By now it’s well known that my philosophy is to invest for growing income. And when I review various LICs, I take a look at their performance figures. But the most important figure, to me, is how much the company has been able to grow its dividend.

Mostly, I’ll use the figures I can find to make a 20 year chart. Ideally, we could look back longer than that, but the data isn’t always available. However, I did manage to find a 60 year example while working on the Milton review.

In the case of AFIC and Argo, I managed to find 25 year and 30 year figures, respectively. Unfortunately, or fortunately (depending on how much you enjoy it), it required some extra number crunching! Apologies now for the non-number oriented folks.

You can find the dividend history for each company on their websites. The figures are relatively straightforward in recent times, but back further it’s a little trickier.

These days the company just pays a cash dividend. But each company used to also issue extra shares – known as a ‘Bonus Issue’ – paid to shareholders along with the dividend.

In a way, this is a form of ‘special’ dividend. And these Bonus Issues meant the shareholder received more income the following year, even if the official dividend-per-share remained the same.

So the dividend figures actually understate the cashflow shareholders have received over that time.

What to do?

Well, to find the real figure, I’ve gone back to 1986 (in the case of Argo), and pretended someone bought shares at that point and simply forgot about them.

Let’s see how the investor fared…

From the Share Issue and Dividend History pages, we can see a few things;

In 1987, an investor could spend $1000 and acquire 400 shares of Argo, at roughly $2.50 each. The dividend paid in 1987 was 11.5 cents per-share, giving the investor annual dividend income of $46.

Roll forward to today. Over the years, there has been 6 Bonus Issues by Argo. Each resulted in this investor being given additional shares by the company, in addition to his dividend. So after starting out with 400 shares, he now owns 813 shares.

Also, its important to note, this is without ever purchasing shares again and without reinvesting any dividends.

His 813 Argo shares paid him 31 cents per-share in 2017, giving the investor an annual dividend income of $252.

This means, when adjusted for bonus issues (which it should be), dividend growth over 30 years was 5.83% per annum. And our old friend, the RBA Calculator, says inflation over that time was 3% per annum.

As a side note – with shares in Argo now priced at just over $8 per-share (at the time of writing), we can also see capital growth over that time was 4% per annum.

Now let’s repeat the exercise for AFIC. Unfortunately, AFIC only has data available going back to 1993 for dividends. Here is the dividend history, and the history of shares issued for those of you playing at home (anyone?).

Our investor buys $1000 worth of shares at the start of 1993. He acquires 568 shares at a price of $1.76. So you know, I’m using the DRP price for this exercise as it’s usually very close to the actual share price.

AFIC were then paying a dividend of 10 cents per-share. In the first year, his investment would have produced an income of $56.

Over the years that followed, AFIC had 2 Bonus Issues, where our investor would have ended up with more shares and a higher future income, without doing anything. So after starting out with 568 shares, he now owns 687 shares.

Again, this is without ever purchasing shares again and without reinvesting any dividends.

The investor’s 687 AFIC shares paid him a dividend of 24 cents per-share in 2017, and it appears likely to stay at that level in 2018. Now his parcel of shares produces annual dividend income of around $165.

This means, when adjusted for bonus issues, dividend growth over 25 years was 4.42% per annum. The RBA Calculator shows inflation over that time was 2.5% per annum.

In addition, the value of AFIC shares has increased from $1.76, to $6.16 (at the time of writing). So this means capital growth over this 25 year period, was 5.14% per annum.

Around the time I was taking notes for this blog post, I stumbled upon some other data, purely by accident.

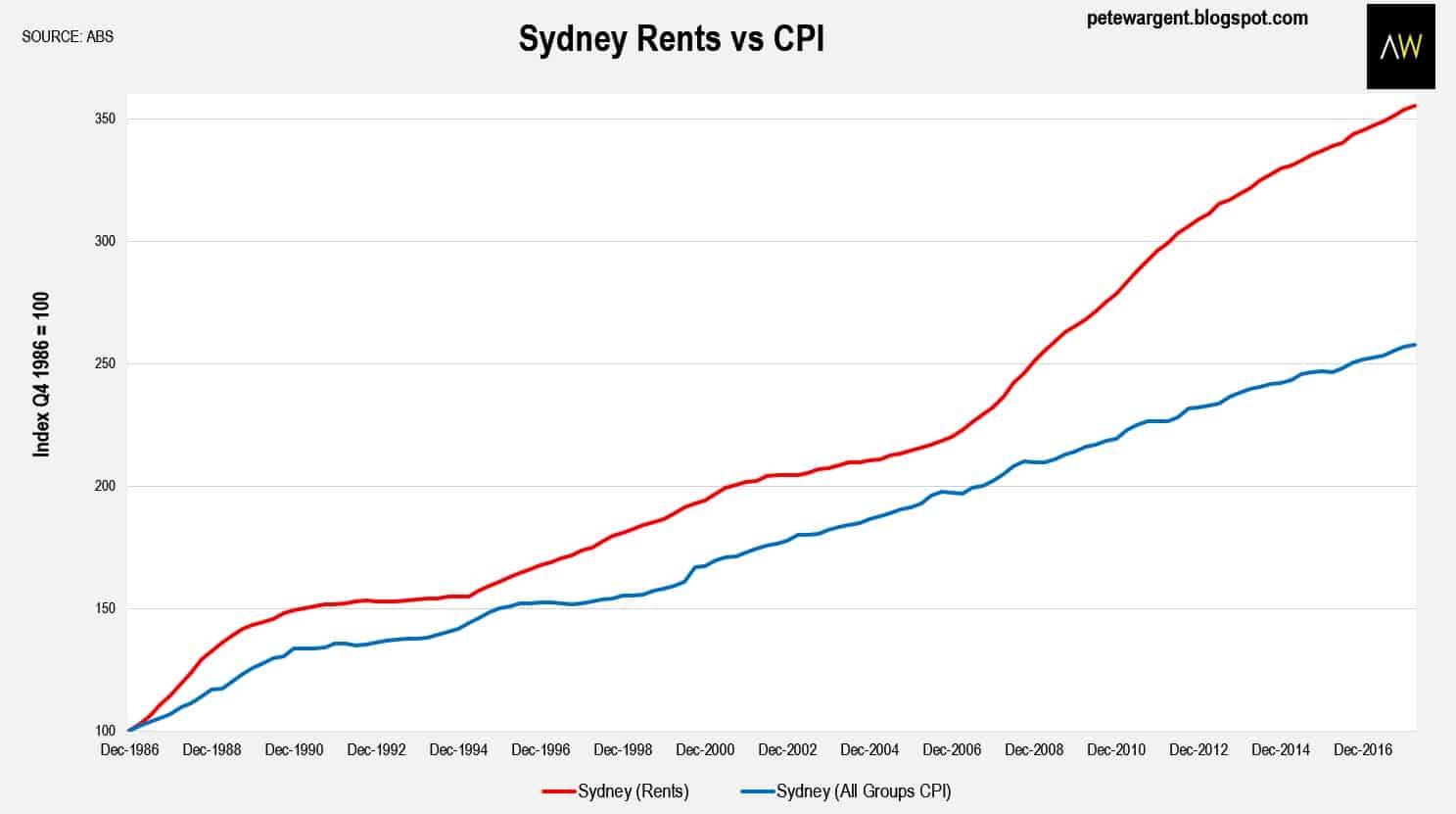

While I can’t find the precise article it came from now, Pete Wargent was discussing rental growth over time. And he kindly posted this chart of Sydney rents versus inflation, since 1986.

Note – this is not in dollar form, but indexed to a starting value of 100.

As we can see, from a starting base of 100, the price of Sydney rents has gone up to around 355. This means rents have grown at a rate of 4.31% per annum since 1986. And remember, inflation was around 3% per annum, over the same 30 years.

That’s pretty good. But not quite as good as Argo’s dividend, which grew by 5.83% per annum.

Or, if we compare it to AFIC over 25 years…

Sydney rents were at around 155 points on the chart, in 1993. And in 2017, sit at around 355. This gives us a rental growth figure of 3.37% per annum, over the 25 years.

AFIC’s dividend growth was 4.42% per annum.

Not to mention the franking credits along the way. And the maintenance and repairs required to keep the Sydney property habitable. This part is often forgotten. It’s definitely not optional.

While rents and prices may grow solidly over time (prices more-so), there’s a certain amount of upkeep or ‘reinvestment’ that is required, just to keep the property in a liveable condition, without adding value.

So, either you spend additional money on repairs and upkeep to maintain market rent, or your property will become completely undesirable to tenants and eventually you’ll be getting no rent at all.

What would the rental growth be if you didn’t reinvest some rent to maintain your property? Probably not much.

This means the difference in income growth over time is quite a bit larger, as the property owner has to cover these costs, naturally resulting in lower growth in free cashflow.

In contrast, the dividend investor is free to spend their entire investment income on whatever they see fit.

We’ll save the capital growth conversation for another day. I have little doubt that Sydney property prices have grown at a faster pace than Argo and AFIC shares over that time, for a number of reasons.

But what concerns me these days, is an asset’s ability to provide an increasing income stream over time. Ultimately, this underpins its value anyway and leads to capital growth, as the intrinsic value of the asset has increased.

What does the future hold? I don’t know. But I’ll take the hassle-free, and likely stronger growing income from the likes of AFIC and Argo.

Not long ago, we spoke about the market crash that is inevitably coming at some point. Since then, I’ve been doing a bit of extra reading on the topic.

I found the following articles helpful in learning how to think about downturns, what to expect, and putting it all in context…

There’s this one on 10 Bear Market Truths. This one on how we think about crashes. Then expecting losses. And finally, an article on all-time highs in the market (which is pretty suitable right now).

Each article is from a blog I highly recommend, A Wealth Of Common Sense. It’s US based, but the writer, Ben Carlson, does a great job of sharing lessons from the history of markets and investor behaviour, among other things.

And here’s a couple of other articles I thought were pretty cool…

Don’t underestimate the value of dividends.

Big Oil is investing billions in renewable energy.

The City of London will be using 100% renewable energy from October 2018

Originally, this article was just to share the adjusted dividend growth figures for AFIC and Argo. But when I stumbled across the Sydney rents example, I thought meshing it together would be interesting. Especially since the time-frame was exactly the same.

This isn’t an either/or debate. Nor is it a beat-up on property investing. I just thought it was interesting and figured you might too!

Both asset classes can be excellent and each will likely provide an income that grows a little quicker than inflation over the long term.

In any case, we need to find our own investment strategy that we feel comfortable with. And importantly, one that meets our personal goals.

At the end of the day, people who continually save and accumulate quality investments over their lifetimes will have little to worry about, except what to do with all the proceeds!

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Great Post! I really like this! It is easy to think not much is happening with my LICs. The income growth isn’t noticeable over a short time frame. The long term dividend growth, now that is something to smile about!

Thanks for highlighting this!

Thanks mate! I always prefer to look at the long term data to put this stuff into better context 🙂

Re: In 1987, an investor could spend $1000 and acquire 400 shares of Argo, at roughly $2.50 each. The dividend paid in 1987 was 11.5 cents per-share, giving the investor annual dividend income of $46.

Roll forward to today. Over the years, there has been 6 Bonus Issues by Argo. Each resulted in this investor being given additional shares by the company, in addition to his dividend. So after starting out with 400 shares, he now owns 813 shares. His 813 Argo shares paid him 31 cents per-share in 2017, giving the investor an annual dividend income of $252.

If my maths serves me right, That means if you had $500k in shares in 1987 you would have received $23k income. Fast forward to 2017 and that income would now be $126k per annum. That is staggering!

That right there is the power of dividend investing.

Hi John – yes that sounds right to me. Thanks for the example.

Dividend investing is quite boring in truth, but it is sneakily successful over the long term. The compounding income is quite incredible!

Ahhh and add franking credits into he equation and there is 30% rebate benefit added to he equation whether in the form of a tax saving or a cash bonus.

No wonder peter thornhill doesn’t know what to do with all his dividends ????

Haha yep. Hope to have that problem eventually myself!

Thanks for sharing your thoughts on this Dave. Being a Frenchy, I had access to some studies on Paris real estate price from 1200!! Funny stuff 🙂 (not as much as the Prime Minister “delicious” wife though).

Comparing the return on investment from 1850 (there is a French government study on this) to today gave an interesting picture of the annual return above inflation with c. 3% for government bonds, 4.6% for Paris real estate and 6.6% for French stock market (and 6.6% for US stock market) with prime real estate faring pretty well during market crash vs household available income.)

But it did indeed appear than shares yield more than prime real estate in the long run, with less maintenance cost associated with it.

To further assess the validity of investing in prime real estate vs share investing, I guess you also have to consider:

– Tax regime of both investments (franking, tax credit on renovations / negative gearing for property), land tax

– Liquidity of investments and diversification easy with shares and harder with property

– Leverage available for property, at decent rate compared with shares

Long term, both appear to be contra-cyclical to each other which seems to be a good argument to have both in your portfolio.

Great comment, thanks for sharing that David!

I believe our market has performed the same – 6.5% or so after inflation since 1900. Prime real estate is probably a safe bet over the long term too. But the costs are always left out of any comparisons.

There’s never really a comparison that both camps (shares and property) are happy with. So we just have to use the data available and make our judgement of how returns have fared and why, and then make our best guess of what the future looks like from today.

If you’ve read my other posts you’ll know I’ve fallen on the side of thinking property’s positives are over-emphasised and it’s negatives are under-appreciated. And the opposite for shares. So I spend a bit of time highlighting what I’ve learned and what things may not be being fully considered by investors – especially where FI is concerned.

Personally, I don’t plan on having both asset classes to ‘smooth out’ the performance given they may (or may not) fluctuate at different times in the future. I think it’s about finding a strategy that meets our personal goals best and aligns with our own preferences for what we want in an investment.

Agree. Seems as if the shares/property camp is trying to convert the other party into thinking their investment strategy is superior. Go with what you understand and feel comfortable with I say.

Great article! Rental income net of costs is pretty terrible.

Went back and realised that even for the oldest two properties in my portfolio (greatest rental growth), that I’m barely breaking even cashflow wise after factoring in all the associated costs. Not to mention we’re currently experiencing abnormally low mortgage interest rates.

Property 1: Purchased 2009. Currently sitting on 9.2% gross rental yield vs original purchase price. Still barely breaking even, due to strata committee raising a special levy.

Property 2: Purchased 2009. Currently sitting on 6.6% gross rental yield vs original purchase price. Still barely breaking even, due to tenant issues, repairs and maintenance.

Cheers Jack. Thanks for the info.

That’s interesting stuff – it’s always good to go back and look at how much things have cost. I still underestimated this stuff despite trying to be conservative. Costs just seem to come from every direction. It’s likely that most property owners, whether investor or owners are drastically underestimating what the true costs are over the longer term.

Damn strata, we just finished paying some special levies too. It’s slowing down the growth of our LIC portfolio 😉

You raise a great point about low rates. The out of pocket costs are currently about as low as they can be. Then we’ve got the rollover to P+I which is another demand on cashflow. Strong rental growth doesn’t seem very likely to make up for it. Stagnant prices for a while may help. For us, we have a few IO loans rolling over in the next 2 years which we’ll have to cop (no serviceability to get around it).

Thanks for sharing. I like to see long-term comparisons like this – it helps to keep things in perspective.

Totally agree Miss B, thanks for reading.

Great post. I have 7 investment properties but rather than keep adding more I am thinking dividend investing may be a better option. At least for some diversification. Agree with others that strata, repairs, etc really eat into rental income.

In the June 2018 issue of Money Magazine they talk about advantages and disadvantages of LIC’s amongst some other income focused investments. One of which was:

Advantage – LIC’s can trade at a premium or discount to their Net Tangible Assets (NTA) which they have to publish every month. An LIC trading at a discount can provide a good buying opportunity.

Disadvantage – If a LIC is trading at a discount this can also be an early warning sign of problems.

Does the premium/discount factor in to your decision on which LIC to invest in or when to invest in it? Or does the long term time frame make it irrelevant to you?

Nice job with your investing so far – adding some income-focused shares can’t hurt.

Well LICs which trade at a discount which becomes substantial usually do have issues. That would be extremely unlikely for the LICs I usually talk about here. These companies have been around for many many decades and have a very large and loyal shareholder base. And because their portfolio’s are similar to the market as a whole, it’s unlikely they would trade at a substantial discount.

Premiums/discounts are only a big deal if they become large in my view. If it’s only a few percent here or there I don’t really care too much. A long timeframe does dilute any premium paid subtantially, but obviously a discount is better! Over the long term, it tends to even out. Sometimes you might pay a premium and other times a discount. It’s another form of dollar-cost averaging in a way.

Some people choose the old LICs when they’re at a discount or trading around NTA, and at other times they’ll buy the index fund. Probably not a huge difference either way, just personal preferences. I’ll write a post on it at some point!

Many people ask me how to approach investing when they start sorting their money much later in life. I guess dividend investing seems to take too long despite its long term superiority, but seriously, unless some risky speculation is entered into and a huge wave of luck occurs, then there is no answer to getting ahead quickly and making up for lost time. My advice is always to get very serious about saving rate and still use dividend investing with a tad of market timing (yes I admit to not using DRP or DCA) . Is that how you would answer?

Reaching for higher returns with speculative investments or leverage can work, but I definitely wouldn’t recommend it as a strategy. Boring investing like this is far, far more reliable and repeatable. People just need to suck it up and build patience and discipline to go with their newfound savings habit. There’s no real shortcuts. That’s not a popular answer though!

Saving hard is the best thing anyone can do for their finances, so yes I’d agree there. But I would also tell people to dollar-cost average and reinvest dividends. History shows that is the superior outcome most of the time and for most people that is the easiest approach to adopt and it avoids the complexity associated with looking at share prices and wondering when to buy. None of us know the future so we’re all just guessing – may as well keep buying. Market is more likely to go up over the long term than go down. Short term direction is anyone’s guess, so why bother 😉

Fantastic post Dave – provides a really great perspective on LICs in the broader context of other investment assets. I’m glad you stumbled across that Sydney rent data 🙂

You’ve really just reinforced my preference for shares here (like you I have nothing against property – it just seems to dominate the Australian investment landscape!), but I must admit I’ve never truly appreciated the strong performance and very long-term nature of some of those LICs. You’re really giving me some new insights here which I appreciate!

Cheers,

Frankie

Thanks a lot Frankie, glad you find it of value!

I guess the dividend growth approach with shares/LICs is so boring it really flies under the radar as a means of building wealth and investment income – something I’m trying to change 🙂

Dave please don’t take this as a criticism, you add a lot to this community. Always look forward to your posts.

Would it be fair to say that being retired for a year you derive the majority of your income from your 7 or 8 investment properties, but are actively building your LIC portfolio and advocate passionately for this type of investment?

I guess where I’m curious – is how much LIC do you actually have – 200k, 500k etc and what proportion of your day to days are actually funded by them as opposed to your properties?

I am building a mixed portfolio and also currently property heavy, working to change that ratio.

Thanks for the comment Rc1. Good question – it’s a common one.

The answer is no – we don’t live on income from property. At this stage, we currently only have around 15-20k of investment income and all of it is from shares. The remaining properties are still negative cashflow, some by quite a bit.

We are actually living on capital from slowly selling properties, while we also invest some into shares each month. So over time, we have less and less outgoings (property) and more and more income (shares). I wrote about this process a while back in this post. I’ve also written about our property experience a bit more here.

Hopefully these posts explain a bit more. We’re receiving nothing from our properties which is why we’re taking our equity out – to build a proper income stream.

It’s perhaps not a common approach, but it’s the one we find ourselves in, and it’s working for us. It minimizes Capital Gains Tax, lets us dollar-cost-average into shares, and helps us choose which property to sell at which time – rather than an all-at-once approach. It will probably take 7-10 years to be fully converted from property to shares (mostly by choice).

We also find ourselves each doing some enjoyable part time work at the moment too, which means a bit extra cash to cover property outgoings or purchase shares.

You’re right I do advocate passionately for investing in shares for income, because of the things I’ve learned from investing in property and how it all fits together with early retirement which I don’t see spoken about much.

I would rather the price of shares actually goes down so I can buy more at lower prices, so I’m definitely not trying to push my message to lift the market! Hope this all makes sense.

Great post! Thanks for putting it together and including the Sydney rents.

Loving the blog overall too, well done.

Thanks a lot kdm! And appreciate the feedback 🙂