The Financial Independence community is an open, helpful and generous bunch of people.

Folks share their savings ideas, lifestyle philosophy, and often every detail of their personal finances. They share tips for earning more, and where to find the best deals on pretty much everything!

The aim of all this is to nudge along their peers, or help curious newbies learn the ropes of this ‘retire early’ business. But if there’s one thing that’s asked more than anything else, it’s how to invest and what to invest in.

I’m sure I speak for my fellow bloggers when I say, we love sharing our thoughts and trying to help others. But, finance bloggers can’t actually give people the ultra-specific answer they’re often looking for.

And that’s for good reason. Today, I’ll explain exactly why that is. Don’t worry, a short post today after the monster from last week!

This is true. It’s typically illegal for finance bloggers to give people specific advice for several reasons. They’re not licensed professionals for one thing. They don’t know your unique circumstances or goals. And plenty more.

Just because your favourite blogger invests 100% in the sharemarket doesn’t mean you should. You might not be able to stomach the volatility. And this may cause you to freak out and sell at the worst possible time.

Maybe the only way you feel comfortable is with a large amount of cash, bonds or even property, alongside your share investments. And if that’s what it takes to help you sleep at night, then maybe that’s the right approach, regardless of what others do, or what is considered ‘optimal’.

Perhaps the people you follow have a strategy that seems great on paper, but is tricky to manage. Does it look a little complex, when deep down, you’d really prefer a simpler approach?

They might be shooting for high growth, when really you just want to preserve your money and are happy with a modest return.

Do you want to actively manage it yourself, or outsource? Do you want to pick stocks? Do you want yield, growth or a bit of both?

It might seem like we’re all shooting for Financial Independence, but there’s more to consider than this. Maybe you’ll be moving overseas when you’re able to retire, or have future kids to plan for.

Do you want to start your own business at some point? Perhaps you’re looking at buying a house in 5 years. There’s a million things that could affect how much and when you need cash, and therefore, the way you build an investment portfolio.

Not all risks are the same. Some people worry about the gyrations of the sharemarket more than others. Others can’t stand the thought of underperforming the market.

The focus for many investors is to achieve the highest possible return. But do you have the stomach for that? Is it even possible to know this in advance?

Many investors want a portfolio where very little decisions need to be made. While others care more about avoiding short term losses, and try to stay out of ‘overvalued’ markets. These folks like to make active decisions based on the changing environment.

Some people worry about the risk of their investments not keeping up with inflation and running out of money later in life. Only you know which risks concern you the most.

Hopefully you can see what I’m saying here. All of these things affect how you’ll invest, what you’ll invest in and what time-frame you’re investing for.

And that’s for everyone to figure out for themselves. This depends on your situation now and in the future, the type of person you are, how you see the world, what you want from your investments, your long term goals, and the approach you feel most comfortable with.

How can a finance blogger possibly have an easy answer for that? It sounds like a cop-out. But when we sit back for a minute, we realise the reality of it.

Now you might be wondering why you bother reading finance blogs at all 😉

Well, we can obviously share what we do personally, and explain the thinking behind it. That can be a useful reference when people are trying to figure out their own approach.

And there are a number of other things about investing that most of us bloggers will agree on. I’ve listed some of these below, though of course there are more (and this wasn’t the point of this post). These things are important, and in general, are true for most people wanting to reach Financial Independence:

A low-cost advisor or ‘robo-advisor’ (like Six Park or others) may make sense if you really want a simple and hands-off approach. It’s not free, but might be worth it in some cases.

But you definitely don’t need a self-interested ‘helper’ which scrapes 1% per year from your balance (regardless of performance or service), for a complex portfolio of ridiculous high-fee funds, which are near-certain to underperform a simple low-cost approach.

Sadly, from the emails I get, these leeches still exist, and apparently have no trouble sleeping at night. I guess they believe their own bullshit. To admit they add no value would be uncomfortable at best, and identity destroying at worst.

By the way, I’m not saying there aren’t good, honest advisors out there who charge fair fees for solid advice. There are undoubtedly plenty of them! But I’d wager the leeches comfortably outnumber the legends.

Related to the above, choosing low fee widely diversified funds is about the number one lever we can control when it comes to improving our investment returns.

In an odd phenomenon, the finance world is about the only line of industry where, when you pay more, you actually get less value in return.

Some people prefer active investing over index funds, for various reasons. If going down this route, just be aware: Studies have shown the best predictor of future returns is fees. Whether active or index, low fee funds typically perform better than high fee funds.

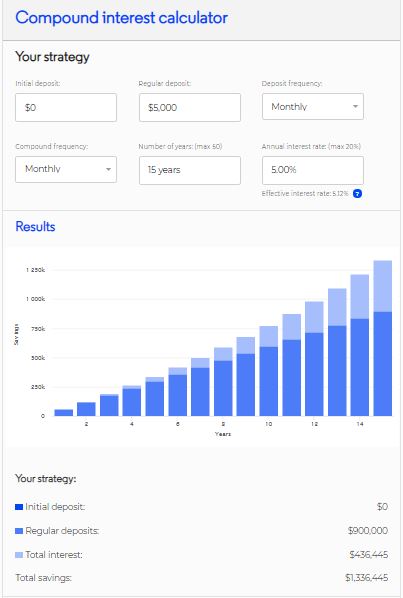

This can be seen with any compound interest calculator using a 10-15 year period. As you see below, the amount ‘deposited’ far exceeds returns. Especially over 10 years, but even over 15 years.

It doesn’t exist -simple as that. So quit trying to find it!

You certainly won’t make perfect choices (I don’t). Nor is there a perfect time to invest (post coming soon). Many of our purchases will turn out to be loss-making when looked at over a few years. That’s totally normal.

But considering we’ll own these investments for another 50-70 years, there’s plenty of time ahead for even the worst-timed purchase to become extremely profitable. And that’s another reason to relax – given the time-frames we’re working with, there is plenty of time to learn as we go!

Some people get stuck in the ‘research’ phase for far too long. But remember, getting started is more important than getting it right.

I better leave it there, before it turns into another 3,000 word beast! Hopefully you get where I’m coming from with this one.

The FIRE community loves to help each other, but what’s right for one person may not be right for another. Clearly, there are lots of factors to weigh up when it comes to investing – many of them unique to us.

So, next time you ask your favourite finance blogger a question like, “should I buy X?” or “what do you think of my portfolio,” and they’re a little shy or sheepish in answering… now you know the many reasons why! 🙂

Why deliberate spending is my favourite money management style. What it really means and how you can use it as your situation and priorities change over time.

My thoughts on ‘The Great Taking’. An idea that the masses will lose untold amounts of wealth in the next financial crash, due to a deliberate plan by mysterious figures.

Get my latest content and thoughts straight to your inbox.

A fresh dose of financial motivation to power your journey.

Thanks for writing this post and making it clear the trickiness we finance bloggers navigate! You’re right – there is no “perfect portfolio” and it’s far better to concentrate on reducing fees and increasing the amount we invest, rather than try to optimise returns to the last % decimal. I’m glad there’s a diverse blogging community in Australia and beyond who share what they do themselves, so readers can pick and choose tactics to suit their situations and values.

Great article. This is also worth keeping in mind when listening to the water cooler finance chat at the office or the ‘hot tip’ spruiked at the bbq.

YouTube finance bloggers annoy me so much, especially the ones who sell subscriptions, courses etc for the kind of stuff you can get for free if you look around hard enough. eg Some 20 year old kid with 2 years of a finance degree trying to pass himself off as an expert in equity investing just to get a youtube income so he doesn’t have to get a real job..Ffs..gimme a break.

Educating yourself is the key.. but we all want to know what the guy next door has in his portfolio and compare, its human nature. Who wants advice off someone who hasn’t been there and been successful? The bloggers with cred are the ones at the top of the mountain

who have made it under their steam and who explain strategy and not give 500 share tips a year and can backup those strategies with a winning portfolio. You should check out a bloke called Dave at

Strong Money, he seems to what he is talking about.. ????

Dont forget the people who have been doing it for 30 or 40 years and are still trying to flog off their book/course. If their advice was so good shouldn’t they be multi millionaires by now retired on a beach?

I understand there will be some who like to give back to the community and try to help people for minimal costs but they are few and far between.

Overall though as with all aspects of life we need to as diligent with financial advice as we are with used car salesmen, door knocking power companies and cold calling phone companies 🙂

The Warren Buffett bet should be essential reading for anyone before they make their first investment. Most folks on here would be familiar with it, but for those who aren’t…

In 2007, Buffett offered a $1m bet to any active fund manager reckoning that over a 10-year period the S&P500 returns would beat theirs. In other words, passively managed low-cost index funds would outperform an actively managed, more expensive one.

In 2008, the year a global financial crisis impacted the world’s economy, the S&P500 shed 37% of its value but gained every year after that. Despite this initial loss of $370,000, Buffett’s $1m ended up earning an average return of 7.1% over the 10-year stretch (i.e. $854,000 compounded). No actively managed fund beat this return, with the average being $220,000.

This was the actively managed fund industry’s chance to put up or shut up… instead it drove a nail in its coffin and for passive investors, it provides positive proof from arguable the world’s greatest investor that patience is all that’s required. A real tale for the ages.

Good post Dave, I agree that no one should be taking specific investment advice from anyone in the FIRE community. I see this so often with people asking in various social media groups about what to invest in without realising there is so much other information that needs to be taken into account, and even if you provide it that the people telling you to invest in whatever probably don’t have a lot of expertise or experience themselves.

It also seems to be widely assumed in the FIRE community that everyone is and should be all in on shares which isn’t always the case either, as you say people have different risk appetites and capacities so this needs to be considered as well. Then there’s things like tax, estate planning and all the rest of it, plus a lot of people put the cart before the horse and want to start investing before they’ve got an emergency fund and insurance in place as well!

Dave,

The first part of this post is great, covers all the points that people need to take into account when taking general advice from a blog.

But then your first point after is to negatively group together an entire industry of people, who actually can – legally- help with every point you’ve raised.

It’s really not good enough to put a token line saying ‘but I’m sure some are ok’ at the end.

No one is saying you can’t do it yourself – but you may as well criticise personal trainers as leaches, as people can just go for a run on their own instead.

I work in the industry (as is probably obvious) and I’ve seen some absolute duffers – but the newer breed of advisors are far more interested in the plan rather than the portfolio management. Passives are used far more than you’d think.

A good advisor can fill that gap in risk tolerances you mention – not everyone is cut out for the rollercoaster that equities can be but we all know without them in our supers and savings, inflation is going to kill our returns.

There’s a significant amount of research by our passive friends at Vanguard no less, that investors with advisers tend to add value far beyond their fees – but the majority of this alpha comes more from behavioural aspect of working with a counter party – with investment management being a tiny value add, if at all.

So if you do see a financial advisor and their first question is ‘what do you earn?’ Or ‘how much do you have to invest?’ then by all means run a mile.

I don’t use an accountant as I’m happy to do the graft & research myself but I don’t think all accountants are self interested (apart from a few legends!)

That said, I probably find that personal trainer…!

It is good to share some ideas with others at this kind of community. I have never had any idea about Financial Free concepts before I read any of self help books.

Everyone has different personality, level of toleration risks, age, lifestyle, and goals. One strategy doesn’t fit all. For example, you might hate your daily job and want to quit the job as soon as possible so you push very hard to save and invest in order to be financial free. For us, my husband got so much passion about his job and he is the type of person don’t have any hobbies except watching TV all day at his free time, then he might not be suitable to quit the job and be financial free as it will drive both of us crazy. We take slow approach and accumulate our wealth in order to be financial free. Financial free gives us security and freedom and we won’t need to rely on government when we are old.

Anthony Robbins’s book: Master Money Game also indicated that cost of investment will affect the ROI. Pete Wargent’s podcast, low risk and high return are pretty good to listen to. Most of financial bloggers gives you some ideas about how to be at better financial situation. You have to look at yourself and set up goals. Thanks to all of financial bloggers. They help me to increases my financial IQ. We are saving more than ever to reach our goals. We are not the type of persons many years ago, never had more than $1000 at bank. We are more resilient.

If you could share your knowledge and help others to achieve what they want, you will get what you want one day.

Completely agree and as a personal anecdote, I escaped from the influence of one of the leeches some years ago and started managing my portfolio myself and have never looked back – one of the best decisions I’ve ever made.

One thing I have noted though (seeing higher fee active fund managers were mentioned). While I agree that only a very small proportion of active fund managers outperform the index, that small proportion isn’t random. By that I mean it will usually be the *same* small proportion that outperform over the long term. Past performance isn’t indicative of future performance but this doesn’t mean that future performance is uncorrelated to past performance. In other words, a fund manager’s track record is important even if it’s not singularly definitive.