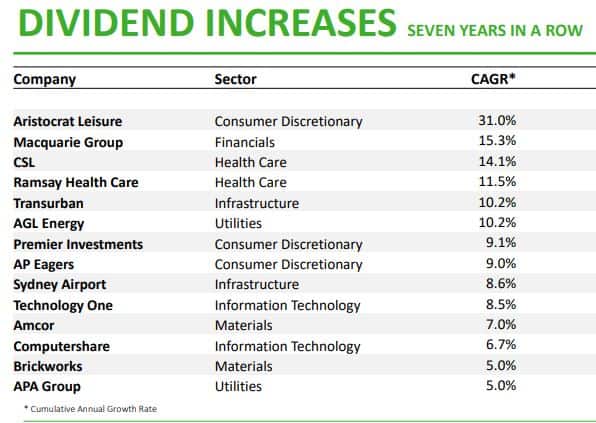

In its recent investor presentation (accompanying slides here), Argo looked back at its portfolio over the last seven years (emphasis mine):

“While the banks and some of the larger ‘blue chip’ companies pay good dividends, few of them have been able to grow them consistently over this period and indeed, a number have cut their dividends in recent times.”

“For Argo to achieve its own dividend growth, we have had to derive a growing yield from other investments. When we look at our portfolio over this seven-year period, there are 21 companies that have increased dividends in each of those years, including 14 which have increased by more than 5% per annum.”

“While we have added and trimmed some of the positions over this time, this group of companies have been the prime contributors to Argo’s continued dividend growth.”

“Importantly, approximately 25% of our portfolio is held in these 21 companies and this has allowed us to continue to grow our dividend, despite dividend cuts from other companies.”

Those annual dividend growth rates show why having a larger, more diverse portfolio makes sense. So you can benefit from companies with faster growing earnings and dividends, alongside those that simply pay a nice income today.

Some investors, like older retirees, might prefer a higher yield regardless of growth. They accept the higher risk and simply want the higher income now to pay for living expenses. I understand that, especially when franking credit refunds are included!

But for most of us with very long time horizons, growth is essential for our portfolio.

Of course, you can definitely make high yield investments a small part of your portfolio if you like them or they interest you. That’s what I’ve done. And provided the yield seems sustainable. But obviously some judgement is required here.

Our high yield choices are a few real estate investment trusts (REITs) and peer-to-peer lending. Simple rent-collecting REITs are typically more predictable and easier to understand than individual companies, but there is still extra risk involved (an article on REITs is coming, I swear!).

Now, it’s totally possible you find solid high-yielding companies that simply are unloved by the market. But I wouldn’t bet on that happening too often. Like that grey-looking meat at the supermarket, things are often discounted for a reason!

So be careful of the yield trap. If you’re not sure whether a yield is sustainable or not, or you can’t figure out why it’s so high… then it’s probably best to avoid.

Some of this stuff depends on each investor’s goals, tax rate, and their personal need for income right now.

But my point is, don’t blindly chase yield because you think it’s easy income, or it means you’ll get a higher return. As I’ve said before, growth is important and is a crucial part of any sensible income-focused investment strategy.

We don’t need huge growth, but we do need it. While a high-ish sustainable yield is fine, increasing cashflow over time is the goal.

I love income. But I’ll be sticking firmly with low cost options that are easy to understand and widely diversified. Things like index funds and old LICs for the majority of our savings.

Besides, look around the world today. Markets are up and yields are low almost everywhere. Interest rates are close to zero, so cash is earning next to nothing. All things considered, a 4% dividend, plus franking credits, is a damn good yield!

If you’re building a portfolio for Financial Independence and are frustrated with your progress and passive income so far, here’s what to do…

Save more money and buy more shares! That’s a simple and guaranteed way to see your investment income increase!

Oh, and maybe try to practice the Art of Patience.

It’s tempting to look for the highest yield stocks or funds to increase your income in the short term – I totally get it. But it’s rarely a good idea.

Instead, build a simpler and more diversified portfolio which provides a healthy balance of income and growth. Yes, that may mean a lower yield today. But it’s a much safer and reliable way to ensure you end up with ever-larger sums deposited into your bank account to fund your early retirement.

And that’s the true happy ending I want for you. Your very own Financial Independence utopia!

What are your thoughts on this topic? Do you have any high yield investments in your portfolio? Let me know in the comments.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Really good content. We’re grateful for you taking the time and effort to prepare this. Much appreciated, G & S

Thanks for reading Greg!

Very timely, thanks Dave, great article.

I spent the whole week going through the following ETFs trying to understand their return compared to my portfolio:

SPDR S&P/ASX Small Ordinaries (SSO)

iShares S&P/ASX Small Ordinaries (ISO)

VanEck Vectors S&P/ASX MidCap (MVE)

SPDR S&P/ASX 50 (SFY)

iShares S&P/ASX 20 (ILC)

BetaShares Aus Top 20 Eq Yld Maxmsr (YMAX)

SPDR S&P/ASX 200 Listed Property Fund (SLF)

I can see how you considered a few factors that I didn’t, there’s still a lot for me to learn. For now, I’ll stick to my LICs, VAS and possible add some VTS.

Thanks

Cheers Alex. If there is one thing about investing it’s to keep things relatively simple. There is no need to make things complex 🙂

Great article Dave, the yield trap is one of the most counter-intuitive concepts in FI – I think this will be super useful for many people 🙂 kw

Appreciate that Kurt – hope so!

I like the banks and yep they have been doing it tougher but its not like AFI, ARG, MLT etc have been hitting it out of the park recently either and thats probably because after all the BS these fund managers talk and write about the decline of the banks they still have them occupying plenty of space in their portfolios and we all know why. The why is that without those big banks those fund managers wouldnt be able to maintain their own dividends they pay out to shareholders and that yield would look very sick.

I’m 59 years of age so my needs are different and very much income based rather than growth but I do like my growth too. I bought the banks during the Royal Commission and it wasnt rocket science that they would get back up to where they before so IMO banks are a stock you can trade and treat like any other company. Too much is made of set and forget with income stocks, you need to be looking at opportunities or analyzing risk like any other investor would do and adjusting your portfolio.

At the end of the day the Banks wont be falling over though, because if they do the whole ASX will fall over.

re: Betashares….how many gimmick ETF’s can a company have?

re: HVST….just a con, but suckers are still throwing their money at that big yield.

Thanks for your thoughts Mark. Given their income focus, it would be hard to justify the likes of AFIC and Argo getting rid of bank holdings. I think even starting fresh today they’d still allocate 15-20% to banks, which is about what they have at the moment.

If someone has the interest to get in and out then they can totally take an approach like that. Many of us are too lazy or simply prefer the set-and-forget approach. Be interesting to see how the banks fare over the next 5-10 years. And yeah some of those ETFs feel very gimmicky or faddish to me… hope they don’t read this and decide to sue lol.

There are some interesting ETF’s that I have on my watch-and-see-but-do-nothing list:-

SYI – unlike VHY it looks at the last 5 years of dividend data

RARI – interesting but low liquidity etc

SWTZ – great concept and intention (dividend growth ….apparently) but MER too expensive

Haha I like the title of that list! Haven’t looked at any of those to be honest – there are simply too many around these days! I’ll stick with the cheapest, most boring and proven funds I think 😉

Another great blog post.

I have looked at many of the high dividend income ETFs. The thing that has put me off them, is the portfolio turnover can get incredibly high. The highest I’ve seen was around 55% in one year.

IFRA, ZYUS, WDIV, VHY are all over 40% portfolio turnover per year.

The only one I’d consider is SYI at only 10%. (it has been as high as 25% in the last 5 years).

I think a market tracking broad based index fund or a low cost LIC is the better option.

Some of these ‘smart beta’ ETFs are pretty dumb!

Haha dumb beta? Sounds like something Bogle would say.

Yeah the turnover is ridiculous sometimes, doesn’t really mesh with long term investing. I totally agree with your conclusion 🙂

Great article Dave. Even the name High Yield sounds like a trap to me. Steer clear. Dumb Beta… Love it. Dung Beetle.. Oh, and I’m sure I’m not alone in looking forward to your REIT post. ????

Haha thanks mate! Hopefully it lives up to expectations 😉

Some good information here, Dave. It never hurts to regularly remind oneself of the fundamentals.

I, too, fell into the trap of chasing high yields early on – I bought Prime Media when the yield was something like 8-10%. It did continue to pay a good dividend for a year but then the business hit a rough patch and the dividend was suspended, where it remains to this day! Not ideal.

Happy to say I learnt from that, and now focus my attention primarily on the good old LICs – which means I don’t have to chase yield anymore, it tends to come to me now!

Thanks for sharing Nick. I think many of us have early experiences like that (a few for me!).

It’s a shame when you see people who like the dividend strategy and then go off chasing all sorts of high yield investments, thinking that’s the same thing. As mentioned in another post, the strategy is ‘dividend growth investing’… the growth is a core part of it. But look who I’m talking to – you already get it 🙂

Hey Dave.

Nothing to add…just wanted to thank you for your posts and the effort you go to.

Thank you Martyn, I really appreciate that.

Love the analogy of “the grey looking meat at the supermarket”!!!

Thanks for another great post. I’ve learned a lot from this one (I’m mainly with old LIC’s, but the temptation to look at less boring ones is always there, and I’m glad I read this so I don’t get myself into trouble!)

Finally, I was going to ask, would you please write an article about REITs?! But I saw that you just promised it before! Looking fwd to it!

thanks again mate.

Haha good stuff Rick. The temptation to look for other interesting investments rarely goes away once you’ve caught the bug. So it’s handy to come back to the basics and remember what it’s all about. Thanks for the comment.

So what’s your advise for retirees who are seeking income and not growth?

Well I dunno it’s quite a personal thing. Depends how desperate one is for income, how they can stomach volatility, how old they are, how much interest and ability they have to invest on their own etc.

If I was in my 60s I’d still be banking on living another 20+ years so having SOME growth is still going to be important. To be honest, I’d probably still invest the way I am now, given a few well diversified LICs with some REITs or Ratesetter could still create a gross yield of 6%+, without as much risk as the yield-chasing options in this post. BKI yields 6.4% inc. franking for example, Ratesetter 5 year loans yield over 7% and some decent REITs are paying 6% or so.

Hi Dave

Cheers for all the content, i find myself regularly checking you sight for something new to get stuck into.

Question: Michael Burry of the big short fame sees a bubble forming in ETFs. Now i know you will say if the bubble burst it will just provide a great buying opportunity, but i was interested in your thoughts on whether LICs like arg and afi would provide some protection from this as they are actively managed?

I have recently switched from buying ARG to now buying VAS but am wondering if its worth the extra risk i now perceive from Burry’s opinion.

Cheers

Hi Joel, thanks for the comment. I don’t really buy the argument that index funds are going to blow up the market or make a crash much worse. Crashes happen and get nasty because of human behaviour and panic selling, and this happens regardless of what investments people are holding.

Does it really matter whether people own individual stocks, LICs or ETFs… if a large number of people are selling irrationally? I don’t think so. And just because something is growing a lot (indexing) and people are deciding to invest in a more systematic, low cost and diversified way, that doesn’t make it a bubble. Here’s a good counterargument to that – https://thereformedbroker.com/2019/08/29/the-real-bubble-has-always-been-in-active-management/

It may be the case that AFIC and Argo hold up a little better because they avoid speculative stocks and invest more in value/dividend-paying stocks (which tend to hold up a little better during a crash), but I wouldn’t expect the difference to be huge – they will still fall a lot!

Buy both Joel. Buy and hold both ARG and VAS. I do something similar with AFI and VAS. It’s a hybrid portfolio of a LIC and an ETF. Best of both worlds then.

Hey Dave. I am wondering about increasing dividends for the LICs that you have reviewed. Some have double in the last 20 years (AFI https://strongmoneyaustralia.com/afic-dividend-history/) and some have tripled in the last 20 years (AUI https://strongmoneyaustralia.com/aui-dividend-history/) and 6 fold increase in the last 20 years (SOL https://strongmoneyaustralia.com/soul-pattinson-dividend-history-whsp/).

Does this mean they trade off the performance to get the increased dividends?

Hey Murray. Nah, that’s not how it works. Some have had better overall performance than others which helps the dividend growth rate. Plus, some traditionally have a lower yield than others. Those with a lower yield tend to have higher growth over time, kind of like I’m explaining in this article.

It also depends on the payout ratio at the start of the period. If one LIC was only paying out 90% of earnings and the other paying out 100% of earnings, the first one has more ability to increase dividends in the following period (but probably has a lower starting yield). Hope this makes sense.

By the way, Soul Patts is very different to the others. If you read the reviews, it might explain a little more.

Thanks Dave. Yes I have some SOL for a bit of spice ! and consistent dividends 🙂