While I consume little news these days, I still manage to come across various stories along the lines of…

The economy is sluggish and headed for recession. Secure full-time jobs are rare and hard to get. And wages growth is stagnant, while the cost of living continues to rise relentlessly.

Today we’ll take a peek into these topics and I’ll offer some thoughts on actions to take in the current environment to help cement your path to Financial Independence.

Now, I don’t typically buy into the negativity in the media. But it’s no secret that the economy is growing a little slower than normal at the moment.

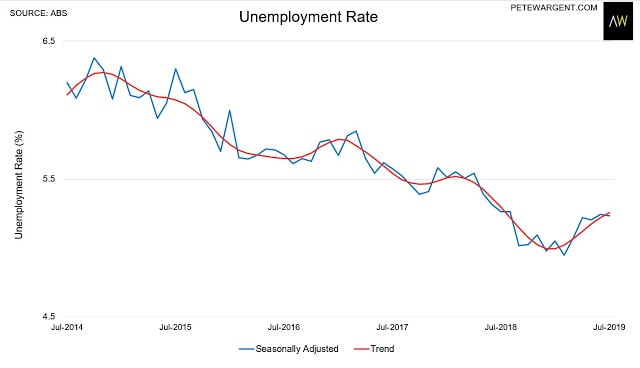

And seeing this, the Reserve Bank of Australia (RBA) has lowered interest rates twice so far in 2019, with more rate cuts possible. This attempt to stimulate the economy is to aid in getting unemployment down (not that it’s even high) and wages up.

The sluggish economy has been felt more keenly here in the West than in the eastern states. So the rate cuts are most welcome!

On top of this, some jobs are being increasingly casualised, as companies look to hire workers but retain more flexibility than traditional full-time employment. And while this sounds like a negative for those working and saving right now, there is a positive side to casualisation, which I’ll touch on later.

But the jobs market is not as bad as you might think. Here’s some perspective from Pete Wargent via his excellent blog…

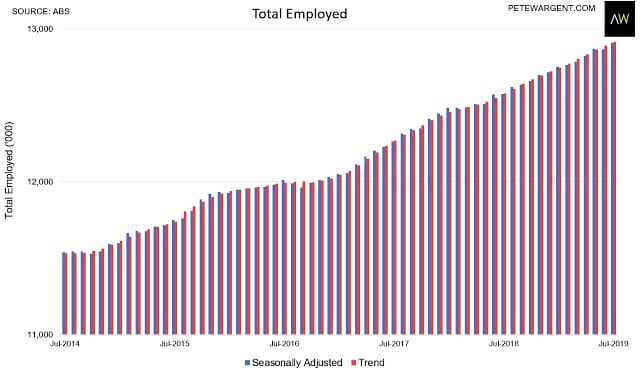

“Annual employment growth accelerated to +332,600, or 2.64%, taking total Aussie employment to beyond 12.9 million for the first time. For some perspective on all the apparently gloomy news out there, the economy has added a thunderous +910,000 jobs over the past three years alone.”

So things have improved quite a bit over the last 5 years, and have simply weakened a little in the last 6 months. But it’s true that the economy is hardly flying.

Despite what you hear, this doesn’t mean a recession and massive job losses are a given. We may just see a period of slow growth, before lower interest rates, tax cuts, a lower Aussie dollar and other things help to get the economy moving again.

By the way, a recession doesn’t have to be a bad thing – I’ll explain why in a minute. But now let’s look at another hot topic – wages growth.

So, depending on the journalist, wages are either ‘stagnant’, ‘stalled’, ‘not keeping up’, or ‘stuck in a rut’. Is this actually true?

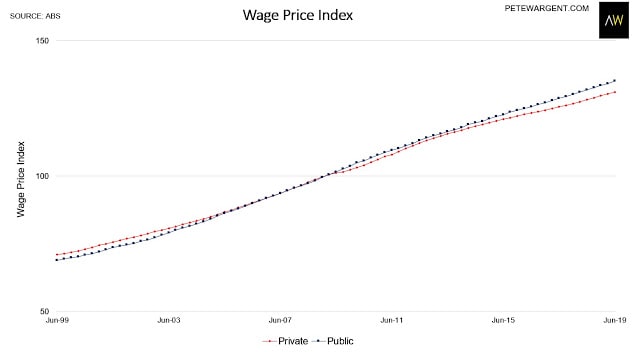

Well, over the last 12 months, wages grew at a rate of 2.3%. That doesn’t sound too exciting, does it? Wages have certainly grown faster in the past. Here’s the Aussie Wage Price Index for public (govt) and private sectors over the last 20 years…

Going by emotive media articles and gossip, we’d be expecting that line to be completely flat! And we can see the trend has indeed flattened out a little in the last few years. But overall, wages have continued to rise.

In truth, the pace of wages growth doesn’t mean much by itself. What’s more important, is when it’s measured against inflation. That’s how we can get an indicator of whether our real wages are actually growing or not.

If you’re getting a 5% wage increase, but inflation is currently running at 5%, you’re really no further forward. On the other hand, if you received a 3% increase, when inflation is 2%, then you’re better off in real terms.

So context is very important. Now, let’s look at the other side of the coin, inflation.

The cost of living – what about that?

The RBA targets annual inflation of between 2% and 3%. But in the last few years inflation has been regularly below 2%.

Over the last 12 months, the RBA has the Consumer Price Index (CPI) growing at 1.6%, as of June 2019. Pretty low. And if you remember, the Wage Price Index increased by 2.3%. This means real wages actually grew by 0.7%. In fact, it’s a similar story over the last ten years…

And that’s assuming you simply accept any price rises and don’t optimise – which should be your natural reflex to price increases!

Some people believe the inflation numbers aren’t accurate, and that the cost of living is ‘out of control’. I don’t buy this for a second. I actually think the inflation estimates are overstated!

But it’s not just me. In fact, in its own paper, the RBA says that the CPI numbers are upwardly biased in several ways and likely overstate actual cost of living increases, by as much as 1% per annum.

CPI assumes you don’t shop around for deals or make substitute purchases. CPI ignores the discount wonderland of online shopping. CPI is also adjusted to include lifestyle upgrades.

The RBA’s paper also confirms something I had suspected for some time…

“Over time, individuals may not compare the cost of achieving the same standard of living, but rather that of a ‘reasonable’ standard of living. Real consumption per person has risen substantially over time, indicating that living standards have increased. Thereby, it is likely that the notion of what is a reasonable standard of living has also increased, as households have become accustomed to consuming more goods and services and those of a higher quality. As a result, perceived increases in the cost of living partly reflect the cost of attaining a higher standard of living for many households.”

In other words, people feel as though living costs are going up. But often, it’s the cost of their desired lifestyle which has increased.

As you can imagine, CPI is likely even more overstated for many of us in the FI community. We’re known to raise a quiet middle finger to inflation, and shop around more than the average consumer. We’re also more likely to delay gratification and less likely to feel the need to constantly upgrade our cars, phones etc.

If you’re keen, check out my post ‘The Real Cost of Living’, where I dig into inflation, wages and affluence over the last 50-100 years. Lots of good nuggets in there, and even a rant, so check it out!

Your cost of living can go up every year. But it doesn’t have to. Much more is in our control than we think. We control where we live, what we eat, what we buy and how we entertain ourselves.

I think many of us are simply looking backwards to the ‘good old days’, and bemoaning an economy that has been growing for nearly 30 years!

We’re anchoring to years past when inflation and wages growth was higher. But remember, wages growth needed to be higher just to keep up.

Inflation is now much lower, at under 2%, so of course wages growth is low. Yet, wages growth is still more than inflation. Why should it be any higher?

We humans are strange creatures. We prefer larger numbers to small ones, even when it makes no rational sense. Many would prefer a 4% wage rise with 4% inflation, compared with a 2% wage rise and 1% inflation. That’s despite the second option resulting in a higher real income than before.

Firstly, that things aren’t as bad as they seem. So recognise this and don’t buy into the negativity. Yes the economy is a little slow right now. Yes, wages aren’t growing that fast.

But with inflation so low, we still have more income at our disposal than we’ve ever had before. And if we don’t, then it could just be down to our own situation and it’s worth looking at the choices we’re making.

In the last 100 years, real incomes have grown so much that we now spend only a fraction of our wage on basics like food and clothing, compared to more than half back then. And our bucket of optional extras has expanded enormously.

Okay, so housing is expensive. That’s no surprise considering we have, on average, the biggest homes in the world, despite less people living in each house!

Buying your ideal home can quickly destroy your dreams of Financial Independence. But what’s forgotten is that buying housing is also a choice, which more than any other, should be weighed carefully. Especially when that decision involves half a million dollars or more of debt.

Here’s something strange I’ve observed: The hardest part about renting isn’t having to move, or dealing with inspections and property managers. Because that stuff’s no big deal. Instead, the hardest part of renting is dealing with people who think you’re insane for renting!

Anyway, my point is, whatever our situation, we need to take complete ownership for that. Nobody can sustainably improve your situation but you. Excuses and reasoning make us feel better in the short run, but ultimately, get us nowhere.

Maybe you believe things are really tough out there and you want to ensure you keep making progress towards your goals. In that case, my number one recommendation is to increase your savings rate.

Seriously. If there’s a recession coming, and there’s a chance of job loss, having lower expenses and more savings will help immensely.

And with wages rising at a pretty slow pace, guess what? Saving more money is the fastest way to strengthen your current financial situation. In fact, it always is.

By all means, keep cash on hand as a safety net in case of job loss. But after that, our savings can’t just sit around – we need to use our money productively! That’s why…

We need to continue putting as much money as we can into investments which will go out to earn more dollars for us. It sounds simple, but it’s very powerful.

And if there’s a recession and shares plummet, that’s actually the best thing that could happen to us when we’re trying to build a portfolio! As we keep buying, we’ll be scooping up more and more shares for the same dollar investment each month.

This is provided you aren’t unfortunate enough to lose your job. In that case, work your arse off to get a new one, and start saving and investing as quickly as possible.

By the way, please ignore the doom and gloom forecasts. Nobody knows what’s going to happen, or when it will happen. The experts have no idea, and neither do I. The difference is, I know I have no idea… while some are delusional and convinced they can see the future.

Or as Warren Buffett puts it, “Market forecasters will fill your ear, but will never fill your wallet.”

Lastly, if growth and market returns end up being slow for a while, then dividends are arguably an even more important source of return going forward. Either way, keep investing and focus on the long term.

If you haven’t already, this is a great time to get a better mortgage rate. Ring up your bank, or do some shopping around and get your mortgage rate as low as you can. That could be a couple of thousand dollars per year for very little work!

You can also take advantage of the current low rates to make extra payments and smash your mortgage much sooner. I know some readers are already doing this.

Consider buying a long term home if you’re renting. With interest rates heading towards 3%, even adding yearly ownership costs of 1%, home ownership is getting pretty close to the cost of renting in many places. Add to this, that prices have fallen in Sydney and Melbourne over the last 2 years, and have been flat or falling for a while now in Brisbane and Perth.

But if you do buy, stay there! The costs of selling and moving are eye-watering. You’ll be out of pocket many tens of thousands each time. This point is often overlooked, but I can’t state it strongly enough.

Of course, your other option is to pay the bare minimum on your home loan, and invest all your spare cash elsewhere for a higher long term return. I discuss the options in detail in this post – Mortgage, Investing or Super.

Whatever you choose, each option is a win in its own way. So choose whichever option suits you best.

I was gonna say, start a side-hustle. But that term makes me cringe for some reason. Maybe it’s been over-hyped for too long?

Either way, the so-called gig economy is here to stay. Right now, you can earn money in all sorts of weird and wonderful ways, on platforms like Airtasker and others.

For those with some extra time, consider doing some casual freelance work. Everyone has at least one skill they can market. And you can devote as much or as little time to it, at the hours that suit you. Or you can simply go for a traditional part-time job.

Look at what activities and tasks you’re good at, and what you enjoy, and find a way to earn money doing that. This approach will mean it probably won’t even feel like work. And by starting with casual work on the side, you might just find a role you’d like to slip into once you hit FI.

So don’t discount this idea. It’s definitely worth experimenting with. Even if only for the purpose of testing the waters for later on.

As we can see, for all the hysteria, the economy is still growing, and our wages are still growing faster than inflation. Like always, our spending can be optimised to combat inflation and even lower our living costs, without dropping our standard of living.

It’s as good a time as any to shop around. For better mortgage rates, insurances and phone plans. We should question our current level of car use and commit to exercising more. And it probably wouldn’t hurt to trim down on eating out for a while (guilty!).

At the end of the day, saving more is always the fastest way to improve your situation, allowing you to build your investments faster and deal with any economic speed-bumps in the road with relative ease.

What are your thoughts on this topic? Let me know in the comments!

James shares his path to building a share portfolio and buying an investment property by 19. He also shares his FI plans, lessons learned + more.

This article unpacks four simple strategies which have the potential to make you an extra $600,000 richer for singles, and over $1m for couples.

Money, freedom, and a better life - delivered to your inbox

Practical insights to help you build wealth & actually enjoy it.

A great level-headed reminder post Dave.

Coincidentally, I was chatting to an older friend the other day about the topic of “the good old days” and he echoed much of your thoughts in his response. He encouraged me to look at what people had back in the good old days (we were using the 1960’s as an example) viz 1 family car, 1 neat small solid home, 1 telephone for the whole family, all meals got eaten at home, fun was free or cheap (picnics, camping, the beach, the drive-in) 1/4 acre with the ubiquitous veggie garden and fruit trees out the back …. you get where this is going?! He encouraged me to reflect on this and to peel back what ‘normal’ looks like now compared to then. He actually still lives like this (AKA 1950s style) but is up with the times as far as being well read, a good conversationalist, interested in current world news and topics, empathetic, resilient and is such a happy wise bloke.

Thanks for sharing that Phil! That’s a perfect example of the issue I think – a happy and satisfying life can be had with or without all the perks of modern life. It’s a shame many are unwilling to consider that’s even a possibility!

Great post Dave.

You know your chapter called Anchoring reminded me of the latest optimisation we’ve introduced to hack inflation. Moving onto a boat!

Even living in a marina; rent and bills have been more than halved and the payback period for the boat is about 4 years. In a few years when we reach FI and are living on anchor full time traveling around living costs will be reduced even further.

I agree totally that inflation isn’t a thing, particularly for the FI minded.

Cheers,

Andrew

Thanks Andrew – that’s fascinating!

I’ve never considered it myself, but it sounds like a pretty cool idea – and with a huge amount of freedom and flexibility attached. Very nice work mate 🙂

You say lower interest rates are a good thing. Well they certainly are not a good thing if you retire with interest rates on investments like term deposits at the lowest point in history. Reserve bank 1% and soon to fall to possibly ZERO.

Stock market over priced and with China and Trump and Brexit and your at an age where you are frightened to put your hard earned savings into shares that could drop 60% overnight in value.

Ok if your 30 but not so fine if your over 65 and dont have the time for it to recover. 🙁

I see where you’re coming from here, but can’t say I agree.

I didn’t actually say low rates are good. I said rate cuts are welcome here in WA as it should help the economy a bit. Low and high interest rates both have pros and cons. There’s an argument out there that people should not expect high interest rates on term deposits, because why should we be handsomely rewarded for taking no risk? I think there’s quite a bit of truth to that statement. If we want to be rewarded, we need to take some risk.

If interest rates go up, it’ll be because inflation is higher, so holding cash means you’ll still be no further forward, especially after tax. So hoarding cash is rarely a good idea regardless of age.

I don’t personally believe the stock market is overvalued as many say. It could definitely fall for an extended period (it always could), but 60% overnight is being dramatic.

Think of it this way, if you’re putting in money and earning dividend income from that, the lower shares go, the higher dividend yield you’re purchasing at = more income for the same dollars. And if the market goes up, then you’re becoming wealthier. It’s not all bad, depending on what you focus on. Even if the market/dividends fall, you’ll still be earning much more income than putting cash in term deposits.

Over 65s get the pension and some super, which I don’t have access to, both of which help provide a reasonable living in retirement. Combined with a small portfolio paying dividends and that makes for a great retirement. So I get that the market/current environment seems scary, but there’s a lot of positives to focus on too.

Thank you for your reply.

However “Over 65s get the pension and some super ” does not apply to him.

The friend that asked me to form my post to you is 10 years over 65 and has zero super and cannot get any pension. He has managed on Term Deposits so far but with interest rates of 1% and soon to drop to even zero , the scary at his age stock market seems to be the only way to go?

The old established LICs are returning around 4% I think?

Any suggestions for a person that has never owned a share? 🙂

There’s a post on Greater Fool today profiling someone in almost exactly the same scenario as your friend. Read it. Then read it every day till the author keels over, and I’ll be surprised if you’re not both more entertained and well off financially than you are today.

Do you mean this American one please? TIME.

https://www.greaterfool.ca/2019/09/01/time/

Well, unless I’m missing something, that would mean he has a pretty large nest egg, which is fantastic. As I see it, the options are; spend down this money if necessary without investing and then he will qualify for a pension. Or invest this money and live on the income it produces, and should this money also deplete for some strange reason, the pension is still there as a backup.

I get that people prefer not to spend their savings, but it’s really not the end of the world. Yes old LICs are yielding around 4% in dividends, plus franking credits which he will get fully refunded, so his dividend yield will be about 5.7% – that’s pretty damn good and many times better than bank interest. Even better, those dividends should grow over time. Living on cash is very dangerous because the income doesn’t grow and you’re at the mercy of interest rates, so the income isn’t even stable. Not safe at all!

The only suggestion I have is to invest the savings each month rather than all at once. Get used to buying when the market is up and down and focus solely on the reliable income you’re being paid – ignore the ‘value’ of your shares. Hope that helps.

Yes Dannie, that’s the one. Essential reading for anyone serious about their finances. His advice to the 74-year-old gentleman was invest conservatively, but invest all the same. Of course I’m not suggesting this advice be blindly followed… just that he knows what he’s talking about and therefore probably best placed to offer suggestions. Notably, he was the financial adviser of FIRE doyens, Millennial Revolution, who feature in the FIRE documentary this blog talked about last post.

Outstanding post Dave.. A solid reminder that optimising our spending and focusing on savings is one of the best things we can do in any economic conditions

Totally. Cheers Craig!

Wage growth isn’t a problem in the sector I work – community services.

Each year since approx 2013 award based employees have received two increases a year, one indexation in July along with all other award employees, and a second in December due to something called ‘The equal renumeration order’.

This has led to eye watering wage growth, particularly in the last three years where July indexations have been in excess of three percent. ERO increases have ranged from 2.2% at the bottom of scales to 3.8% at the top.

As a result new grads with little to no experinice can expect to start on 60k.

In addition to this employees can also expect an increment each year until they hit the top of their band. So we’re looking at closer to 10% wage growth for a lot of employees.

Of course in exchange for this investment the people of Victoria can expect an increase in productivity. Actually no they can’t – productivity increases are zero.

Despite these ludicrous increases the majority of my staff continue to complain of being underpaid and struggling to make ends meet. I sadly shake my head, unable to comment. And continue to raise my saving rate with every unearned pay rise I am given. If only I could refer people to your blog I might open a few eyes.

Australia is a bonkers place. In my previous life in London I received precisely one indexation to salary in my 14 year career – all others were earned through promotion etc.

Not sure of my point – just wanted to rant.

Wow that’s very interesting – appreciate you sharing that!

Maybe you can do a staff presentation on living standards across the globe and throughout history…and compare it to how they all live today lol! And you could start a reading list as part of the staff training and some of these blog posts could serve as mindset and personal finance lessons 😉

The complaining doesn’t surprise me – it’s become the norm to obsessively complain and cry hardship. Like a weird form of bonding, sympathising with each other. Most middle class Aussies (myself included) have no idea what hardship is!

You inspired me to pull out the spreadsheets and check our personal inflation over the last 4 years we have been on the FIRE trail. Year one spending (ignoring mortgage interest) was $31,763, year 4 is projected at $30,503. 2nd year and 3rd year were increases of 4% and 7%, this year we pulled it back and it dropped by 14% from last year.

Its very much coming down to how much we spend on groceries, eating out and overseas travel which this year is respectively 16.58%, 10.76% and 10.71% of total costs. Travel down 28% from last year – next year will be a big one though. Groceries down by 19.43%… thank you ALDI.

At the same time, income has increased by 18.33% from year one. Those high yearly increases are coming to an end as i think we have both topped out somewhat.

Great article and definitely our experience bears out your argument.

Awesome stuff Adam! If you include mortgage interest there would be even more deflation, as interest rates have fallen and you’re probably paying the home down too. So it’s likely even better!

Eating out and travel is huge for many people, though these seem to make it into the non-negotiable ‘basic living expenses’ category. Again great job, it sounds like your savings rate is increasing nicely!

Fantastic post mate.

Great to hear some rational comments about what is going on, rather then the over sensationalised BS the news spits out constantly.

Thanks very much – exactly what I was going for! 🙂

Hi Dave

I agree things have slowed in the recent past and there are some head winds (Brexit, trade war talk and tariffs) that causes voiltility in the markets, but when isn’t there? I remember not long ago it was Italian banks or Greece defaulting.

But its always best to remember to stick to the data rather than speculating.

Here’s a couple if other points to add to your argument about the economy not likely to head for a recession.

1. Aust capex plans for 2019-20 are up 10.7% on year ago plans for 2018-19.

Mainly driven by mining (+20.7% good news for where you are Dave), but manufacturing (+8.6%) and other industries (+5.8%) also improving. These figures demonstrate confidence that business investment is improving.

2. Investment in public infrastructure will jump to $70 billion this financial year and is likely to be maintained at that level in real terms for a further four years. These include spending on construction, water, telecommunications, electricity and social building (health, education and other public buildings) as well as transport.

So while residential construction has dropped off, infrastructure spending is likely to pick up the slack and business confidence is improving.

I think the economy will continue to grow in the near future as you suggest Dave and most businesses will continue to make profits, which means we should be right to continue to chip away at our financial goals.

Love the site btw Dave!

Thanks for the thoughtful commentary Mark, excellent!

Exactly – there is always stuff to worry about. But there is usually plenty to be positive about too. And it’s generally much more sensible (and profitable) to be an optimist rather than a pessimist 🙂

Once you’re on the path to FI, Mr Money Moustache likens finances to a video game set to easy. Honestly, if it’s still possible, every post on this blog takes the difficulty down a notch. In about four years I’ve gone from broke to essentially financially independent. It’s embarrassing how easy it is once you know the tricks. Inflation, stagnant wages, looming recession… it’s like worrying about the end-of-level boss when you know you’re going to have invincibility.

Thanks for all you do Dave… would not be clocking the game of finances without it!

Haha great comment Chris! And thanks for the compliment. I really do try to make this stuff simple and take away the need to worry, as well as shoot down some of the common excuses that get thrown around. So it’s fantastic that you’re finding it effective.

Quite a turnaround you’ve had! In fact, it would make a great case study… if you’re okay with it, shoot me an email through my contact page as I’d like to find out a bit more.

Will do

Hi Dave,

I am 38 years old and currently making 55k a year. I started investing last year and my current net worth is 180K. I am currently living in Sydney but I do feel it would be very hard to achieve financial independent if I live here as the cost of living is very expensive.

If you were in my shoes, what would be your recommendation to achieve financial independence?

Hi Sugi, well the first thing is to optimise your housing. If you’re single, I suggest a some type of share-house arrangement. If you have a partner, then you should still be able to find something acceptable for less than $400 per week (and hopefully your partner earns some income also). Aim to live close to transport so you can perhaps avoid car ownership as well. It might also be possible for you to do overtime at your current workplace, or aim for a higher paying position. And of course, if you don’t really have any special reason to live in Sydney specifically, you can of course move to Melbourne or Brisbane, both of which have more affordable housing and still plenty of jobs. Hope these thoughts are helpful!

Bring on the recession…. need to buy me some more stocks and even better yields!

Haha! 🙂

Hi Dave,

Love your work, always a really interesting and informative read.

As background I’m 66 and semi-retired and investing for reliable, sustainable income with the additional aim of preserving and growing capital, ahead of inflation.

I’ve been inspired to invest in a portfolio of LICs and now ETFs after first stumbling across your excellent site earlier in the year (thank you). It’s also prompted me to look more widely at all sorts of investing options – with a focus on defensive assets providing income that i believe could be largely sustainable over a market crash while preserving capital over the longer term. But in doing this there’s just one thing i don’t really get – why I shouldn’t just take the easy route and look at a top performing Industry Fund – paying a monthly ‘pension’, like Australian Super Choice Income or Host + equivalent. With a mix of of managed options offered to make up a portfolio from Pre-Mix (say Balanced) to DIY Aust. and International Shares that based on a 5 year average return between 9.5% (Balanced) and 12.5% (Int. shares). All managed without much hassle, at low costs – and paying a regular monthly 6%. I’m hard pressed to find other investments options across income focused and regularly paying LICs, ETFs and other funds and alternatives that provide much greater performance and regular income, without much higher risk. Am I missing something here?

I really look forward to your response – and any advice on alternative options.

Again, I love the Strong Money site, well done,

Vaughan

Thanks for the feedback Vaughan!

Interesting question. There is nothing wrong with low cost industry funds, but they don’t ‘pay 6%’ in terms of income only – some of that return will be from growth in the fund as you slowly draw it down over time, or simply some of your balance paid back to you. They invest in asset classes broadly that are mostly available to us too, like shares, property, infrastructure etc.

If you’d like the automated option, I think it’s fine, but these funds are not earning 6% income from their investments as they’re typically quite diversified, so there’s no magic in the 6% payout they’re apparently providing. I looked at the website, and they pay 6% of your balance (regardless of what the fund’s returns are) … your balance will fluctuate over the years, so your payments will as well I assume. Again nothing wrong with this, but it’s good to understand how it works.

The long term returns will likely be pretty similar with the markets they invest in – again no magic, albeit they would’ve had a tailwind from bonds as interest rates have fallen further. The issue is that these funds in ‘income mode’ are extremely risk averse so you’ll hold lots of cash and bonds, which are likely to have pretty poor long term returns, without the volatility of shares obviously, so that’s the trade-off and something else to consider.

It’s really up to you how you invest from here. As you know, a decent weighting to Aussie shares will get you close to 6% in income once franking is taken into account, and dividends will typically grow with inflation over time. Other assets can provide strong returns too, but they will be in the form of lower income higher growth, which will need to be sold down to create a higher income. Both are fine ways to do it, and only you can decide how much cash/bonds you feel comfortable with. The point is there is no free lunch, to earn more income from assets these days you have to take more risk, given interest rates and bond yields are so low.

Thanks Dave, your viewpoint is much appreciated.

Great article Dave, and thanks for the link to Pete’s blog too.

I saw at the bottom of his article he pointed out that “markets are pricing for two more rate cuts over the coming six months, while OIS pricing is maxing out at 1.50 per cent all the way out until the middle of this century” – imagine how far behind TD and HISA savers are going to be in 30 years time…

Getting back to your article – insightful points on real wages growth. Thanks for doing the research and compiling the numbers! I think you’re right about anchoring and bigger numbers. Indeed, why does inflation exist at all, except that we have an irrational need to be getting paid ‘more’ in nominal terms? (genuine question)

Also, this line had me in stitches – “the hardest part of renting is dealing with people who think you’re insane for renting!”.

kw

Haha thanks Kurt! Glad you like it mate.

The outlook for long term rates is pretty crazy really. It doesn’t bode well for those with lots of cash/bonds – zero real returns before tax. Also makes other assets quite cheap/attractive in comparison (post on this coming soon).

On why inflation exists… Well, I think a little inflation is the preferred option, because deflation is worse. Deflation effectively discourages spending and discourages investment – why would you invest or spend money now when you could expect lower prices in the future? And this feedback loop is obviously terrible for innovation, jobs, wealth etc. It’s a complex topic, but that’s my basic understanding.

Fair point, cheers mate. Looking forward to reading your follow-on article!