“Should I pay off my mortgage or invest? Or should I put money into Super?”

These questions come up all the time for people looking to reach Financial Independence, or simply build a better future for themselves. And it’s a tricky one, because it depends on a lot of things.

Then of course, everyone has their own opinion on what’s the best option. So today, I’ll add my own thoughts to the pile and hopefully get those brain-juices flowing a little! But remember, nothing here should be taken as financial or investment advice – see my full disclaimer here.

Putting money into Super is not generally a strong focus for those looking to retire early. And in my view, that makes sense, given we can’t access the money until we’re 60 or older.

In this case, investing or paying off a mortgage usually fit the person’s goals better. But in some situations, the trade-off is much harder.

It really depends on your age and expected time-frame to retirement. Essentially, at your current savings rate, how long is it going to take you to build enough investments to live on?

Let’s say someone is over 40 now, and they expect to be somewhere close to Financial Independence at 55 or later. In that case, I would personally focus on investing mostly in Super, while building a small portfolio outside Super.

Then in the last few years I’d save a big pile of cash. Between 55 and 60+, I’d live on the investments, pile of cash and possibly do some part-time work to tide me over until I could access Super.

There’s a million possible scenarios – obviously I can’t run through them all! So that’s just one example of how I’d approach a late stage FI journey.

While you can never know the future, there are calculators made for people taking a blended approach to FI (super plus investments). I haven’t used it personally, but Aussie Firebug has one which may help you make some guesstimates.

And the government could change the rules around what age we can access Super in the future. One thing we know for sure is, we can’t rely on things to stay the same!

But if using a blended approach to FI like this, make sure you have a good Super fund. In fact, everyone should do that anyway!

I don’t have a favourite, but I’d choose a fund that offers a high growth (or 100% shares) option at low cost. This is likely to offer highest returns over the very long term.

Some of the better fund providers include Sun Super, First State Super, Hostplus, Australian Super and REST. See Pat the Shuffler’s investigative look at a few funds here.

In general, for people in their 20s and 30s wanting to retire early, Super is a much less attractive option. With a decent savings rate, there’s no reason why you can’t retire in 10-20 years on an investment portfolio built outside Super.

So in that case, I wouldn’t put a single extra dollar into Super.

The biggest catch-cry from the pro-Super crowd is the tax advantages. And there’s no arguing about that. With a tax rate of 15% on contributions and investment earnings, that’s likely to be a much lower tax rate than most readers are on currently.

There are limits of course. But given most readers are probably on a tax rate of at least 32%, that’s a pretty big free kick. However, those of us interested in Financial Independence need a pool of investments outside Super that can pay our bills.

So we need to concentrate our efforts into building those investments to create that freedom faster. Yes I know the tax benefits of Super are very attractive.

But a big investment account you have no access to, isn’t much bloody good if you want to retire early, is it!?

That leaves us with two other long-debated options. Paying off the mortgage vs investing.

Some assumptions in the calculations here. This is your home, not an investment property. And the comparison is against investing in the sharemarket with no leverage. This makes for the cleanest, simplest, and for my readers, probably the most common comparison. Assumes a 4% interest rate and 7% long term return from shares. Also that shares are held long term, not sold at the end of the period. Okay…

It’s often said that a 4% mortgage interest saving is equivalent to a much higher return from shares, since there’s no tax payable. Because a 7% return, that’s taxed at say 50%, leaves only a 3.5% net return. And a 7% return taxed at 35% leaves only 4.5%, which isn’t a huge jump from today’s mortgage rates.

So the answer is, focus on your mortgage first, as there’s no benefit to investing? Hmm. I don’t think that’s quite right for a few reasons.

First, what matters is your after-tax return. Not an ‘equivalent’ or hypothetical return. And in this case, the after-tax return is 4%.

Now to our shares example. What’s often missed is, this 7% return is not entirely taxable. Some is income and some is growth. In Australia, this would be 4% dividend yield and 3% growth. But only the dividend income is taxable. And because of franking credits, the investor gets a tax credit of 30%.

So for an investor on the highest tax rate (47.5%), there is some out of pocket tax to pay. This brings the after-tax yield down to 3%.

Once you add growth back on, the after-tax total return is 6% per annum. This means only 1% of the entire return was lost to tax, for the highest tax-paying investor. For anyone on a lower tax rate than 47.5%, the result is better.

Australian shares are very tax efficient. Even under the worst case scenario, investing still seems to offer stronger returns. And for most people, likely a decent bit higher than current mortgage rates of 4% and below. Let’s look at that now.

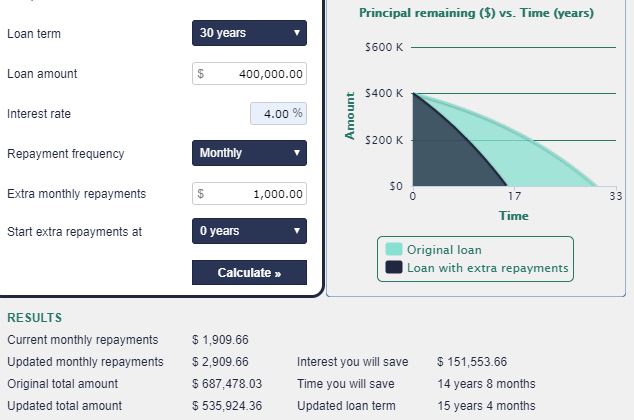

Let’s say you have a 30 year mortgage of $400,000. Your interest rate is 4% and your repayments are $1,910 per month. Over the life of the loan, your total repayments would be $687,478. That’s made up of $400,000 in principal and $287,478 of interest.

Now let’s say you also have saved up a lump sum of $50,000 and you can’t decide whether to invest it or pay down your loan. Let’s assume you put that into your mortgage.

Your new total repayments over the life of the loan are $591,712. This means you saved yourself $95,765 in mortgage payments. And your new loan only takes 23 years and 8 months to pay off. Pretty good!

A $50,000 lump sum earning a return of 4% grows to a total figure of approximately $128,000. Invested at an after-tax return of 6% (as above) in shares, your $50,000 would grow to around $190,000 over the same period.

Now let’s say you decided to use your monthly savings to pay off your home loan, rather than invest. We’ll assume you throw an extra $1000 at your mortgage each month.

In this scenario, your $400,000 loan would be paid off in around 15 years. Your total repayments would be $535,924.

Here, you saved yourself over $151,000 in interest costs over the life of the loan. In this scenario, at a 4% return, your total after-tax funds grow to $253,000. Investing this $1,000 per month for 15 years at 6% per annum in shares, you’d end up with a balance of about $301,000.

Both the mortgage and investment figures are before inflation. Think about how the value of debt declines in real terms all by itself. Due to inflation, $400,000 of debt today won’t feel anywhere near as much in 20 years time.

An offset account is a fantastic invention which Aussies are using to their advantage. This way, every dollar of spare cash is then effortlessly reducing the monthly interest bill. But it tends not to be a permanent scenario. Having a mortgage completely offset with your savings, forever, is pretty unlikely!

So the options are usually, invest that money or pay off the loan. Of course, you can do both using debt recycling, but that’s a whole other topic.

Initially, I did this post with some incorrect calculations which made the mortgage option look less attractive. I got this wrong and was admittedly influenced by another article I’d read on this topic. Apologies if this altered anyone’s views unnecessarily.

My view is still that investing is quite often the more attractive option. But I completely understand the certainty that comes with less debt and the guaranteed return of mortgage savings!

There is, however, a danger of focusing on the mortgage first. And that danger is laziness. I’ve heard of more than a few couples being so happy to be mortgage free that they relax their finances a bit, as a reward. But a number of years later, they’re still debt free but they’ve got nothing else to show for it.

This is a great position to be in. But having zero passive income is hardly the reward you want after so many years of saving. Also, you then have all your savings tied up in an illiquid asset. By investing in shares while keeping your mortgage, this gives you diversification.

So I think beginning to invest while still having a mortgage keeps you sharp, and allows you to benefit from higher returning investments and get compounding working harder for you. Later on, you can always cash in chunks of your investments to pay off parts of your mortgage if you really want. Be mindful of tax, obviously, but the option is there.

Some people aim to do both – pay off the house and build investments to live on, with the aim of timing it so they can be mortgage free at the time they reach FI. And honestly, that’s not a bad way of doing it.

If you want the certainty of less debt, I totally get that. It makes your cashflow more predictable, for one. And nobody can deny the psychological and happiness boost from having your own home paid off. A paid off home also gives you lower living expenses, forever. That’s very cool!

Another big win for the mortgage option is the forced saving element. While I’d normally say discipline is better, some people really need this. And this option is effortless too. Simply increase the repayment amount with the bank or setup an auto transfer when your pay goes in.

Having said that, I would still focus more on investing for higher long term returns and a faster road to freedom. But maybe that’s just me!

It’s pretty clear by now I think investing in shares is likely the best place to put long term savings for many people wanting to reach FI. Here’s a couple of reasons why.

Long term returns are very attractive. Global markets have averaged returns of around 5% after inflation since 1900, according to the Credit Suisse Global Investment Returns Yearbook. Australia has been a bit higher at around 6.5%. That tells us nothing of the future of course, other than if we’re lucky, hopefully we can expect that 5% real return to continue.

In modern terms, with inflation of say 2%, that gives us an expected return of 7% per annum. That is lower than history, but inflation is generally lower and more stable these days. And investment fees are now basically zero too. So net returns, after fees and after inflation, are likely to be just as good. For the hassle and effort involved (almost zero), that’s appealing to me!

Your income increases with inflation, or faster. While debt is worth less each year due to inflation, your shares will throw off dividends which grow over time with company profits. And that tends to be with inflation, often more.

Because of this, if you invest in shares, any year you decide to start paying down debt, you’ll have more income to do it with, in real terms. So investing first, gives you more firepower to pay down debt later.

Higher returns vs mortgage. As mentioned earlier, if you’re on a 47% tax rate, you’ll likely still earn a long term return of 6% after-tax in shares. Lower taxpayers will end up with a bit more. So that’s perhaps 2-3% higher than current mortgage interest rates.

Maybe that doesn’t sound like much. But imagine all the cash a good saver would be pouring in over a 10 or 20 year period. That’s a shitload of compounding returns missed out on!

For higher taxpayers, there are also more tax efficient ways to invest in shares, for those interested in LICs.

On my journey to Financial Independence, I focused solely on saving and investing. And starting today, I’d do the same thing (but would invest differently).

If I had a mortgaged house, I’d probably invest the bare minimum every single month. And if possible, I’d refinance every few years to a new 30 year mortgage term, to lower my repayments. This would leave more cash leftover for investing and see the mortgage get even cheaper over time due to inflation.

Of course, there’s no rule that says you can’t do both. But I’m kind of an all-or-nothing guy! If mortgage rates were higher (say 6% or above), then maybe I’d focus on the mortgage.

Here’s a few ideas for the current environment.

Home loans are now available at around 3.5%, it’s less attractive than ever to pay off debt, in my eyes. Not only that, interest rates are expected to fall a bit further from here. So you can take advantage of it by either paying off your home sooner, or using that extra cash for investing.

Aussie shares still look like a good option compared to other markets and asset classes. The dividend yield of the market is about 4.3% (at time of writing). And the long term outlook for Australia’s economy is attractive.

In the short term, as always, I have no idea what the sharemarket will do. But between you and me, nobody else does either! 😉

Another option I find interesting is peer-to-peer lending. I’ve been investing in this space using RateSetter for a few years now. We’re invested mostly in the 5 year market where interest rates are currently over 7% per annum. Here’s a snippet of the main market rates right now (3/5/19)…

Those rates are lower than recent years due to the platform getting more popular – RateSetter just reached $500m in loans. But the yields are still pretty attractive if you’re in a low or no tax environment.

From what I’ve seen, other platforms can’t match what they offer. Open to everyday investors, who can start with $10. And a provision fund in place which has covered all loan defaults since opening in Oz in 2014, and since starting in the UK in 2009.

Many are only open to ‘sophisticated’ investors (big money). And most have no provision fund in place, so while the interest rates look high, the return is less reliable – you have to cop the losses yourself.

With RateSetter, no investor has ever missed a payment of principal or interest. The provision fund is not a guarantee, but it’s been managed very well so far.

You can find out more in this overview of our experience in peer-to-peer lending with RateSetter I wrote a while back.

And remember, Strong Money readers get a $100 bonus when they signup with my link and invest $1000 in the 3 year market (this blog also gets paid for referring you, so if you sign up, thanks!).

As always, where to put your money is a personal choice. So there’s no right answer for everyone, and indeed, a combination of things is what most people go for.

Many times, it’s more about psychology than it is about numbers. So if you’d simply prefer to be debt free, then by all means, pay down that mortgage with no regrets.

But if you’re happy to accept more risk in the short term, for higher returns in the long run, then investing is the way to go. I think building an income stream from investments is the fastest road to Financial Independence.

What’s your view on these different options? And where are you putting your money at the moment? Let me know in the comments.

And if you enjoyed this post, get the latest Strong Money content by subscribing below!

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Great blog post, plenty to think about here. My personal strategy is as follows; as my investment income grows I put more into Superannuation. This keeps me in the 32.5% tax bracket. All Super contributions save 22% tax. This is the best of both worlds and works well for my situation. We paid off all debt early but interest rates were at 8.5%.

Cheers willis! Thanks for sharing mate, sounds like a good system you’ve got there 🙂

Great post!

Just thinking though that if you are 50 and have 15 years until retirement, wouldn’t owning your own home outright by 65 have pension benefits and thus favour paying off the mortgage vs investing?

I’m thinking about the Barefoot Investor’s Don Bradman strategy now.

Assuming you’re over the lower limit and below the upper limit, lower assessable assets (e.g. in the home) has a guaranteed return of 7.8% in additional pension payments. So yes, it could be a massive consideration.

Hey Peter, yes I think the trade0off is a bit different in that case. Given pension rules, it probably does make sense to go into retirement with a paid off house rather than a portfolio plus mortgage. Good thinking mate!

Yes, similar situation here, Peter. I wish I’d come across the FIRE concept 30 years ago! But then, I’m not sure it was all that well known back then.

Great article! If it’s ok for me to play devil’s advocate the mortgage does have one advantage I don’t think you stated explicitly: it’s a guaranteed rate of return. I can tell you recognise this from your language about share returns (“likely” etc) but it’s worth thinking about.

If investors can expect to be paid extra for more volatile vehicles it’s reasonable to say that less volatile ones are worth it even if they return less over the average xx year period. I can’t think of an investment that returns 4% guaranteed after tax in the higher tax brackets, so maybe the market thinks that it’s a pretty good deal. Especially if it’s an offset where you still have access to all the cash!

Thanks Stable 🙂

That’s a fair comment, I didn’t mention that. There is definitely a trade-off between the certainty of less debt and aiming for higher long term returns. We each have to decide what feels right for our own situation at the end of the day. An offset account is a fantastic invention!

Great article, thanks. Agree with your super points. I know the article can’t cover all scenarios but I reckon a lot of us FIRE tribe can pay off our mortgage in 5-7 years no problems, this tips the scales to favour paying off the PPOR in my opinion for the usual reasons; risk free, stress free and gives an achievable medium term goal to work towards. Just by 2 cents, cheers

Totally agree Nick. Many in the FI community don’t fit the typical 30 year mortgage scenario and can definitely smash a home loan in a short amount of time! Definitely all good points you make, thanks for the comment 🙂

This is one of the best articles I have ever read and I have been reading FI blogs for 8 yrs.

great work.

Very kind of you Prabhat, thanks!

We’re going with investing while slowly paying off the home loan, and supercharging our progress by debt recycling.

What you said about laziness is so true. We spent a few years just doing nothing apart from paying down the mortgage. That was such a missed opportunity to create more wealth by investing. We could have been in a better position today if not for our complacency back then.

That’s very big of you to acknowledge Ms FireMum – most people wouldn’t!

Thanks for sharing your plans, all the best with it 🙂

We paid off the mortgage first. If we’d invested in shares instead we’d almost certainly have been FI by now. Having said that, it is nice to be debt free, and interest rates weren’t always as low as they are now.

When you have a large mortgage and people around you are being made redundant it’s very hard not to resort to the certainty that comes with reducing debt.

Excellent write up, mate!

I really struggled to figure out what the best strategy for me was. I ended up building a calculator in Excel to help me work it out, and found out investing heavily in LICs/ETFs for 3 years, then paying off both our properties (investment and PPOR), then back to LICs/ETFs would get me to FIRE soonest. Weirdly specific, but there you go.

I’ve just put the calculator online for anyone interested in running the numbers for themselves: https://ughhrrumph.blogspot.com/2019/05/ughhrrumh-fire-calculator.html

Apologies for the formatting!

Cheers mate. Pretty cool you created the calc to fit your situation!

Interesting findings, whatever gets the job dones I guess. Hopefully other people find the calc helpful too.

Hi Ughhrrumph

I couldn’t download your spreadsheet from the link. Maybe I’m doing something wrong?

Hi FIRE for One,

It’s not a downloadable calc. It’s embedded in the page. You might need to give it a second to load.

Send me an email if you have trouble with it and I’ll send it to you directly.

Ugh.

Forgot to add my email! – Ughhrrumph@gmail.com

Cheers, Ughhrrumph, I’ve sent you an email.

Thanks for sharing that Ughhrrumph, it’s very impressive the detail level and how well structured your calculations are 😮

Dave, thanks again for another brilliant post, this reading for me is like attending a master class. Although I don’t have a mortgage I think it’s very important to compare what I’m doing (LICs) with the other options out there and to understand why I’m not doing those.

Funnily enough I’ve had a post about this very subject on the backburner for a while and it was going to quote the very same article from Ben Carlson! Great minds must think alike! I was going to take a look at it from a historical perspective but it was too hard to look at the different multiples of median wages for median house prices and compare across time so it got shelved until I figured out if there was a way to do a decent comparison. So far no luck.

In any case I actually came to a different conclusion as to what is best to do between investing and paying off your mortgage. For me and for a lot of people a guaranteed decent return is more important than a potentially higher but more variable/risky return. I pay off the mortgage I get a guaranteed return, I invest in shares and maybe I get a great run of returns but maybe I hit a bad sequence of returns and I end up with less than what I put in. If I had a guaranteed smooth rate of return from shares then it might well be a different story, but I don’t.

To some extent it’s about regret/risk minimisation. There’s very few people out there who regret paying off their home early, and it’s hard to see much downside to doing so. Investing in shares may well work out great and most of the time it will give you a better return, but there are also a fair number of occasions when it doesn’t. This is one of those (rare) times where I would have let my heart overrule my head and gone for the mortgage first. Plus my wife hates debt so there’s that to consider as well, happy wife happy life!

In any case there’s no right or wrong way and to some extent it comes down to personal preference.

Haha or fools seldom differ? 😉

Wow that sounds way more in-depth that my article, you should keep going with it.

Totally understand the appeal with the guaranteed nature of having a debt free house – it’s likely we’ll end up in that camp at some point. For me it’s the appeal of permanently lower living expenses!

I tend not to think about periods of returns, I simply think about likely very long run returns without being too optimistic (because what else can we go on really?). But if you’ve got a specific timeframe in mind, like getting the house paid off at the time you reach FI, that’s a different story.

Definitely no wrong answers here I think mate, and I wouldn’t argue anyone out of their choice. As long as we’re using our cash in a productive way and moving forward, that’s all that matters!

I’m in the Paid Off Mortgage camp too. I currently have the loan’s balance sitting in offset, ready to pounce if the market dips 20% but otherwise it sits there offsetting those pesky interest payments. Each month I get a ‘dividend’ of unpaid interest around $1700.

MMM or one of those guys wrote an article about how they consider their paid off house as the “bonds” in their portfolio, and to some extent that’s how I look at it… the ‘dividend’ this part of the portfolio pays is free rent forever. Hooray!!

Super is against equities and now all mortgage payments go into VAS till we hit FI. Simple as it gets.

Thanks for sharing your approach Chris. Sounds pretty good to me 🙂

Must admit, I also like seeing what our cash balance has saved us in interest each month!

Hi Chris

Ive also paid off my mortgage and have an offset account.

Thinking of selling, but also thinking of keeping it rented.

Maybe what i could do is, do what you said, (i also thought of this some time ago) if market drops like 20% pull out funds from my offset account and invest into the share market.

Still haven’t worked out whats best for me, sell the proprety and invest into managed shares or keep it and do the above.

Maybe there is a tax simulation on line with the australia tax.

Thanks, getting me thinking about what i should do

I like this approach Chris. A guaranteed 4% return from the mortgage and the chance to buy a market correction/crash if you see fit.

I’m not trying to be difficult/troll (rather trying to start a constructive conversation or learn if I’m missing something) but I’d still argue your previous thought/conventional thought that ignoring taxes, the return on paying down your mortgage is exactly the same as the interest rate, even considering compounding.

In your assumptions with the amount the $50k grows to, you’re including the initial invested amount when comparing to interest saved. I believe the comparison is earned interest/returns because in the interest saved calculation you’re not including the lump sum payment which has reduced the debt.

If the return is the same as the interest rate, the total interest paid on a loan with additional repayments is exactly the same as the total interest paid on the same mortgage minus investment returns on the money that’s been invested rather than put against the mortgage.

On another note, if you have the borrowing capacity to do so and you’ve decided you want to invest, technically, you should never invest cash when you have a mortgage due to tax rather you should pay down your mortgage and borrow the equivalent to invest as your borrowings are exactly the same but the loan split is more tax friendly. Acknowledge you touched this concept when mentioning debt recycling which is an extended version of this (saying this for some readers that may not have explored).

Thanks for the comment Kyle. Not taken that way at all, my posts aren’t the last word on anything!

Debt recycling totally makes sense mathematically no question, but there are also some behavioural things that come into play (which I went into in the post here) when people have debt for shares, rather than debt for their home, even though it’s simply a mental thing.

I get part of what you’re saying (and you definitely could be right), but some of it lost me. Honestly, the longer ya think about this stuff the fuzzier it gets! In the $50k example you save yourself $95k in total mortgage payments over the loan, and it cannot be more than that – total mortgage payments drop from $687k to $591k. And because you’re essentially removing the last few years off your loan payment schedule where the interest payable is quite low, it makes sense that the benefit would be low.

I clearly think investing makes more sense even if mortgage return does equal interest rate, for the other reasons given. But whatever someone decides, I don’t think there’s really a ‘best’ option – as long as they’re saving money and using it productively, it’s all likely to work out pretty well!

I agree with your conclusions for someone in accumulation stage. However during drawdown stage things aren’t as clear cut again, another thing to consider is that the effect on sequence of returns risk is profound.

The easiest way to conceptualise this is as follows

If you are financially independent with $1,000,000 in shares earning $40,000 per year, and you are renting at $20,000 per year. When the market crashes by 50% and your income drops to $20,000 per year you are effectively up shit creek as all your income is now going to your rent.

If you however own a home worth $500,000 and a share portfolio of $500,000 earning $20,000 per year, when the market crashes by 50% your housing is covered and you still have $10,000 to cover expenses.

But this doesn’t only happen in awful 50% bear markets, this happens in all markets.

What ends up happening in reality is during any share market downturn or subdued share market growth environment, those that own houses drawdown on their portfolios at lower percentages than those of equivalent networth but are renting. Having a mortgage magnifies the effects of volatility and reduces safe withdrawal rates.

The following article is my favourite on this topic

https://earlyretirementnow.com/2017/10/11/the-ultimate-guide-to-safe-withdrawal-rates-part-21-mortgage-in-retirement/

Good point Pat. Can’t cover every scenario obviously. Sitting on $1m on the retirement date example, it’s up to the FI individual whether they want to buy a home for the higher certainty of cashflow/living expenses or willing to take the risk and roll with the market and be prepared to plug bigger income gaps. Some people just won’t want to own for other reasons.

Rent can be easily adjusted downwards at almost no cost if need be, and ownership comes with costs that cannot, let alone the cost of moving to a cheaper house, but the point remains that there is more certainty with a mortgage free house.

>>> When the market crashes by 50% and your income drops to $20,000 per year you are effectively up shit creek as all your income is now going to your rent.

That is an assumption that would most likely not play out in real life. First, during the GFC, AFIC continued to pay a full dividend. Some of these LICs have the ability to smooth things out when the shit hits the fan. Nothing changed. If you were living away from media and were only concerned with seeing a dividend hit your bank account, the GFC would have made no difference to you if you were all in AFIC.

Second, if I was FI, I would make sure I had a good cash buffer set aside to ride out a market crash. I’ll likely continue to work part time anyway, so cash put aside plus some salary would ride out a crash.

AFI and a lot of the LICs maintained a smooth dividend, but if you’re going the index approach then this might be a bit scary. STW which is an index tracker so the equivalent of VAS or A200 dropped it’s dividends by over 50% in the GFC. http://www.sharedividends.com.au/STW

Look at the franking levels 2005 to 2008. It wasn’t pure dividends to start with. It was capital returns of some sort. Could be turnover, special unfranked dividends, I haven no idea. I know REITs went crazy with borrowing to pay capital distributions which proved unsustainable and would explain the lack of franking, possibly contributed. But dividends from Australian companies did not triple in 5 years. I think they did double (which is extreme in itself), but the rest was return of capital.

Wouldn’t expect that to be indicative of every correction. In any case, a rational person wouldn’t expect 15% growth pa in dividends to continue forever and would be expecting some correction. 3% per annum is more realistic, much more than that and it’s subject to correction.

I agree with all of that from a rational viewpoint, but a lot of people will most likely just look at what the payments have been from the last 3 years or even less and figure that’s likely what it’s going to be in the future.

Yeah I think up shit creek is a touch dramatic. Assumes dividends fall 50%, assumes no flex in spending, no cash buffer, and on the other side $3-5k per year home ownership costs (water, council, insurance, maintenance, repairs).

I’ve granted that having paid off housing and half a portfolio compared to renting and a full portfolio is more stable cashflow wise because you’re less reliant on investments, but it also doesn’t mean the other person is screwed.

I used a purposefully extreme example because it would have the effect of taking a magnifying the effect and make it obvious what it was.

For the record, I would actually be in the camp of holding debt to maximise investments until you had ‘enough’, however you define that and then paying down the house. Maximising returns through my lifetime isn’t the overall goal for me.

But yeah, as you said the point is the cashflow is relatively more stable in all market conditions when you have a paid off ppor. You may pay for this stability with lower overall returns (unleveraged houses grow slower than unleveraged share market on average).

In effect, a paid off house is kind of like a position in bonds

I agree that this is a great article and I agree with this comment. Taking an option value approach to assessing the investment makes sense when its your lifestyle at stake.

Personally, at 44, I’m doing exactly what Dave says in his sixth paragraph. Its funny how suddenly 60 doesn’t seem too far away … but then I have already got rid of the mortgage so the question is more simple. For some reason, my psychology ruled that priority numero uno was having a paid-off house.

I’m in the same boat, Tez. 44 and had pretty much belted the mortgage but big tax bills, school fees and a decision to start investing recently pushed it back out to $50k. I’m comfortable I’m doing both now. The mortgage can be a little bit two steps forward and one step back but with low interest rates and a heap in offset accounts I can handle that. The lady wife maybe not so much.

So I assume your contributing the maximum to super like I am. Can I ask, what are you looking at for your investments? I’ve got some going with robo investor Six Park but I’m thinking then next wad of cash I’d like to stick into either a LIC like AFIC or VAS. The election has me a bit skitty though.

I have just started salary sacrificing to make my total amount $22k for the year. I just want to feel my way on cash flow before upping it any more.

In terms of investing, its jlcollinsnh.com all the way for me. VTS mostly, a little VAS whenever I think the Aussie dollar is too low and IAA whenever I’m bullish on Asia. Also, I use esuperfund for our SMSF which I am very impressed with..

You’re all over it! No LICs for you then?

Firstly, I’m so glad to be back in the finance blogging community after a long hiatus and reading such a fantastic post was just the thing to get me fired up again!

Secondly, I’m in the invest while paying down the mortgage camp. In fact, I’m in the debt recycling camp, or will be soon as we are just setting up the needed structure currently, hoping to have it all fired up ready to go for the upcoming financial year. I struggled with it for a long time, especially because I found there to be not as much literature on debt recycling written up as compared to that of say “pay off your mortgage ASAP!” type literature. Will it work out well in my favour? Ask me again in 10 – 30 years time!

Hey Pia, good to see you again 🙂

There’s definitely very little content explaining how debt recycling works in simple terms, hence my article about it! Given your time-frame it has a very decent chance of working out well – all the best with it!

Interesting article!

I admit my eyes glazed over with some of the Maths talk, but that’s not your fault!

I made a conscious decision to pay off my house first before I started investing. I vaguely knew that it probably wasn’t mathematically optimal to do this, but when you leave your husband with $60 cash in your hand and 4 kids under 5 to support, suddenly security becomes hugely important!

I have no regrets doing it this way. Having a paid-off house made it possible for me to release the equity in it and move to a cheaper area, so I’ve effectively caught up to where I’d be if I’d invested from the start – and I have no mortgage expenses.

My kids are now in their 20’s and I’m looking to pull the pin on my job in 2 or 3 years. It’s now all about getting the house how I want it for my retirement and throwing the rest into investments.

You’re a superstar, Frogdancer.

Haha sorry about the numbers!

These decisions don’t always come down to the numbers, more so it’s what we’re comfortable with, so there’s no wrong answers I reckon.

I still love that story, it’s really awe inspiring! Sounds like a solid plan to me Frogdancer 🙂

Great artical, I’ll have to re-read it to fully understand and help solve my financial problem

I retired at 50 and living in Thailand where the cost of living is less, otherwise I’ll be still working.

I’ll not get a Government pension in Australia as i’ve lived and worked overseas for to long, But I’m happy with that.

I’m at a point that i have a property in Sydney that i rent out, mortgage free but with a offset account where I can drew off up-to 300k.

I do my numbers and looking at the income I receive from my IP and what i could get from a managed share like AFI.ax or VHY.ax if I sold the Ip and reinvested it, looks like the returns is like 3% better off in the managed funds compared to Property.

I wander if this is what most retired people come across where their investments were in Property, I must admit that there is a little bit of emotional factor there as it’s nice to have something solid back in Australia.

When I get an email from the property manager saying, needs fixing$$$, tenant moving out$$$, market going down$$$. makes me think weather I should sell up and invest into Share market.

(I already have 500k in shares)

Thanks for the great articals, keeps me thinking

Thanks for the comment Stephen, glad you like the blog! Nice work retiring at 50 by the way!

While I can’t tell you what to do, I think you’re correct that the income earned from dividend paying shares will be substantially higher than from your investment property. I think it’s very common for people to build a decent net worth through property and then realise it’s a pretty terrible investment for income to live on. Sadly, many people aren’t comfortable with shares so they simply stick to what they know, forgoing lots more income and often freedom in the process.

Having something solid is nice. But remember, you’ll always have a share portfolio which is very solid should you want to cash in and buy property in Oz later down the track. Personally, I’m looking forward to selling off our properties and having a decent share portfolio instead, the income and hassle-free nature of owning shares is great. All the best with your plans Stephen!

I understand going into every detail is impossible in a post but with the comparison of paying mortgage off early (and calculating subsequent savings) vs investing, wouldn’t capital gains also come into play? The house, and land, itself are an asset that (hopefully) appreciate over time so would add to its overall ‘investment gains’? My thinking is just that a mortgage sort of has 2 streams on the road financial independence – saving on interest (paying off early) and the asset itself appreciating?

I get that the asset appreciates whether you make extra payments or not, however, if you were to sell with a mortgage it would eat into your gains versus not if paid off.

Hopefully that makes sense? Haha

I’m living in eastern suburbs of Melbourne, 30 year old and looking at what to do with my savings pool (110k, able to put 1600 a fortnight into savings) – house (been given a range of 540-580k investment option from some lenders already visited)? Shares? Both – but at a lesser value of each?

Hi Jake. Good question. You can certainly look at it that way, but for this exercise I wouldn’t. The house is either going to appreciate or not, regardless of whether you’re paying the loan off aggressively or paying the minimum. These are two separate things. So adding any growth or losses when seeing how much extra repayments save you, doesn’t make much sense.

It’s true that your net worth increases if the property increases. But most often, the next house you move to has also gone up, so your not actually any better off in real terms. By thinking of repayments as gains isn’t quite right for me. Think about it, you’re simply moving money from your cash account into your home loan account. This doesn’t increase the ‘profit’ on your property purchase. It’s simply cash from one account to another.

I really can’t tell you which way to go mate, just keep reading about each asset class and try to be unemotional about it. I’ve written about our experience with property here, maybe it’ll be interesting to you. Yes leverage can be good, but be very conservative and realistic with your growth expectations. For me, I’d rather base a strategy on an income stream to reach my goals than rely on capital growth, because it’s more reliable. But you choose what suits you best. Thanks for reading!

Capital Growth of your PPOR could come into play if you 1) downsize / Geoarbitrage , or 2) switch to renting, then selling your PPOR would also be Capital Gains Tax free. 🙂 Then invest the proceeds.

It definitely could! Probably not many people’s base case scenario.

Hi Dave – if you were in your early to mid-50s and were on the way to FI, what sort of super portfolio would you be looking at for yourself? Would you still be piling into 100% equities or would you pull it back into a more “balanced” option — which usually means there’s a cash and fixed income component up to about 30% of the portfolio. Cheers

I was just looking at Hostplus options of interest again. Currently I’m in the Indexed Balanced (IB) option:

• 75% equities (Aussie and international)

• 25% defensive (10% cash and 15% fixed)

• 0.07% management fee

They have a “Balanced” option which is also 75% equities

• this option has received awards for being very good

• the 25% part has nothing sitting in cash and uses property as well as fixed

• over the long term it out performs IB after fees

• management fees are about 1%

Finally there is an all shares option (Australian shares only)

• it out performs both of the above after fees

• fees are about 1%

That depends Scott. If I’m going to get the pension as well, then I know that a good portion of my income will be fixed and very reliable. So in that case, I probably wouldn’t mind having at least 80%-90% in shares. Probably different for everyone though. If I was aiming to be fully FI, then I’d probably still go similar or slightly more aggressive, knowing that the pension is there as a backup anyway. But don’t read too much into that – it’s easy for me to say casually since it’s not the situation I’m in.

The numbers are only part of the equation… emotion the rest. But when considering risk-adjusted returns, paying off the mortgage surely comes up trumps – where else could you get such a high risk-free rate of return?

Spot on burrow! It’s not always about the numbers for most people, so no right answer for everyone.

My partner and I will have our mortgage paid off in 2 or 3 months at a holiday resort we intend to retire in. We also have a 7yr old property in Newman WA we purchased 2 years ago for 115k now worth about 240k. We get 20k / yrs rent. We now have a bit of thinking to do as we intend to retire in 4-5 yrs and need to think what we do with our joint 250k yearly income.

Hey Walshorton. Awesome position to be in, well done!

Sounds like a pretty high yielding property, though in a relatively high risk area. Whatever you do with that very hefty income, save lots of it and use it to buy more income producing assets and you’ll be headed to FI in no time!

G’day SMA,

Another great post. Thanks for your efforts. You almost convinced me to switch to buying shares instead but I will stick with the paying down the mortgage. I will be debt free early 2020 and then all that money currently going into the mortgage will be going into LICs. I am disciplined so it wont be an issue but I agree if you are not disciplined then this could be very dangerous having spare cash around. Putting all this cash into LICs should have me hitting FI in under 10 years and debt free.

Cheers.

Cheers Steven. Great job mate, that’s only a few months away!!

Discipline is a wonderful thing and it’s under-rated in our coddled Western culture. Sounds like you’re flying along, keep up the good work.

Just wanted to echo some others here and say thanks for a really great article. It’s particularly timely for me as I’m about to borrow for my PPOR, and I’m trying to come up with the most efficient strategy to keep building my dividend income. This is perfect!

Thanks very much Nick, all the best with your investing 🙂

A great article and a good reminder on how to compare real returns.

Even though I understood that it would be better with current rates to invest I have still decided to pay off the mortgage early instead.

I consider this decision as “Insurance against future rate rises”. Although in the short term that “insurance” is probably not needed who knows what can happen over a 30 year loan term.

The great part for us is the flexibility of knowing that this strategy can change easily. Especially when we feel our principle is low enough that the loan term is much shorter, and any future rate increases will have minimal effect.

We still invest slowly in some LICs/indexes also – but this is more to gain a overall education in what we will invest in heavily once the mortgage is paid off in a few years.

Getting rid of a mortgage is a huge win in anyone’s book. Interesting though process on treating extra repayments like insurance, that’s a pretty neat idea. I also like that you’re doing a bit of investing as well. I think that’s a great idea because you can learn lots as you go and decide what feels right before you put tons of money in, otherwise it could be daunting having to put lots in without having much experience first. Nice work Matt!

Hi

I have been running the numbers based on your example but can’t see to get the results you highlight. For example, after 15 years (4% interest rate, 400k loan) the balance outstanding is ~$258k.

Investing $1000 per month after 15 years is $279k. So you are ahead by $21k and if you had to pay the loan off you would pay capital gains tax as well. So the numbers aren’t as great as per your article.

If I was to just consider interest saved vs investing then also $1000 per month over 15 years at 6% only earns me ~100k gain from stocks.

Could you please clarify where I am going wrong?

Hey PB. No you’re correct mate, after re-looking at it the figures are wrong and will update the post shortly! I was convinced by Carlson’s article but the initial assumption of a 4% mortgage interest saving is correct. So it’s come full circle lol.

Hi Dave, I hope you’re well.

Do you know how or do you use any calculators/simulators for running scenarios of your money (or any amount of money) in Superannuation being invested in a period starting in the past until today?

A financial advisor suggested a super fund and sent me historical data of Vanguard Indices and what I’m trying to do is to simulate what the performance would have been if I had invested in those indices since they started paying the fees I’m about to pay. I don’t think she factored that in.

Reading “The Little Book on Common Sense Investing” is giving me a lot to think about 🙂

Hey Plutarch, great question. The answer is, no not really. I’d just make sure the fund is low fee like the ones I mentioned and you could perhaps choose one that invests in index funds rather than active management, because the likelihood is that will offer the best long term returns. Historical returns don’t tell us all that much about the future, fund fee structures and active/index allocation might have changed during that time in those funds, which muddies the water a bit. So I think focusing on the known wins today going forward makes more sense, like low fees and using indexed options where appropriate.

Thanks very much for your words Dave, that helps.

This fund invests in index funds and the fees are low thankfully.

Cheers

G’day SMA, I’ve heard you say previously that starting over You wouldn’t bother with property, the leverage aspect is overrated in your opinion.

I am starting out but don’t feel I could generate capital quickly without leveraging into property. Something both you and AFB have done quite well, then convert the profit from property into income producing shares.

Would you really go straight into shares if you started over at 18 years old, and would growth shares or dividend shares be the way to go from the start.

Appreciate your time. Forward

Hey mate, that’s true I did say that. Did I mean it? Yes, 100%. I wouldn’t have said it otherwise 🙂

To be honest, we have not done that well at all in property, as I went into in this post. And in fact, our property performance has worsened since I wrote that.

You can invest a higher sum quickly with property, no question, but that doesn’t mean higher gains quickly though. It’ll take years just to breakeven because of stamp duty, settlement costs, ongoing negative cashflow, repairs/maintenance, and later on to switch to shares you’ll have to pay agents fees and CGT. There are far too many costs to list here.

Instead of thinking of us taking our ‘profit’ out of property, it’s mostly us taking our ‘savings’ out of property, as there’s not much profit to speak of once all costs have been included.

As for growth shares vs dividend focused investing, I can’t tell you what to do. But I’ve outlined my approach and why I prefer it. To go for growth first, to reach your goal you will be 100% reliant on market movements to hit your FI number, and those swings can push you back for many years if it comes at the wrong time. Going for growth and switching later means you’d be up for some large CGT later on when selling down and buying new holdings.

With dividend focused investing, the income is relatively reliable from year to year, so reaching your goal is much more dependant on saving and reinvesting dividends. Sure dividends can go down and we’ll have a recession at some point, but the fact that dividends are generally more reliable than shares prices means that hitting FI is more predictable and you don’t have to rely on share prices to reach your goal, but instead rely on company earnings and dividends, which are more stable from year to year.

People focus on growth investing and selling down a portfolio and that’s perfectly fine, it’s just not for me. So if you want to go that route, then that’s all good, but I can’t really offer any insights there. Hope this helps Forward.

Dave, great post. You may be interested to take a look at Trilogy – https://www.trilogyfunds.com.au/ – they have the same pooled lending product as Ratesetter but for Property. They paid 7.7% return last month. The return has ranged between 7.5% – 8% for the past decade and I have been investing there for over 2 years alongside my equity portfolio.

That said, I’ve been doing a bit of reading on pooled lending products though and I must say that I’m a little worried about what might happen when the inevitable downturn happens, given they are a new asset class that hasn’t been tested by a downturn yet and seem to have a large liquidity risk – i.e. when defaults start to increase will a cash run occur and if so, won’t that mean that the pooled product provider will have to default?

This is one of the papers I read on the mortgage market: https://www.brookings.edu/wp-content/uploads/2018/03/5_kimetal.pdf

Negative outcomes for unsecured loans and business loans would likely be magnified when compared to property-backed loans…

Also, I’m working on a calculator that tries to pin down the right time to stop saving in non-super investments and transfer across to saving in the super pool – would love to share it with you when I get it into shape!

Thanks for the comment Kurt.

There’s no question that in a downturn defaults will rise from where they are now. RateSetter have a provision fund which should help to some extent and they can start taking higher up front fees from new borrowers if risks start to rise, which may also help further. But the truth is nobody knows what the next downturn looks like and what that means for loan defaults. Also RateSetter’s loans are a mix of secured and unsecured loans.

A cash run cannot occur with RateSetter as you are locked into a loan contract. You may access funds early but only if there is a new investor to take your place. RateSetter is simply the middle man which arranges the loans and takes a cut in the middle, so they won’t be defaulting. I can’t really say anything for Trilogy as I’ve never looked into them before.

This was a fantastic article. Really great and helpful advice for those who aren’t quite sure where to place their money – LIKE MYSELF :D. A bit about me, I am a 28 year old married female, with a $600k mortgage – (outer Melbourne). Combined income of $140k post tax. My husband and I are pre-kids, so we really want to think about multiple income streams, but I have been ‘umming’ and ‘ahhing’ about where to invest our cashflow. Option a. Increase the existing mortgage repayments from double to triple per month. Option b. Deposit another lump sum into our LIC account. Option c. Increase super repayments. We are both quite young, and idyllic – and would like to retire before 60, and after reading your article (and other posts from AfamilyonFire), I am confident that investing longterm is looking like the best option for us right now. I have been reading about LICs and ETFs all day, and noticed that some people are diversifying their share portfolio by buying both shares in Australian LICs & international ETFs (the word Vanguard gets mentioned ALOT). I’m wondering if diversifying our shares is the better option, or should I keep all my eggs in my trusty AFIC basket. (I’m not expecting you to tell me the answer here, nor would I hold you accountable for any advice, but would be greatful for your opinion on the matter). Essentially, for a rookie such as myself – my sole purpose is to invest in the benefit of compound interest. Does compound interest still work in the same way even you diversify your share portfolio with both Australian & overseas shares?

Cheers Edwina!

Out of those options, Super is the least attractive to me for anyone near the age of 30 and looking to retire earlier than the standard 60-65. So I think investing and paying down the mortgage are both good options to focus on.

As for international shares, yes compounding works in the same way for both Aussie and international shares. The difference is, in Oz more of your returns will come from dividends, and overseas more of your returns will come from capital growth. People argue capital growth is more tax efficient, but in Australia dividends are taxed extremely favourably so you won’t be paying any more tax than investing in overseas shares.

I think it’s up to each of us to decide what the ‘better’ option is for us and our own situation – essentially what we’re comfortable with. If you’d feel more comfortable including international shares for diversification then it’s probably a good idea.

You guys are on very good incomes, so make sure you’re making the most of it by saving as much as you can, then if kids come along later and income is lower, you’ll be in a much better position because you saved hard early and got compounding working for you. Hope that helps.

In case it helps Edwina, in the past I have agonised over whether to invest internationally and if so, how much… in the end I’ve decided that my outside-superannuation investments will be Oz shares (VAS) and my inside-superannuation investments will be international shares. I can’t remember why exactly I decided that, but I have a strong inkling it was to do with the complicated tax situation that applied if income was earned on international shares. I could be completely mistaken, but that’s how I’ve set it up. I keep my allocations 50-50 (that is, if I have $50k worth of VAS and $150k in super, I’ll split my super up so it’s $100k international and $50k Oz) and rebalance occasionally.

It seems silly to not have an international allocation of some kind, and to me it makes sense to have that in tax-favourable super where the super company can worry about fees, etc.

Hi Dave,

Great article , again.

I have a “WWYD” Q for you (Yep, not advice). Have been doing heaps of reading.

Situation : I am 35 and husband is 45. Have around 270k owing on 800k house. Very small share portfolio of 4 stocks bought in GFC. I was going to start adding much more to that in EFTs and LICs, but now thinking since hubby is only 15ys away from being able to access super, would be better to salary sacrifice the max amount, and switch from AustSuper to one with lower fees.

WWYD?

TIA!!

Thanks for reading 🙂

Interesting scenario. In that situation, if I was expecting it to take at least 15 years to reach FI anyway, then I would probably go the Super route, keeping in mind the risk that the access date could be pushed back. Other than that I think I’d probably aim to pay off the house too, so that in the event that Super access date is pushed back then part time work in the interim would probably be enough to live on – essentially a few years of semi-retirement until full FI kicks in.

That’s exactly what I was planning, thanks! Now busy researching super funds.. Thanks for your input 😀

Hi Dave,

Interesting reads. My situation currently payed of two properties with the first one had a push back after a divorce. Smashed out two loans in 7 yrs but currently only own one. Age 50 single dad with two kids. Was looking into a investment property or topping my super. Not sure which would be best to have FI . Shares can be volatile while property can have continually outlays. Guessing I will continue reading blogs to figure out what will be best for my situation. Enjoy the reading, great site.

Thanks Craig.

Thanks for the comment Craig. Awesome work on those home loans!

I would probably be looking at super/shares and starting to build some sort of passive income. Even paid-off property can have pretty woeful income after all costs. Happy reading, and all the best 🙂

Great post! I wouldn’t be so hasty to dismiss the benefits of superannuation even for young investors in our 20s though. Sure, if the aim is purely FIRE and wanting to retire as soon as possible then superannuation isn’t the best vehicle for the young. However when the goal is long term FI, not just retiring early, the tax benefits of superannuation shouldn’t be dismissed, particularly for higher income millennials. My marginal tax rate is 45% – sometimes can knock it down to 37% with deductions and accounting. But not high enough to be hit with Division 293. So being taxed at 15% in super is a good 22-30% saving, which can then be invested in indexed options within super and continue to grow. Even though this money isn’t accessible for another 30+ years, there is no reason that this pool should be foregone as long as you also are able to have a high savings rate and strong investment plan outside of super at the same time.

Thanks NF, appreciate your comment. You raise a very fair point. Not everyone would approach things the same as me, especially if they’re looking at retiring a bit closer to regular retirement, as opposed to 25-40.

I tend to be an all-or-nothing kinda guy, so prefer to focus 100% of possible dollars towards FI sooner. Even if a high savings rate could be sustained in combination with extra super contributions, I’d still opt for FI sooner focusing on personal investments. Super is always there to be added to later. Probably also depends a little on one’s priorities and how quickly they want to reach FI.

Absolutely! My priorities admittedly are different, I am only 27, I do enjoy my job and am not looking to retire super young. My aims with FIRE is to be able to work part time from my mid 30s and be retired by my mid 50s – and to have a tidy nest egg both inside and outside superannuation! And yes it’s true that super is always there to be added to later, it just makes more sense to me to add it there while my taxable income is high and so the discount is actually a big saving.

Ahh totally understand, thanks for clarifying 🙂

Hi Dave,

Great article and appreciate you shedding light on what can be a very contentious topic haha! Of course everyone has their opinions on where to invest but I think your pretty much on the money here (pun intended!). Personally I max out my Super contributions (max $15K concessional contributions) as well as keep a healthy offset in my investment property mortgage offset account (emergency fund) and then the rest goes straight into ETF/LICs spread between AUS, US and total world markets. If i get a windfall or unexpected cash, then I lump sum invest it straight away,

Cheers, Capt. FI

Good stuff Captain, thanks for sharing – makes sense to me 🙂

Great post !

Is the assumption that this is your home and not an investment property?

If you are paying the mortgage for the house you live in.. the interest you are paying isn’t tax deductible.

Does this affect your investment strategy at all?

Thanks Mattia. Yes, I’m assuming it’s your home, though the math doesn’t really change for paying off an IP. Where the interest is tax deductible, you may then receive less benefit than by paying off your home, so the maths would again favour investing rather than paying down debt. Hope that makes sense.