The end of year is fast approaching, so it’s that time again!

Today, we peel back the curtain as I share what we’ve been doing with our money behind the scenes.

This way you can follow along as I continue building an income-focused portfolio for us to live on and steadily transition from property to shares.

There has been a small change to where our cash is going, but nothing drastic. If you’re a new reader, you can see our last portfolio updates here and here, to get a feel for how we do things. OK, let’s get started!

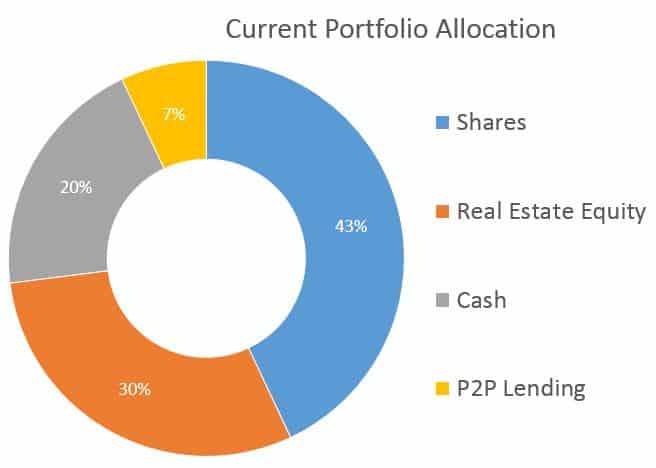

Below is the breakdown of where our net worth is located, at time of writing. Superannuation has not been included, and I’ve used percentages rather than numbers for privacy – you understand 🙂

As you can see, compared to last time, basically no change. Our peer-to-peer lending allocation has fallen slightly, as we’ve been using the cashflow elsewhere (more on this later). Other than that, it’s rather boring compared to the last update where we sold a property!

Going forward, we will probably look at selling another property in 2-3 years. If you’re wondering why we have so much cash, or why we don’t just sell all the properties now, this post explains.

Once we have a much simpler set of finances (no investment property), our cash holding won’t be very big at all – probably around 5%. I’m very much looking forward to those days!

As most of you know, this year the sharemarket has performed pretty well. In fact, the market has returned around 20% since the start of the year.

Our remaining properties in Perth have likely stayed the same or declined in value by a small amount. But the outlook for Perth continues to improve, with supply shrinking and the economy gaining momentum. Nothing is certain, but at least things are heading in the right direction!

The location of our other property – Brisbane – also seems to have a reasonable outlook over the next few years. Then again, maybe I’m just seeing what I want to see? Time will tell!

And finally, our RateSetter investment continues to provide a handy amount of reliable monthly income. The platform has maintained their track record of investors receiving every dollar of principal and interest owing, with the provision fund covering the small percentage of defaults to date.

At this point you might be wondering about the change I mentioned. Well, here it is…

We’re now paying principal-and-interest on every single one of our loans!

What does this mean? Well, it hammers our cashflow in the short term, with our loan repayments jumping quite a lot. Obviously this isn’t great when we’re trying to use our cash to build a share portfolio at the same time!

Why are we doing it? Well, because the interest rates for principal-and-interest loans are much more attractive than staying on interest-only loans. We switched most of them over last year, but two loans were on fixed rates, so we had to wait until that expired to switch over to principal-and-interest.

In some cases, the interest rate difference is 1% or more. That means on a $500k loan, we would’ve been forking out $5k more in interest every year just to stay interest-only. Now imagine you’ve got a few of these loans!

Also, we have zero ability to switch banks because we’re not full-time employees with a plain-vanilla home loan. We’re relatively income-poor early retirees, with one part-time job and lots of debt, lol. The banks don’t exactly get excited about that, and nor should they!

Well, our share portfolio will be growing much slower than we’d like. And our transition from property to shares will be much lumpier than expected.

But the extra money we’re now spending on loan repayments doesn’t disappear. It reduces the debt on each property. As we sell each property, it will now have less debt attached, so we’ll get more proceeds from each sale. So it’s more of a timing thing. That’s provided our properties don’t fall in value, obviously.

I would’ve much preferred to invest that money sooner and remain interest-only on all of our loans. But hey, you’ve gotta go with the flow.

In practice, the growth of our share portfolio will now be slower. And for the final couple of property sales, we’ll likely get quite large sums of cash due to lower debt. This is another reminder that having debt (especially lots of it), always puts you in a less certain position. It brings in another variable into your plans which you don’t control – something important to consider.

Another interesting phenomenon is that interest rates continue to move lower. And rates may even be reduced a little further in Australia. You can approach this two ways…

You can take advantage of lower loan repayments to pay off your mortgage much faster than planned. Or you can use the savings to invest more in higher-returning assets like shares or property. Staying in cash and term deposits, although it looks safe on the surface, is not a sensible long term plan. I wrote more on that here – Mortgage, Investing or Super – Where Should You Put Your Money?

There are also options kind of in-between, like peer-to-peer lending, which pays monthly interest without price volatility. In the current environment, the 5 year lending market on RateSetter is paying well over 7% per annum, which if you’re in a low-tax situation, is pretty good.

By the way, readers of this blog get a $100 bonus when they sign-up and invest $1,000 in the 3 year or 5 year lending market using this link (full disclosure: this blog also receives a bonus, so thanks in advance). I wrote more about RateSetter and how peer-to-peer lending works here.

Anyone with a home loan right now must pressure their bank into giving them a better rate. Seriously, there are some great rates out there, and it’s really competitive.

Tell your bank you want a better rate or you’re leaving, and that rates are available under 3%. Ask for their fixed rates too, some of these are very attractive.

Provided you’re in a reasonably good position (decent income, moderate debt), the banks will be very willing to accommodate. This one call will save you many thousands of dollars in interest over time. And if your bank won’t play along, then shop around and switch banks!

Even getting just 0.20% off your rate will save $1,000 per year, for a $500k loan. In many cases, you could save multiples of that. So do it as soon as possible! What’s the worst thing that could happen?

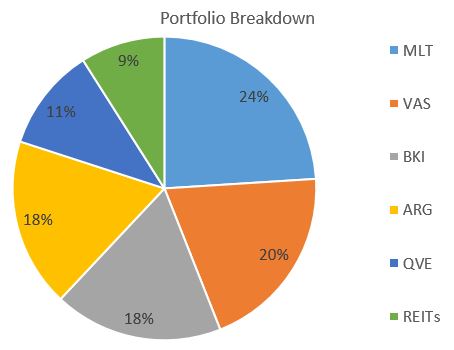

Since the last update, we’ve made a small handful of purchases. We bought more shares of VAS – the ASX 300 index fund. And we’ve also added to our holding in QVE.

QVE has underperformed its benchmark as value investing has not been rewarded. But the company has continued to pay higher dividends and is now trading at a large discount to NTA. We’re still comfortable with QVE as a long term holding and it aligns with our objectives.

Here’s how our portfolio looks right now…

Unlike some in the FI space, our focus is to invest for a growing stream of income through dividends. And overall, I’m pleased with the cashflow our portfolio is producing.

No real changes in holdings from last time. VAS has actually decreased slightly due to the market fall last week, with the LICs holding up a bit better.

Our REITs have increased a bit due to strong capital growth this year. We haven’t added to these as they don’t appear great value at the moment. And our QVE holding has grown as we bought more shares.

Just so you know, there are no major changes planned for the portfolio. We’ll continue to add to holdings that seem attractively priced, and if nothing stands out then we’ll probably just top-up our index fund or large LICs.

As mentioned, purchases every month or two will be pretty small, due to our now large loan repayments. A little frustrating, but that’s okay. Now let’s cheer ourselves up by looking at our dividend income!

My favourite performance metric. This is what really matters to us – increasing cashflow from our investments. Here’s our updated chart for the 2018-19 financial year (I missed a dividend last time).

In the last few months we’ve received a fresh batch of income from our investments. Almost all of our holdings paid higher dividends compared to last year, which was very pleasing. This income will be included in next year’s chart.

VAS paid higher dividends due to many companies in the ASX 300 paying special dividends this year. Both Milton and Argo increased dividends faster than inflation again. Milton increased by 2.1%. And Argo increased its dividend by 4.8%. QVE’s dividend also went up by 4.8%.

BKI’s yearly dividend was flat, but the company paid two special dividends in the last 12 months. All up, income from BKI including franking credits was huge – something like 9%. That likely won’t be repeated, but given our situation of near-zero tax and franking refunds remaining, I won’t complain!

Two of our three REIT investments also paid higher dividends and all have forecast for modest growth this year, in the region of 2-4%.

Because of the flurry of special dividends, we received a decent amount of extra income and franking credits which were welcomed, and thankfully, refunded at tax time. All up, it was a pretty good year to be an income-focused investor.

I’m already looking forward to posting next year’s chart. It might be a little irrational, but I love seeing that line creep upwards each year. You’ll probably laugh at this, but I’ll tell you anyway. I’ve translated this approach to another area.

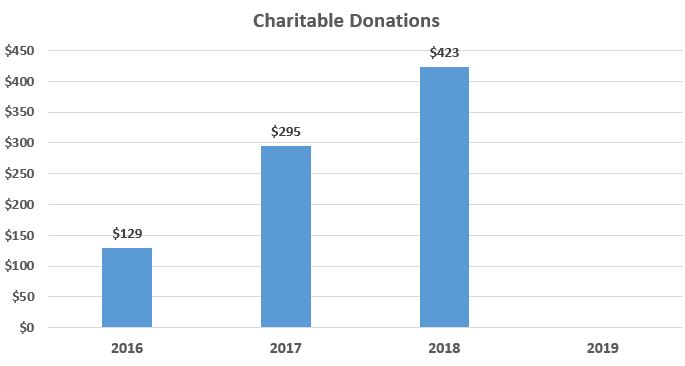

I’ve started a ‘Charity Donations’ chart, where I’m trying to do the same thing. A little bit nerdy I know lol. It’s early days, but here it is so far…

This one is measured by calendar year, like our household spending. I’m not 100% sure on previous years as we didn’t really track spending much before I started the blog, so I estimated from our tax returns.

The goal is to donate slightly more each year and keep the upwards momentum going. We’ve got a few years in a row so far, which is a good start.

Over time, hopefully it looks like a beautiful dividend growth chart, but extra meaningful, and something we can be proud of!

This is totally selfish. But this year for Christmas I’d like the sharemarket to fall. Not by so much that it freaks people out, like falling 30%. But just enough to cause a bit of a shakeup – say a drop of 10%-20%.

Oh, and ideally this would occur due to increasing uncertainty and fears around a recession, trade wars etc., rather than an actual economic downturn. Essentially, a nice discount from today but without a hit to company earnings or dividends.

Maybe asking a bit much, but it’s not totally unreasonable! What do you guys think? What would you like to happen?

Overall, we’re pleased with the increasing income from our share investments. The property side of things is pretty lacklustre, but hopefully improving from here (I’ve said that before). And we’re now (reluctantly) directing heaps of cash towards paying down debt.

At this point, I’m not sure whether we’ll always keep some debt around, or whether we’ll decide to become completely debt-free. Debt can have its advantages, but I’ve never heard anyone regret being debt-free. Anyway, still plenty of time to think about that.

So that’s what’s happening behind the scenes here at Strong Money. I look forward to bringing you our next portfolio update early next year.

In the meantime, how’s your portfolio going? Share in the comments, and thanks for reading!

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

I explain why (and how) I bought a Tesla. The experience so far. How much it cost, and ongoing savings/expenses. Charging options + EV basics. Tax rebates + subsidies. And whether you should get an EV.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Interesting stuff Dave. I suppose a benefit of paying down the property portfolio is that if you ever decide to keep any one of them, the yield will improve once the loans are fully paid off (as you’re not losing funds to interest).

Do you have the ability to refinance the loans back out to 25 or 30 years? That could reduce the cashflow hit quite a bit.

Personally I’m leaning towards investing more in shares than paying off loans, especially in current low interest rates. The potential return I’ll get, especially if combined with debt recycling, far outweighs the return from paying off my loans. My loans are all P&I, but I’m only making the minimum repayments, and directing everything else into the sharemarket.

Thanks, your approach makes perfect sense to me 🙂

Nah we aren’t able to refinance at all, the extension would be pretty handy tho! It’s true that the cashflow on the properties improves, but the net yield after costs would still be dismal compared to Aussie shares, so I can’t see us keeping any.

Hi Dave, just looked at RateSetter and their 1 month rolling investment pays 3.1%, their 3 year pays 2.6%. Inverted yield curve!

Haha yeah, pretty strange! Wouldn’t bother with 3 year at the moment, 5 year looks decent.

It’s been like that most of the time for the last month or so Sam.

That’s a good read SMA, thanks!

Interesting to read that around the mortgage issue. Gosh, $5k just to keep interest free – I had no idea the market could deliver a penalty like that, that’s brutal! Has that always been there – or is that a market change in the past few years?

That’s a lovely idea on the recording the charity giving front. Anchoring it to the portfolio income would also be another way to motivate yourself to keep growing that income. Like you, I think I would be back to my tax records to even find the amounts! 🙂

Cheers mate. The interest rate gap really opened up when the regulator cracked down on IO loans – it was more or less the same rate as P&I before this. The banks saw this as a green light to jack rates up in a bid to ‘discourage’ IO borrowing lol. Nowadays I think they’re happy to keep the gap there to sustain margins, though they’ve been reducing IO investment rates recently since borrowing from investors has essentially dried up.

Thanks, and that’s the idea – even if it’s just a tiny increase in giving on last year, it’s good to keep the momentum going 🙂

Love your blog Dave.

I’ve also been looking into QVE.

Old mate Nodrog got me considering it although I appreciate he always posts without any guidance or recommendations in place.

Regards,

The Incompetent Invesetor

Cheers mate! QVE requires patience or the ability to simply not care about performance vs benchmark. They stick to their value style regardless and as such haven’t owned the small tech names and other high flyers which have driven the small/mid cap index. No guarantees so one has to have a bit of faith in the strategy!

Hey Dave, great post yet again! You mention the slight transition to picking up VAS nowadays instead of being soley focused on lics which when the market declined or has a rough day stubbornly go to a premium to nta (like argo in the last week or so). How often does your investing plan involve topping up vas or other lics for that matter?? Monthly or when u have 2 to 3k or more? I see some ppl wait till they have 10k or more but then they ride out 3cent or 5 cent swings in share price in order to market time (dead cat bouce as PT says). I gather every couple months wont break the banj with commsec $20 brokerage or could even go to self wealth with $9.50 trades.

Cheers.

Thanks Peter! For most of this year I’ve been buying every month, usually around 2-3k… that may reduce now due to P&I loans as mentioned.

I know some people prefer to purchase less often to save brokerage, but I prefer monthly investing because I find it more motivating and it helps you create a greater feeling of momentum and progress 🙂

Having said that, I don’t want to pay more than 1% for brokerage. So with Selfwealth I’d make $1k minimum purchase, Commsec $2k.

Cheers for the reply Dave! Have u given lics or the index more love recently??? Seeing as tho you invest nearly monthly i assume no market timing on your part just buy Vas be it $81 or $83 or 84 or whatever!! Similar to Argo, no point waiting for as PT told you ” wait for what”! Keep investing! A good headspace to be in!

Yes we bought more VAS this month actually, regardless whether the market is up or down. The more we buy, the more our dividend income increases, and that’s about all there really is to think about 🙂

Thanks for sharing your posts Dave I always find them so Interesting and also I must say have picked up many Investment Ideas from them , I have now included 3 E T Fs , Argo , Argo Global ALI , and DUI , and I intend to add to them twice a year each time they go X Divided , Look forward to seeing where they are in 7 years time , once again Dave Thanks Mate

Thanks for the feedback Mervyn, glad you enjoy it!

Great to see the investment income increase Dave, is that purely from the shares or does it include Ratesetter and cash as well? And does it include the franking credits on the shares?

Also good to see the charitable donations going up as well!

Thanks AHF. Oh sorry, I stated this in the last one but not this one… I should prob state it clearly in all of them! Those figures are not including cash or ratesetter. Just dividends and franking.

Ratesetter will be included next time as the allocation is now more in line with what I had in mind. Was previously much larger but we were spending the entire repayments, so including this would’ve looked great but not been an accurate measure of passive income. Hope that makes sense mate.

I like your idea of tracking your charitable giving!

I’m not sure if you’ve heard of it, but there is a movement not unlike FIRE for charitable giving called ‘effective altruism’. Followers treat their charitable donations in the same way as their investments by doing due diligence and quantitatively analysing options against outcomes in order to maximise your giving efficiency (eg. lives saved per dollar donated).

I’ve found the analysis and recommendations on the following websites really interesting:

https://www.givewell.org/

https://www.effectivealtruism.org/

Thanks Bob. Yes I’ve read about that not long ago and it’s a fantastic concept. I haven’t used it yet, but will consider in the future. At the moment, we donate mostly to animal-focused charities, and random things that come up, including a local one here in Perth which is doing some re-vegetation for endangered birdlife.

Hello .

One way to help bird life is to plant trees wherever and whenever possible .

Currently , l am battling my local council in order to plant more useful trees in the park opposite my place .

The best trees to feed birds are any of the olive variety with the bonus that the trees never actually need to be fed nor watered , indeed when entirely neglected l find that they produce the best olive fruit crop !

Best wishes , Ramon .

Awesome stuff Ramon! Keep up the good fight!

Luckily in our area the council has been quite good and is planting quite a lot of extra trees (including food sources) and providing funding for the volunteer group also (saves them on labour costs).

Hi Dave,

I am surprised to see that we are in a very very similar situation, early retiree, asset rich, cashflow poor.

I have several IPs, lots loans. I invest in VAS and VGS (sold all AFI, ARG recently because after research, I found almost all LICs underperform index in the long run).

I don’t have a formal job (only some casual work income) so am unable to refinance my loans. I will have to be forced to switch to P&I on all of them very soon. So it will be a massive hit on my cash flow.

I have never sold my IPs but will be thinking of selling down some of them one by one to free up some cash.

I used to have this belief that I would never sell my IPs and will hold on to them forever. Also I thought debt is a powerful leveraging tool, but now I realise too, like you said, that the more debt you have, the more uncertainty it is, especial at my current stage.

Good thing is now the property market seems going into the promising direction (I am in Sydney), so we’ll see how it goes in the next few years.

Hey G, thanks for sharing – we do have a lot in common!

I really think makes sense to sell off property in retirement to put the equity into shares, much simpler and much better cashflow. I wrote about this equity rich cashflow poor dilemma here comparing an equity-rich property investor and a cashflow-rich share investor.

I hope the market picks up nicely for you and assists with your plans!

Hi Dave

Thanks for another great post. We’re in a similar situation, with the view to transition some investment property to shares over time. However most of our investment loans are fixed P&I for another 3 years apart from the largest one, which is variable. I totally agree with your comments about asking the bank for a better rate. Recently I have been onto our bank about what variable rate they could give us and they came back with a .4% reduction. Most people would be happy and accept this, but I went back and asked them again and they took another .2% off, so a total of .6% just for asking! They just wanted to know what rates I had found elsewhere, so you just need to do a little research but nothing onerous. So that reduction has at least offset a little of the fixed rate pain on the other loans! Now with the latest cut I’ll go back to them again. I wanted to ask you whether you DRP your dividends or take it as cash?

Wow, that’s fantastic! You must be saving thousands in interest vs before!

That’s the thing with fixed rates, the break-costs are often huge so you can’t really sell the property if desired. Having said that we also have mostly fixed rates right now because they were quite a bit cheaper.

We take the cash dividends, which then goes to living expenses, property costs or to buy more shares. I like the flexibility of getting the cash, but DRP is a good option too.

Hey Dave, when you say the market is up about 20%, which market or combination thereof are you referring to?

Dan, I was referring to the ASX 300 return including dividends since the start of the year. Vanguard shows it as 22% – https://www.vanguardinvestments.com.au/retail/ret/investments/product.html#/fundDetail/etf/portId=8205/assetCode=equity/?performance

Hi Dave, great read as always. I recall you mentioned at some stage owning VHY as I currently do myself. Did you find VHY easy to sell, as in there are no liquidity problems offloading them?

Thanks James. We owned the managed fund version direct with Vanguard, it was the first thing we owned. Shouldn’t be any issues at all in selling VHY as it’s a big fund (over $1 billion).

Hey Dave, great post! My wife and I also have two IP’s (in Perth) on P&I after originally being on IO. One is fixed at 3.69% which expires in a few months and the other is variable at 3.75%, both with Suncorp and under 80% LVR. It has been 1 year since we have reviewed our loans so we definitely need to negotiate better rates or find another lender. I’m interested to know what yourself and other readers current IP interest rates are and the lenders you are using. I’m tossing up whether to use a mortgage broker again or wade through the home loan minefield myself, cheers!

Cheers Paul! Those rates you’ve got are pretty good for investment properties. But you could probably get it a little cheaper these days.

Our lenders were setup with a broker at time of purchase and haven’t changed because we can’t meet serviceability to switch – we have Macquarie, AMP and Bankwest, rates are between 3.5% and 4.5% (the higher ones were fixed before rate cuts and high lvr so no room to bargain lol). I like using a broker generally, but there are some excellent rates out there with some online lenders that I’m not sure they have access to.

Lowest effort solution is to browse around at rates for IP loans and then bargain hard with your bank, saves the stuffing around of switching/broker paperwork. Any readers with thoughts to add?…

Hi Dave and Paul

I recently started researching a better rate on my P&I investment loan with Qudos since they did not pass on the full amount of the lastest rate cut. It is currently 3.84% (has an offset) so your rates are competitive Paul. I was thinking of using what I had in the offset account to buy shares, which is why I was researching better rates, but we have decided to get rid of all debt and use the rental income to buy the shares monthly.

Ratecity is a good start for a comparison website and will give you a good reference point to bargain. https://www.ratecity.com.au/home-loans/investor-loans

Ubank (owned by NAB) looks good, they have passed on the last two rate cuts and it has a good online calculator as a starter.

Love the blog Dave, and well done to you and Mrs Dave in working positively towards your financial goals. I understand your frustrations with holding onto property when your preference is shares, I’m in a similar situation, but at least it’s a first class problem and you’re not forced to sell.

Thanks for sharing that Mark, good stuff!

Ah yes sites like Ratecity are good for browsing what rates are available when you’re about to bargain with a bank. Ubank and some online lenders are incredibly cheap right now and are passing on the full cuts. Provided one has good serviceability these are well worth looking at since even if they jack rates up later you can always refinance elsewhere.

Appreciate the kind words too, thanks for following along!

Hi Dave,

How do you fell about QVE’s fees? A lot higher when compared to VAS or AFI.

Regards,

Hey Richard, I don’t jump for joy on the fees, but for a small/mid cap value manager with a long term record, paying 0.8%-1% is about my limit of what’s acceptable. And only given it’s a small part of our portfolio. Many active managers in that space charge higher fees and often performance fees as well!

Hi Dave,

I know that everybody’s situation is different, and I totally understand why you are holding on to your properties. But in my experience, one of the biggest investment mistakes I ever made was holding on to my last investment property for too long (for sentimental reasons, actually). I finally sold it in the 2017-2018 financial year and paid a hefty CGT bill. I plowed the proceeds into shares (mainly lics), and my investment income jumped by 45 percent (just lodged my tax return for 2018-2019).

Another investment mistake I made many years ago was to have too much of my investments in cash (term deposits). The prevailing wisdom of popular finance commentators at the time was that cash is an essential component of any portfolio. Given that interest rates have been trending downwards for a number of years, it is clear to me that “cash is trash”, and I am convinced that equities are the best way to financial independence. My investments now consist only of shares (apart from a little cash to cover a few months’ living expenses).

Great comment Robert, and thanks for sharing your experience!

I heartily agree with your conclusions. It’s funny that some say ‘cash is stable’ but look at the return on cash – has gone from 15%+ to 2% over a few decades. That’s a gigantic drop. Whereas the income from shares has grown relentlessly over that time. Sure the ‘value’ moved around, but so what!? It’s now worth many many times as much. I sound like Peter Thornhill lol.

We will eventually be entirely shares and minimal cash, and looking forward to it, even just from a simplicity perspective.

Enjoyed reading your update as always.

Is your charitable giving a percentage of your passive income? Or just giving where you can at the moment?

I like the idea of adding in franking credits to your dividend income, I usually just track the actual dividend and think of franking as an end of year bonus. I’ll add it in and watch my passive income grow overnight hehe.

Have a great day,

B

Hey Miss B, thanks 🙂

It’s not a percentage, just trying to gently increase it from where we started over time. Even if our passive income goes down at some stage, I’ll still try to have a small increase in giving.

Haha I like that idea. Franking is definitely worth including in my view, it’s real cash with your name on it that’s added to your total income at tax time. I’ll keep including it unless franking refunds are taken away, then counting cash dividends only will be more accurate. Thanks for the comment!

HI SMA

Thanks for the awesome info.

We are on fixed P&I homeloans that dont expire until 2021. I spoke with the bank and they want to charge us a break fee to have interest rates reduced.

Is there any way around this?

Thanks

Hey Joel. I don’t know of a way to get out of paying the break fee, but depending on the numbers it still be worth it, especially if it’s an investment loan. For example, if the break cost is $2k, but you can lower your rate by 0.5% or more, you might save much more than the break cost. See what they’re going to charge you and then figure out how much lower you can get the rate, either with the same bank or elsewhere.

Thanks Dave,

Did you guys get charged an early exit fee when you sold your IP?

Not this one as the loan had already come off fixed. For a previous one we did, and it was thousands (!) as it had a few years to go, can’t remember how much exactly.

Hi Dave.

Really appreciate your blog and opinions. I’m actually after an opinion here (from yourself or anyone else). I’m pondering going down the LIC (or index fund) path but wanted your thoughts on the following. For someone in their mid 50’s (who owns IP’s and not much in super), would it be better to plow money into shares (LIC’s) or put those funds into super? Assuming one is looking for an income stream at retirement (say in 10 years time), which would be more tax effective.

Cheers.

I realise there is limited info to go on here, but just after off the cuff opinion/s.

Thanks for reading Martyn.

Personally, if I was in my mid 50s and still working (moderate to high tax rate) and planning on working until retirement age, I would probably go the super route. There are lots of rules, but one could potentially be adding quite a bit extra to super in a tax advantaged way, and then it’s zero tax in retirement up to $1.6m of assets.

I love the flexibility and control of investing outside super. But I think in many cases super is more tax effective, and if someone is not going to be using the money until traditional retirement age anyway, then it generally makes sense to invest more through super. Hope that helps.

Agree with all Dave says and he has answered your question but I would add that everyone should look at the whole world and not just tax advantages. One caution would be that our politicians are showing an increasingly larger glint in their eye every time Super is mentioned. There is no doubt some “Political Risk” associated with Super.

Heya Dave,

I liked that dividend performance metric so much from the last Portfolio update that I decided to create my own and it’s sort of become like an anchor for when I catch myself getting caught up in the swings of the market.

I just had 4 weeks off from work and spent it abroad trekking through the mountains, so I was more or less out of contact with everything financial and market related which was a real refreshing state of mind but what I found more fascinating is I ended up returning with more money then I left with because of dividend payouts and market movements.

I’m still a long way off from achieving my financial goals, but I felt like that was a small glimpse into the power of investing, being frugal and working towards financial independence.

Thanks for the update once again, look forward to the next one!

Good story Scott, thanks for sharing! Having a complete break like that must have been great.

I also find that focusing on passive dividend income to be an excellent anchor, keeping you reminded what it’s all about (companies earning cash, rather than markets moving around) 🙂

Hi Dave, what are your thoughts on AUI? It looks pretty good to me but not many people seem to mention it much. Anything that I’m missing?

cheers!

Hey Rick. I wrote a review on AUI here.

Mate you’re a mind reader! I just finished reading it 2 minutes ago! I saw today it’s at a discount t of about 3%, do you think it’s a good time to buy some?

I’m now onto reading your Whitefield review!

As with everything, if you like it and want to hold it long term, then sure.

Hi Dave,

I’ve listened to an american investor share his strategy and it consists of having 3 months of living expenses in a bank account, then investing the equivalent to 3 months of living expenses in Bonds, then Reits, then Blue Chip Stocks, then Large Cap stocks, then Mid Cap Stocks then Small Cap stocks.

He moves from lower levels of volatility to higher. He said very clearly that this is his own strategy, and that are many ways to achieve financial independence.

I looked at these asset classes myself and identified the ETFs for each one of them, except Bonds, and then run a portfolio simulation in Sharesight to compare those ETFs individually with my portfolio (AFI, ARG, BKI, MLT, VAS) and my portfolio gave me a higher Total Return and Dividends. I’m not sure if I’m missing something, if this is not as attractive in Australia or if he might have picked stocks individually that have better performance than the ETFs.

Have you ever considered those asset classes or do you think that’s already part of VAS and LICs? (I’m still learning)

Thanks

There’s probably no way to know what drove the outcome unless you dissect every holding/breakdown in a portfolio and what happened to each market and sector over the time period (the outcome can vary wildly if picking stocks). Personally, I don’t see the point of breaking up asset classes too much like that, because large cap, mid cap, and small caps are all included in the overall market (and old LICs), as well as REITs, so we don’t have to think about it.

We can slice and dice in a million ways but I’d rather own a couple of funds instead of a huge bunch which I would have to add to and regularly rebalance. The overall goal is a diversified portfolio which spits out growing income over time. While either choice gets that done, I’d rather go with the less complex one. Hope that makes sense.

Thanks Dave, that certainly may be too much work with no real benefits.

Another question: do you ever overlap total returns of varios ETFs / LICs year by year in a chart?

I can’t find that already done in Sharesight, SelfWealth, Yahoo Finance, Vanguard or MorningStar. I’m curious to see all of them together, I guess I could build them myself. I see many charts of volume and price.

I don’t know if this is what your looking for but ETFWatch compiled a performace report chart for LIC’s and ETF’s for 2018 and 2019 which I found interesting to look through.

http://www.etfwatch.com.au/2019-financial-year-etf-lic-performance-report/

Hi Scott C, thanks, I’ll check that report

Hey Alex. Nah I don’t bother with things like that. Sharesight will be the best source, you can simply enter a pretend ETF/LIC purchase up to 20 years ago and compare it against each other, or the benchmark index (STW) which has been around since 2001, if that’s of interest? This will show total returns including dividends and franking.

Hello .

Some thoughts on a LIC portfolio construction ;

AFI ARG WHF AUI DUI BKI MLT CIN MIR ;

nine LICs , in toto , chosen for criteria of yield , mer ,and range of stocks ;

if these nine were to be equal-weighted the arithmetic averages would be ;

yield 6 . 8 % , mer 0 , 20 % .

l think such is to become my LIC portfolio in the crash to come , whenever that

happens to be , and bought , of course , opportunistically at the lowest prices possible .

Note , MIR specializes in small cap stocks , my one deference to the small cap

sector .

Best wishes , Ramon .

Correction ; MIR deals in a mixture of Smallcaps AND Midcaps . Apologies .

Take it easy , Ramon .

Hi Dave, I’ve really enjoyed reading your blog and especially the LIC reviews. I’m just curious as to when and why you got rid of AUI from your portfolio. Your review mentioned you own it in your portfolio, but it seems it’s no longer in there. On paper AUI ticks all the boxes and I’m thinking about adding it to my current LIC portfolio of AFIC, Milton & BKI. Is there a downside to it that made you want out? Not many people have it so I’m just wondering if there’s something I’m missing. Thanks and keep up the awesome bloggin!

Cheers Matt, thanks for reading!

All explained in a previous portfolio update here. 😉

Hope that helps.

Hi Dave,

Thanks for posting this. Just wondering where you get the money for your living cost.

Is a mix of dividend income and selling shares eg From dividends, do you take the cash rather than DRP? And for the remainder, do you sell of a bit of your shares or use Mrs SMA income?

Thanks

Hey Aly. I explained how we manage our cash in an earlier portfolio update here.

Essentially, cash from a property sale sits in an offset account. We use this cash, dividends received and whatever part time income is earned, to pay bills and remaining property expenses and usually manage a small share purchase each month to keep the portfolio growing. It’s very messy unfortunately, but that’s the way it is. Hope that makes sense.

Thanks Dave for being so transparent (and responsive). It really helps me benchmark my progress. Most of my savings are in the stock market so it’s not as messy.

I received a similar amount of divs as you ($20k). I am considering transitioning into semi retirement an was considering only working part time to supplement by dividends income so basically I would see how much dividends I got the previous year and work out how much I need to work (eg our year spending is around $50k and last years dividends payments was around $20k, so I would only aim to work and earn $30k this year). Is this a good approach or am

I missing something very fundamental here

No worries. Your plan sounds pretty sensible to me. The main thing is you’re willing to work to plug whatever gap there is, which is fantastic. Your position would be even stronger if you could make a little bit extra to keep growing the portfolio slowly over time, or if unexpected expenses popped up. But other than that it sounds good! Especially if you have some super you can access later on too – this is extra cushion in your plan.